Author: Chloe, ChainCatcher

Last month, just hours before attending a state banquet with King Charles III, Donald Trump's second son, Eric Trump, posted a five-paragraph defense on X. The trigger was a controversy surrounding a company under his name: he had been telling investors that the publicly traded cryptocurrency company "American Bitcoin," in which he was involved, could mine Bitcoin at about half the market price, a claim debunked by a Forbes report.

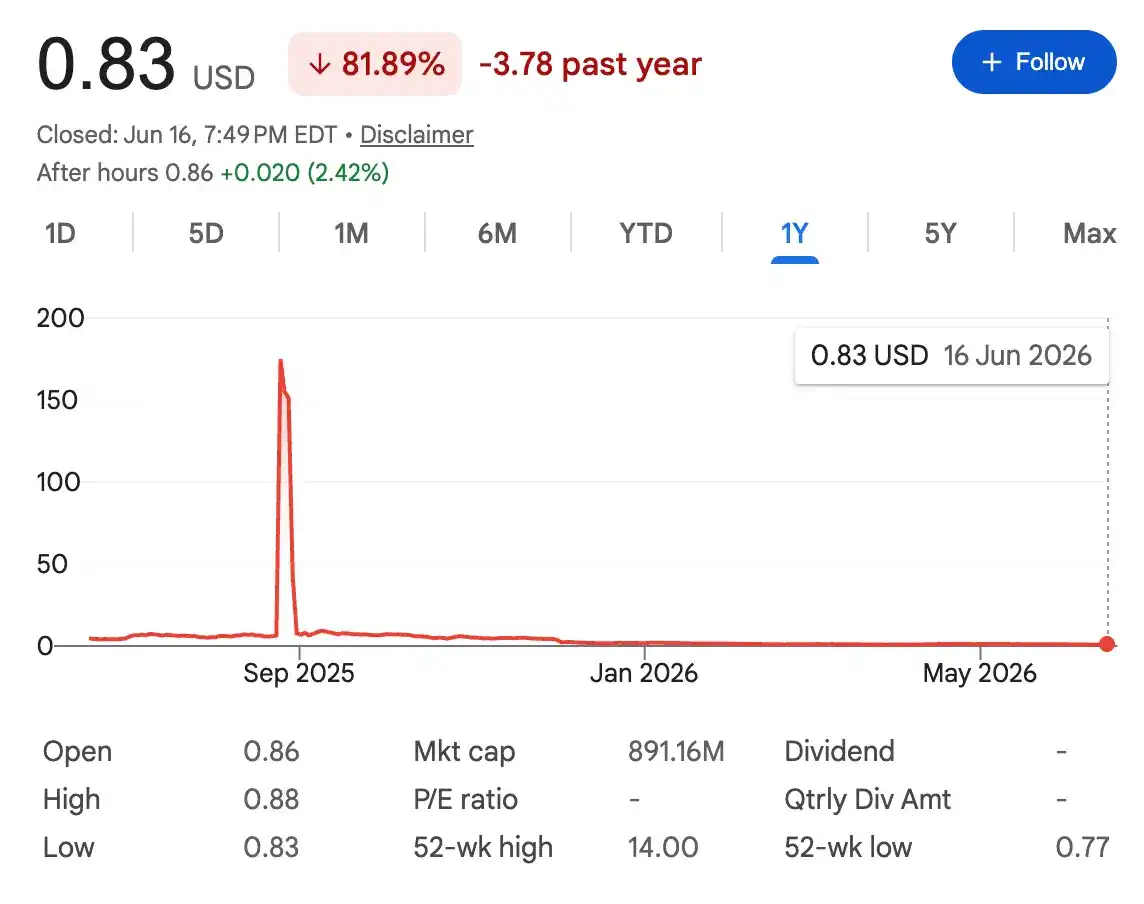

As of June 17, 2026, the stock price of American Bitcoin (Nasdaq: ABTC) had fallen to about $0.83, a crash of about 90% from its peak of around $175 last year and its IPO price of $14.

Then, in his post, Eric pivoted to another matter that has weighed on him for nearly a decade: a 2017 Forbes investigation into the children's cancer charity foundation he founded. He wrote that the attacks were "madness," portraying his younger self as simply a young man "dedicated to saving dying children."

There's no denying he did some good. Over the years, this foundation has donated over $25 million to St. Jude Children's Research Hospital in Tennessee. Its operations were streamlined, focusing on fundraising while leaving the complex execution to others. However, its other side revealed misleading rhetoric, sloppy accounting, a board entangled in conflicts of interest, and unabashed loyalty to Trump—and the same tactics are now appearing in the crypto industry.

The Trump Family Always Emerges Unscathed from Scandals

Through Freedom of Information Act requests, Forbes obtained thousands of pages of documents. They revealed that between 2011 and 2016, his foundation directed at least $500,000 in charitable funds back into family businesses through a series of transactions, most of which never appeared on tax filings.

These files also explain why the Trump family always gets away. Their playbook: first, counterattack loudly on TV or social media; then, use lawyers to bury paper trails; next, adjust practices just enough to satisfy regulators and avoid punishment, while changing nothing substantial. Once the dust settles, they re-emerge unabashedly as victims, asking the public for trust again—and there are always plenty willing to believe.

Eric's foundation is a case study of this script from start to finish. Nine years after the scandal, the renamed entity is still operating, expanding its fundraising year by year, spending over $500,000 annually, and holding events almost exclusively at Trump-branded venues.

Conflicts of Interest Were Obvious, Even the White House Was Involved

The foundation's origin was indeed well-intentioned. It began with Eric and his wealthy friends wanting to do good. The 2007 IRS application even stated, "Our family owns three golf courses in New York and New Jersey that can be used." It promised not to sign leases with any company controlled by its leaders. For the first three years, it held true, spending about $50,000 annually and raising hundreds of thousands.

But starting in 2010, Trump Organization employees joined the board, and expenses surged to $142,000 the following year. Former club manager Ian Gillule pointed the finger directly at Trump himself: In the early days, the foundation used venues for free, and bills often vanished. Trump was displeased, not with "helping for free," but with donating so much without leaving any paper trail or credit. He ordered that everyone, including his own son, be charged.

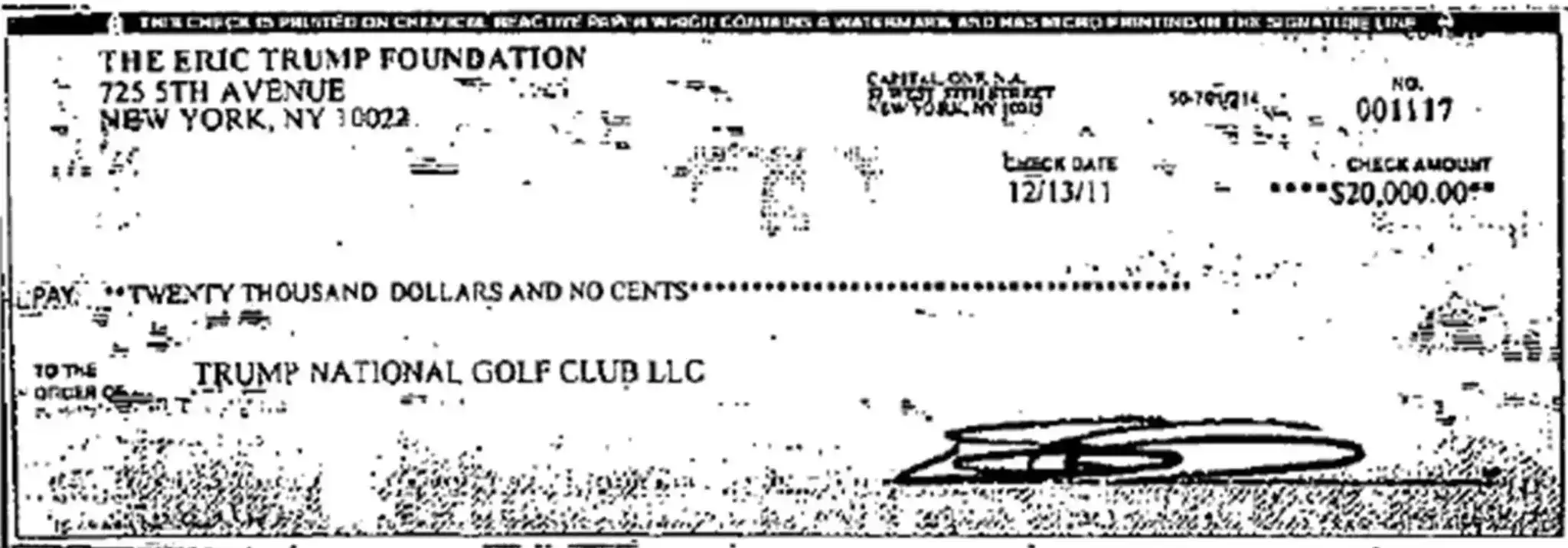

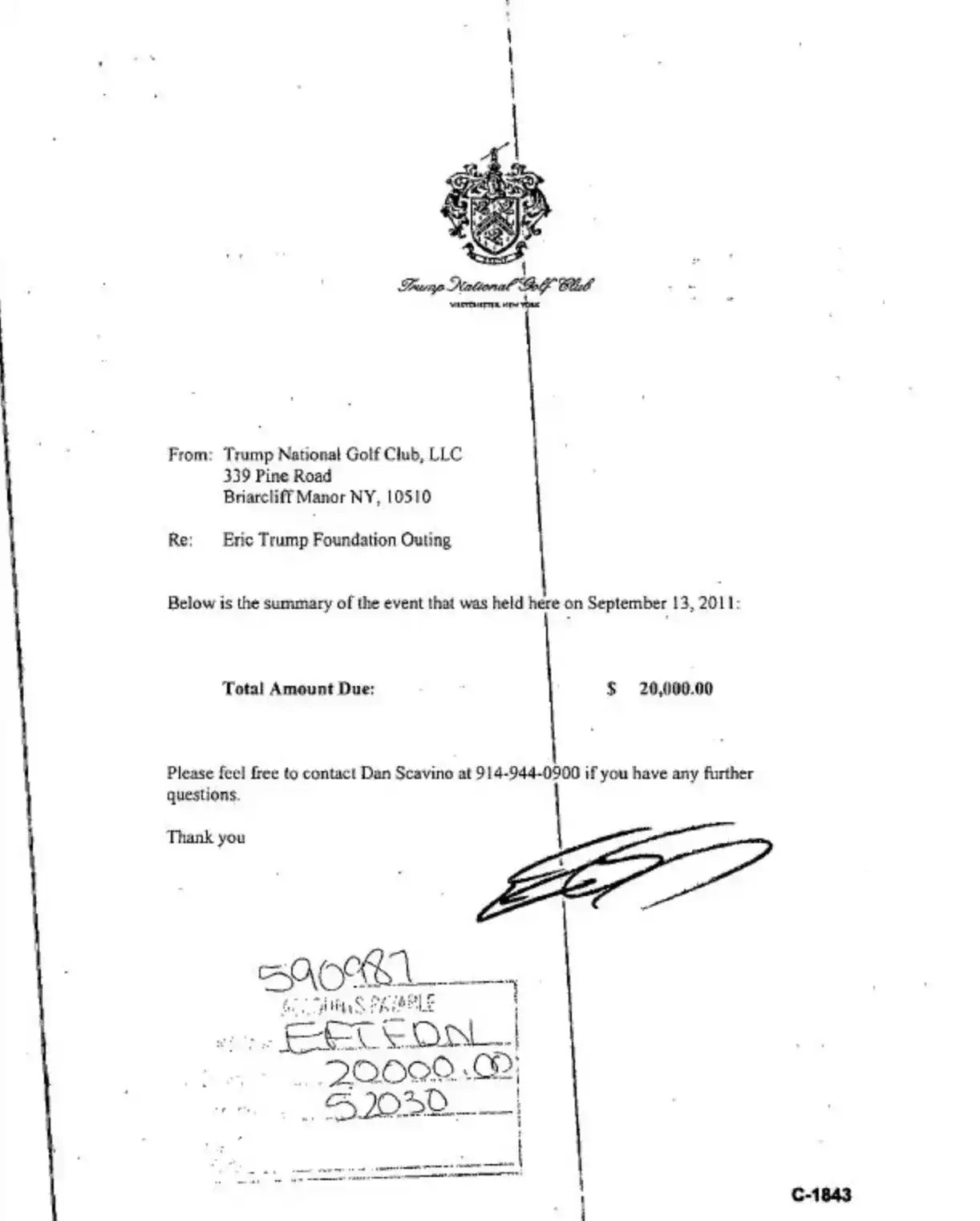

So, everyone got charged. After a 2011 event, Trump National Golf Club billed the foundation $20,000. A copy obtained by Forbes bore a note: "For questions, call Dan Scavino." The conflict of interest was glaring. Dan Scavino, now White House Deputy Chief of Staff, was then both the club's general manager and a foundation board member. The invoice bore Eric's signature at the bottom, though it's unclear in which capacity he signed. Bills kept coming: the club charged $100,000 in 2013, $99,000 in 2016, with Trump Soho Hotel and Mar-a-Lago also getting a cut.

Poisonous Candy Wrapped in Pretty Sugar

"Dear friends," Eric wrote in the 2014 gala program, the foundation has "one of the lowest expense ratios in the world," insisting on using only Trump-owned venues, full-time volunteers, donated catering, and celebrities performing for free, so that St. Jude received nearly all the funds.

But the books didn't match the rhetoric. The gala featured Hooters waitresses and mini Eric bobblehead dolls. Performers were mostly celebrities from "The Celebrity Apprentice." "They all performed for free," Eric claimed, yet he personally signed performance fee checks exceeding $90,000. Auction items "were all donated," but the foundation spent at least $65,000 procuring them. In 2012, it even bought an item for $6,040 that sold for only $3,310. Transportation was another expense, with Sunny's alone charging over $35,000.

Additionally, hundreds of thousands went to other charities, some with ties more direct to family interests than to childhood cancer; at least three also held fundraisers at Trump golf courses. In 2013, Eric even spent $1,600 of foundation money to buy a decorative copper still and an antique bottle washer near his family's winery. Of course, the foundation did donate large sums to St. Jude, from $220,000 in 2007 to $2.9 million in 2016, the year Trump was first elected.

Eric as Victim, Feeling 'No Good Deed Goes Unpunished'

Politics soon thrust the foundation into the spotlight. In late 2016, the Daily Beast and AP exposed its dealings with Trump clubs. The New York Times reported that an investment manager bid nearly $60,000 at a fundraiser auction just for coffee with Ivanka Trump. The problem wasn't just PR: under New York State and federal law, such related-party transactions required board votes, documentation, and disclosure on tax forms.

So, Eric decided to restructure, distancing it from the family: all Trump Organization employees left the board, including himself. He said his father's administration required avoiding "perception problems," so he wouldn't personally fundraise until after the term. The foundation was renamed Curetivity, pledging all donations would go to St. Jude. On the surface, it seemed a return to the original intent. But Eric remained defiant, telling Forbes a month after the board changes, "We get the use of the best facilities in the world 100% free of charge, which is why our expense ratio is the lowest in history."

The day the article was published, he went on Fox News, framing the scrutiny as a political witch hunt and casting himself as the victim. "I raised tens of millions of dollars and got hate in return."

Two days later, the Attorney General's office sent a letter requesting the books. The investigation hurt the foundation: donations in 2017 plummeted by over two-thirds, falling below $1 million, while administrative and legal expenses soared from nearly zero to about $50,000 annually. At year's end, the AG wrote again, highlighting multiple issues: financial reports not conforming to accounting standards, ignoring related-party transaction rules, misleading marketing, and threatening to revoke its fundraising license.

Thereafter, the accounts grew increasingly opaque. After Eric left the board, the occasional "related-party transaction" notes disappeared. The "rent/venue fees" line was consistently left blank. Fundraising expenses dropped from $384,000 in 2016 to $111,000 in 2017. By the end of 2018, when the AG's office indicated the investigation was shifting towards compliance rather than enforcement, Eric re-emerged in promotional materials, eventually being credited as the "founder" of Curetivity. Fundraising expenses rebounded, hitting a new high of $392,000 in 2019. How much flowed back to the Trump Organization became impossible to discern from the murky accounts.

Today, fundraisers continue to be held one after another at Trump-branded venues: in 2020 at Mar-a-Lago, costing $309,000; in recent years at Trump golf courses in North Carolina and Jupiter, Florida. If the fees are similar to the past, Curetivity alone could bring about $200,000 annually into Trump's business empire, accumulating over a million in two decades.

The Same Playbook Moved to the Crypto Industry

This playbook of "pretty words, value flowing back to insiders" didn't stop with the charity foundation; it has now been almost entirely transplanted into American Bitcoin.

Previously, Eric packaged this company as a "money-printing machine," publicly claiming it could mine Bitcoin at a 53% discount to spot prices, with a cost per Bitcoin around $57,000. It sounded remarkably similar to the foundation's "lowest expense ratio in the world." But just like with the charity, the books didn't match up.

The investigator this time was the same Forbes reporter, Dan Alexander, who exposed the foundation nine years ago. He found that about 70% of the company's Bitcoin wasn't mined; it was acquired by constantly issuing new shares and buying them on the open market. Factoring in depreciation and overhead, the all-in cost per coin was actually close to $90,000, far above Eric's claimed $57,000.

Now, the stock price has collapsed about 90% from its late-2025 peak of around $175 and its $14 IPO price. Retail investors are estimated to have lost about $5 billion cumulatively. Financially, it's bleeding, with a net loss of about $81.8 million in Q1 2026. On the insider side, the view is completely different.

The founders initially received shares at near-zero cost. Even with the 90% stock crash, Eric's personal stake is still worth about $70 million; during the same period, his net worth is estimated to have grown to about $300 million. The aftermath script also feels familiar. Facing questions, Eric didn't directly address Forbes' calculated costs and dilution. Instead, he countered with impressive numbers like quarterly revenue growth and holding over 7,000 Bitcoins. On X, he railed against Forbes as a political weapon and a disgrace to journalism.

Last September, Eric stood at the center of a party at the Westchester Country Club, hosting the 19th Curetivity fundraiser, surrounded by several important business partners. Since his father's re-election, his net worth has exploded from an estimated $40 million in 2024 to $300 million today.