Original | Odaily Planet Daily (@OdailyChina)

Author | Ethan(@ethanzhang_web3)

RWA Sector Market Performance

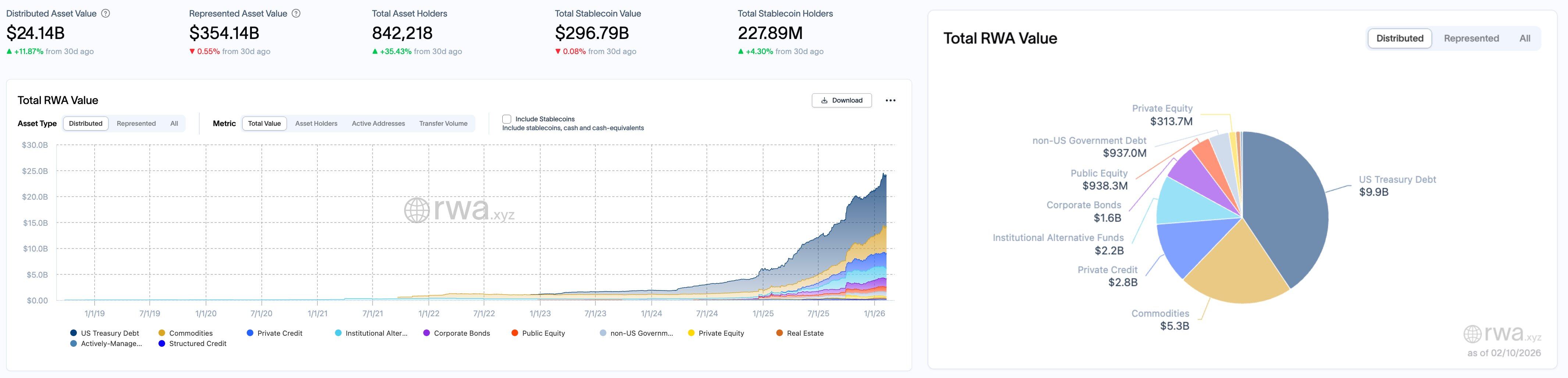

According to the rwa.xyz data panel, as of February 24, 2026, the total on-chain value of RWA (Distributed Asset Value) increased from $24.14 billion on February 10 to $25.07 billion, a total increase of approximately $930 million over two weeks, representing a growth of about 3.85%. The on-chain asset scale continues to refresh阶段性 highs. The Representative Asset Value rose from $354.14 billion to $362.56 billion, an increase of about $8.42 billion, representing a growth of about 2.38%.

For the first time, the user端 showed a decline. The total number of asset holders dropped from 842,200 to 710,400, a decrease of approximately 131,800 people, a decline of about 15.65%. In terms of stablecoins, the total market cap remained relatively stable, slightly decreasing from $296.79 billion to $296.10 billion, a reduction of about $690 million, a drop of about 0.23%. However, the number of stablecoin holders increased significantly, growing from 227.89 million people to 236.91 million people, an increase of about 9.02 million people, a growth of nearly 4%, indicating that the user base for on-chain funds continues to expand.

In terms of asset structure, U.S. Treasury bonds grew from the previous $9.9 billion to $10.6 billion, an increase of about $700 million, a growth of over 7%, making it the single largest contributing sector to the total volume this period. Commodity asset规模 remained around $5.3 billion,基本上持平 with two weeks ago, maintaining a high level. Private credit slightly increased from $2.8 billion to $2.9 billion, continuing a温和 expansion. Institutional alternative funds remained around $2.2 billion, with little change, staying in a sideways range; compared to the above assets, other asset categories showed smaller fluctuations.

Trend Analysis (Compared to Last Week)

Overall, compared to February 10, in this phase of the RWA market, the scale of on-chain distributed assets continues to expand persistently, with U.S. Treasuries becoming the main direction for capital承接. Commodities and private credit maintained high-level stability, with structural increments more concentrated in low-risk or high-liquidity categories. Additionally, stablecoin market cap moved sideways but users increased significantly, and overall risk appetite remained温和. Capital has not migrated on a large scale to high-volatility or low-liquidity assets; the structural focus still leans towards directions that balance yield certainty and liquidity.

Market keywords: Holder contraction, U.S. Treasury strengthening, Low-risk investment.

Key Event Review

US SEC Clarifies Net Capital Calculation Standards for Payment Stablecoins: Proprietary Positions Subject to 2% Haircut

The U.S. Securities and Exchange Commission (SEC) updated the Q&A on Rule 15c3-1 (Net Capital Rule) on its official website on February 19, clarifying the haircut treatment for broker-dealers when calculating net capital for proprietary payment stablecoin positions.

The解答 stated that if a broker-dealer认定 its proprietary held payment stablecoins have a "ready market" under Rule 15c3-1, then when calculating net capital, a haircut of 2% can be applied to the larger of the market value of the long or short proprietary positions. Under this treatment, SEC staff will not raise objections.

SEC Crypto Assets and Cyber Unit Chair Hester Peirce subsequently issued a statement supporting this treatment. She emphasized that stablecoins are important infrastructure for blockchain payments and trading, and reasonable capital treatment helps broker-dealers use stablecoins more effectively in custody, settlement, and businesses related to tokenized securities. She believes that compared to the 100% haircut some brokers might adopt out of caution, a 2% haircut is more in line with the reserve backing of payment stablecoins, which is primarily composed of U.S. dollars and high-quality short-term assets.

RWA Based on Hong Kong Assets Not Under the Jurisdiction of Mainland Chinese Regulatory Authorities

Following the joint release of the "Notice on Further Preventing and Handling Risks Related to Virtual Currencies and Other Matters" (referred to as "Document No. 42") by the People's Bank of China and seven other departments, the regulatory framework for mainland Chinese assets issuing RWA overseas is初步 taking shape. The general tone in Document No. 42 is a strict ban domestically and strict regulation overseas for RWA.

According to sources familiar with regulatory matters, Hong Kong is one of the overseas issuance locations for RWA. RWA based on Hong Kong assets are not within the scope of监管 of Document No. 42 and are not the responsibility of mainland regulatory authorities. Currently, there are no RWA based on underlying mainland securities or funds in Hong Kong or other overseas locations. If there were, they would fall under the responsibility of the Institutional Department of the China Securities Regulatory Commission (CSRC). Furthermore, "originally, it was一律 not allowed." Now, "it's not said that it's all not allowed," but there is strict regulation of mainland assets going overseas for RWA. There is no meaning of "encouragement" here; it must not be interpreted as "promoting development."

US SEC Discusses 'Gradual' Regulatory Path for Tokenized Securities, Plans to Launch Innovation Exemption Mechanism

U.S. Securities and Exchange Commission (SEC) Chair Paul Atkins and Commissioner Hester Peirce stated that the regulatory agency is considering introducing an "innovation exemption" for on-chain securities to promote the landing of tokenized securities in the U.S. capital market in a gradual manner.

Atkins pointed out at the ETHDenver event that this exemption mechanism would allow some tokenized securities to trade on new types of platforms on a limited basis, while accumulating practical experience for the establishment of a long-term regulatory framework. Peirce reiterated that tokenized securities本质上 still fall within the category of securities and should be advanced prudently within the existing legal system.

Over the past year, traditional financial institutions including Nasdaq and DTCC, as well as several crypto companies, have explored tokenized stock businesses. If the SEC approves the relevant path, crypto platforms may be able to offer blockchain-based traditional stock trading, competing with traditional brokers.

Currently, global demand for tokenized stock trading continues to heat up. Kraken reported that the cumulative trading volume of its xStocks product has reached $25 billion; the trading volume of Robinhood's RWA blockchain project exceeded 4 million transactions in its first week of launch. The SEC stated it will adopt a "step-by-step" approach to balance innovation and investor protection.

US Senator: CLARITY Act May Pass in April, Coinbase Sees "Path Forward"

U.S. Senator Bernie Moreno stated that the crypto market structure bill, the CLARITY Act, is expected to pass Congress before April. Moreno said in an interview with CNBC that a clear path for the bill's advancement has now emerged.

Coinbase CEO Brian Armstrong said in the same interview that there were previously disagreements surrounding stablecoin interest-bearing clauses and regulatory归属 issues, but各方 are now seeking "win-win" solutions. Reports indicate that the stablecoin yield clause is one of the main points of contention in the bill's advancement.

Moreno also stated that he does not believe the results of the congressional midterm elections will affect the bill's passage process. Previously, relevant White House officials also expressed positive expectations for the bill's advancement early this year.

US SEC Chair: Key Initiatives Including Investment Contract Determination, Innovation Exemption for Tokenized Security Trading to be Launched in Coming Months

The U.S. Securities and Exchange Commission website published the discussion content of Chair Paul Atkins at the ETHDenver conference, which disclosed the following matters to be considered in the coming weeks and months:

1. Develop a framework explaining how to view crypto assets subject to investment contracts. How such investment contracts are entered into and terminated;

2. Establish an innovation exemption to facilitate limited trading of certain tokenized securities on new types of platforms, with an eye towards establishing a long-term regulatory framework;

3. Propose a rulemaking proposal aimed at establishing a reasonable path for raising funds through the sale of crypto assets;

4. No-action letters and exemption orders to provide more clarity, including addressing wallets that do not require registration under the Securities Exchange Act;

5. Rulemaking regarding the custody of non-security crypto assets (including payment stablecoins) by broker-dealers;

6. Develop rules for the modernization of transfer agents to accommodate the role blockchain can play in record keeping;

7. Provide additional guidance and no-action letters to help the crypto community understand how existing rules apply to unique practical situations.

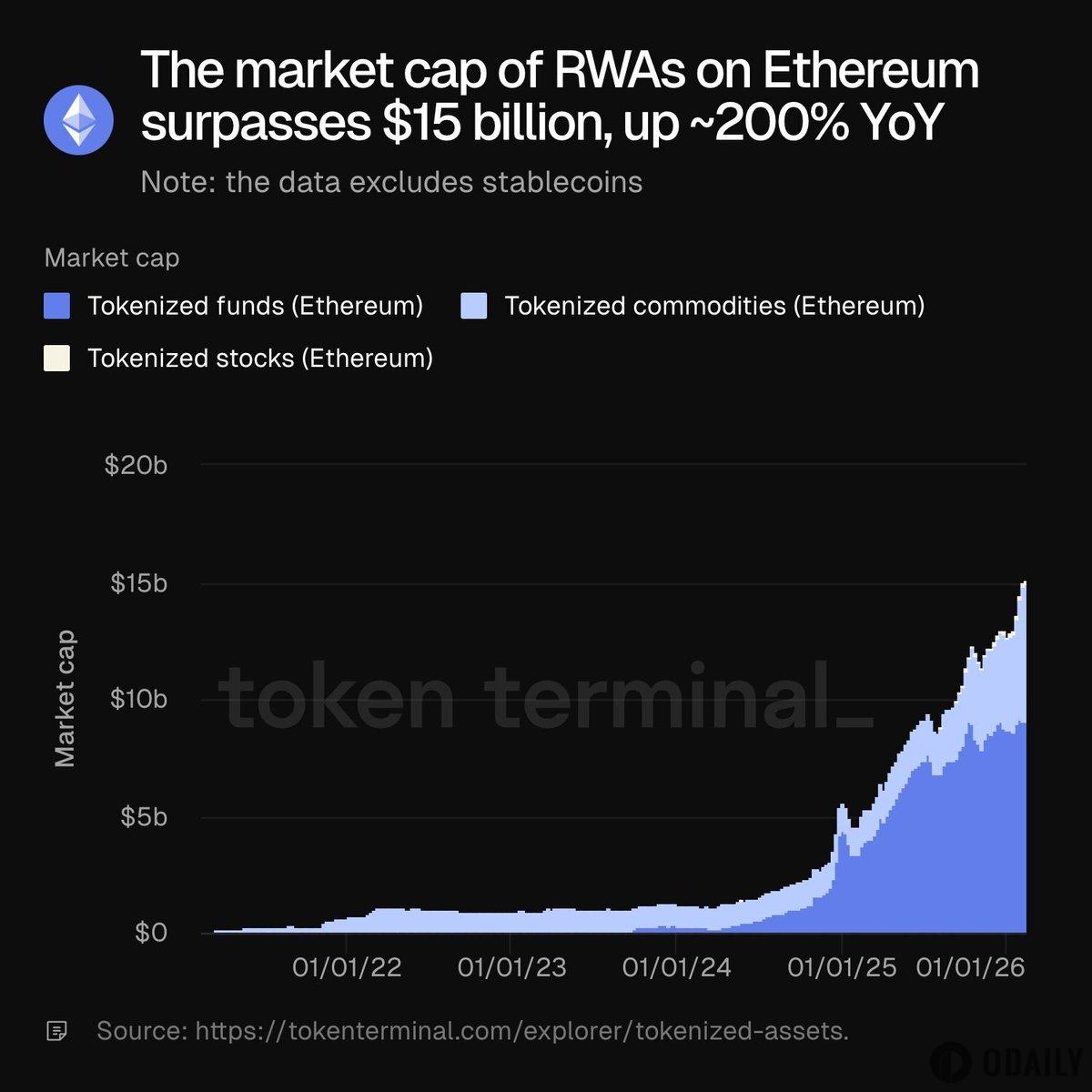

Total Market Cap of RWA Assets on Ethereum Chain Exceeds $15 Billion

On February 17, Token Terminal data showed that the total market capitalization of RWA assets on the Ethereum chain (including tokenized funds, tokenized commodities, tokenized stocks) has exceeded $15 billion, a year-on-year increase of about 200%.

OneChain Officially Announces Completion of $67 Million Series A Strategic Financing

OneChain recently officially announced the completion of a $67 million Series A strategic financing round. This round of financing will be主要用于 used to build a complete RWA (Real-World Assets) on-chain infrastructure面向 institutional asset issuers, financial institutions, and global investors, providing a one-stop solution for real-world assets from issuance, management, rights confirmation to liquidity trading.

This round of financing was jointly invested by Bitgo Capital, East Bank, PACIFIC BANK, and UBpay, with GBEX Holdings serving as the exclusive financial advisor for this financing.

Tokenizing Real-World Value (OneChain) is committed to converting real-world value into on-chain assets and is a compliant RWA asset issuance and management platform面向 the globe.

WLFI: USD1 Suffers Organized Attack, Token Maintains 1:1 Peg

WLFI issued a statement saying that USD1 suffered an organized attack that morning. The announcement pointed out that relevant personnel入侵 the accounts of several WLFI co-founders, spread negative information through channels, and simultaneously built large short positions on WLFI.

WLFI stated that USD1, backed by 1:1 asset support and minting and redemption mechanisms, currently continues to trade at parity with the pegged asset. The team emphasized that it will continue to advance its既定 plans and advised users to rely on information from officially certified channels.

Hot Project Dynamics

Ondo Finance (ONDO)

One-sentence introduction:

Ondo Finance is a decentralized finance protocol focused on structured financial products and the tokenization of real-world assets. Its goal is to provide users with fixed-income products, such as tokenized U.S. Treasury bonds or other financial instruments, through blockchain technology. Ondo Finance allows users to invest in low-risk, high-liquidity assets while maintaining decentralized transparency and security. Its token, ONDO, is used for protocol governance and incentive mechanisms. The platform also supports cross-chain operations to expand its application scope within the DeFi ecosystem.

Latest developments:

On February 12, Ondo Finance announced that Ondo Global Markets' tokenized stocks are now live on DeFi lending markets, first launching SPYon and QQQon, integrated with Morpho and Gauntlet. Ondo tokenized stocks and ETFs can now serve as efficient risk-managed collateral assets in Ethereum DeFi.

On February 13, Ondo Finance posted on platform X that the DeFi application for Ondo tokenized stocks, supported by Chainlink as the official data oracle, is now live. Institutionally priced assets like QQQon and TSLAon have unlocked on-chain stocks as high-quality collateral. With TradFi liquidity and oracle data, Ondo tokenized U.S. stocks can now support on-chain lending and structured products. The first projects launched are Euler Finance vaults, with risk management by Sentora and security provided by Chainlink. This marks the first time tokenized stocks are used as collateral in Ethereum DeFi.

Previously, Bloomberg senior ETF analyst Eric Balchunas stated on platform X that 21Shares is applying to launch an Ondo ETF.

MSX (STONKS)

One-sentence introduction:

MSX is a community-driven DeFi platform focused on tokenizing and on-chain trading of U.S. stocks and other RWAs. Through a partnership with Fidelity, the platform achieves 1:1 physical custody and token issuance. Users can use stablecoins like USDC, USDT, and USD1 to mint stock tokens such as AAPL.M and MSFT.M, and trade them 24/7 on the Base blockchain. All trading, minting, and redemption processes are executed by smart contracts, ensuring transparency, security, and auditability. MyStonks is committed to bridging the gap between TradFi and DeFi, providing users with a high-liquidity, low-barrier entry to on-chain U.S. stock investment, building the "Nasdaq of the crypto world."

Previous developments:

On February 11, Maiton MSX announced that its official website msx.com completed a comprehensive design upgrade on February 11, 2026. This revision focused on three main directions: "visual redesign, interaction optimization, and brand communication," including adopting a dark financial color scheme, introducing neumorphic style and character elements, and reorganizing the layout of market quotes and functional modules. In terms of interaction, the website increased page whitespace based on a grid system, weakened interference from non-critical information, and centralized and streamlined the entrances and buttons for high-frequency areas like quotes, positions, and order placement to shorten the operation path. Simultaneously, the website uniformly uses brand green to mark key operations and status feedback, improving the readability of key steps like order placement and confirmation, and reducing the risk of misclicks and misjudgments.

On January 13, Maiton MSX issued an announcement changing the fee collection model for RWA spot trading effective immediately. After the adjustment, this section changed from the original "two-way fee" to "single-side fee." The specific execution standard is that the buy side maintains a 0.3% handling fee, while the sell side handling fee is reduced to 0. This means that when users complete a full trading cycle of "buy + sell," the comprehensive transaction cost will be reduced by 50%. This fee policy is now effective across the entire MSX platform, covering all listed RWA spot trading pairs.

Additionally, Maiton MSX官方 previously published a 2025 review article "Anchoring the Era Window, Co-building a New On-Chain U.S. Stock Ecosystem," reviewing the阶段性 achievements of the year.

Related Links

《RWA Weekly Report Series》

《Robinhood Charges into L2, Focusing on RWA Tokenization》

《After Document No. 42 Sets the Tone, What is the Best RWA Token Standard?》

《Web3 Lawyer Interpretation: 8-Department New Regulation Lands, RWA Regulatory Path Officially Clarified》