Authors:Dave Mazza, Thomas DiFazio

Compiled by: Deep Chao TechFlow

Deep Chao Guide: The market capitalizations of the world's three largest memory chip manufacturers have all surpassed $1 trillion. Morningstar promptly published an article reminding investors not to forget fundamentals. Roundhill Investments (the issuer of the DRAM ETF) countered point by point: AI infrastructure has reshaped the supply and demand structure of the memory industry; the manufacturing barriers of HBM make it impossible for new players to enter; and the combined projected profits of the three giants for 2027 are expected to reach $704 billion. Please note that the authors of this article are the managers of the DRAM ETF, a naturally bullish position.

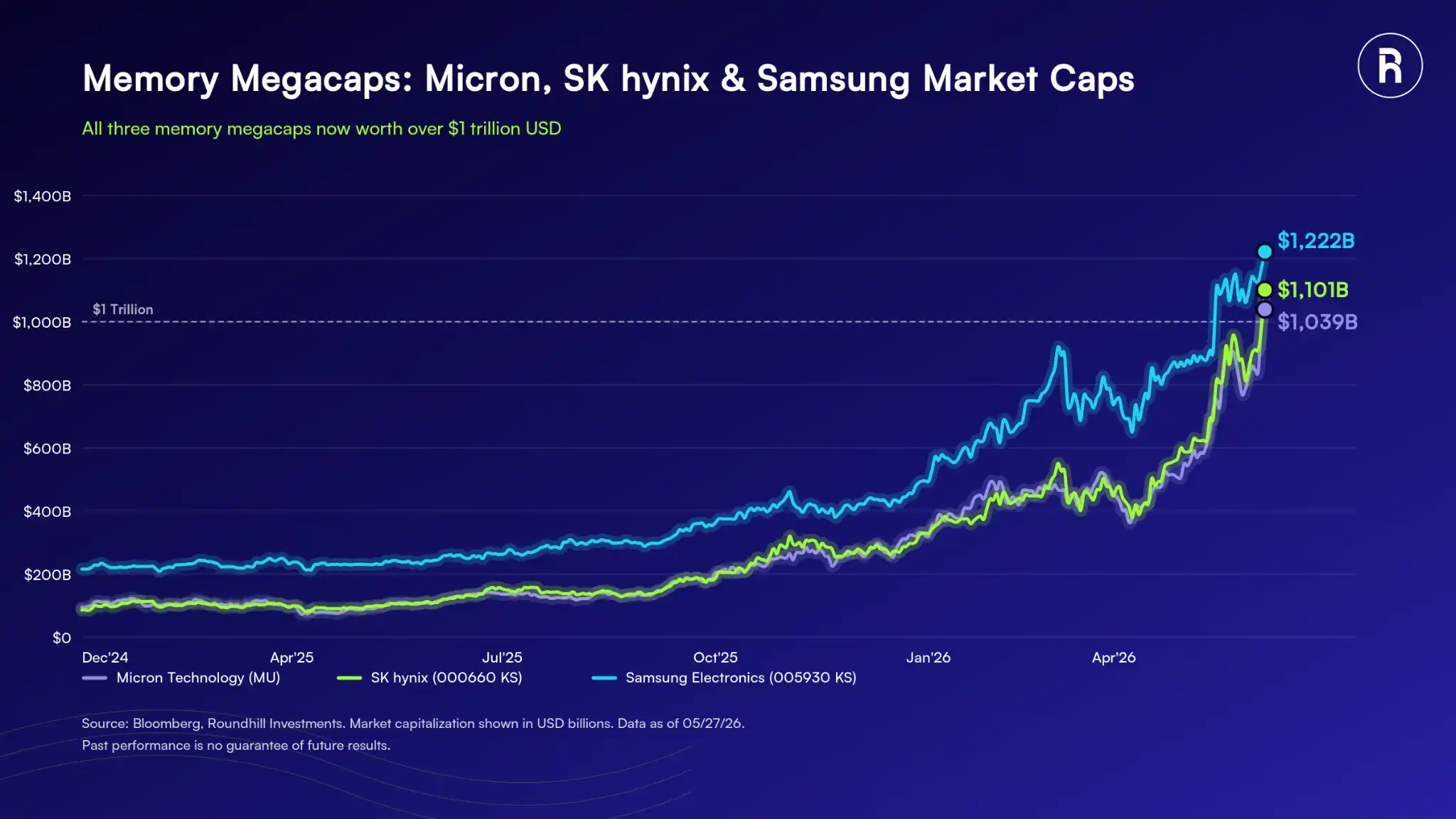

The world's three largest memory chip manufacturers—Samsung Electronics (005930 KS), SK Hynix (000660 KS), and Micron (MU)—have all surpassed a market capitalization of $1 trillion, joining an exceedingly rare club. However, this milestone has also invited scrutiny.

Morningstar recently published a blog post reminding memory ETF investors not to overlook fundamentals, raising several pointed questions:

- A Cautionary Tale from History: The memory industry has repeatedly experienced boom-bust cycles. Investors might be ignoring this history.

- Memory Companies Lack Moats: Memory is essentially a commodity business. New capacity can always enter the market and erode pricing power; companies lack true barriers to protect profit margins.

- The Rally Might Be Momentum-Driven, Not Fundamentals-Driven: The enthusiasm surrounding memory stocks reflects more excitement about AI than a sober analysis of earnings, profit margins, and supply-demand dynamics.

- Valuations Have Skyrocketed: Memory stock prices have surged significantly, possibly running ahead of fundamentals.

Caption: Overview of the Memory Chip Industry

Roundhill's position is: this time is different. To understand the future of the memory industry, one must first look back at its past.

History is Indeed a Warning, But Is History Still Relevant?

The boom-bust cycles of memory chips are a fact. A classic cycle occurred in the mid-1990s. Microsoft released Windows 95 in August 1995, transforming personal computers from business-exclusive to consumer goods. The DRAM capacity per PC quadrupled from 1-2 megabits to 4-8 megabits. Manufacturers were caught off guard by the sudden demand, leading to a frenzy of factory construction and expansion, ultimately resulting in oversupply and a price collapse.

A similar story unfolded in the mid-2010s. When Apple released the iPhone 7 and upgraded the base storage from 16GB to 32GB, it seemed like a small change. But scaled up, demand surged dramatically. Manufacturers again invested heavily, followed by oversupply and price drops.

These cycles share a common pattern: technological breakthrough → surge in demand → manufacturer expansion → oversupply → price collapse.

The question is, is this pattern still applicable today?

The memory chip industry has undergone structural changes. Memory demand is no longer tied to consumer electronics upgrade cycles but to the compute power expansion of AI infrastructure. The scale of this market far exceeds a single smartphone upgrade wave, and its growth potential is much larger.

DRAM and NAND prices have increased more than fivefold since January 2024, leading hyperscale customers to begin demanding long-term supply agreements to lock in bandwidth. Historically, long-term supply agreements in the memory industry have been loose frameworks subject to market changes. But this model has changed. During its January 2026 earnings call, SK Hynix stated that current agreements reflect "strong reciprocal commitments" between customers and suppliers, citing the high capital intensity of advanced memory manufacturing. Micron also reported similar long-term agreement conditions.

Caption: DRAM and NAND Price Trends

The Moat of Memory Chips: Manufacturing Complexity

Not all memory chips are created equal. The memory driving today's AI systems is called High Bandwidth Memory (HBM), which is entirely different from the memory in phones and computers. HBM is specifically designed for AI workloads, with extremely demanding manufacturing conditions.

Data from Goldman Sachs shows that SK Hynix, Samsung, and Micron control nearly the entire global supply of HBM. This industry has consolidated over decades, and the accumulated manufacturing expertise cannot be replicated overnight. Manufacturing complexity itself is the moat, and it's the very reason these three companies have reached this point.

Caption: Global HBM Market Share Distribution

This logic is completely different from that of the old cycles. The past was: demand rises → new capacity enters → prices collapse. The current bottleneck is not capital or willingness, but technical capability. SK Hynix currently controls about 58% of the global HBM supply. On June 2, it announced plans to double wafer capacity over the next five years while warning that supply shortages would persist until 2030. Building a new factory takes at least 3 years, or over 5 years for a completely new site.

Furthermore, ASML—the sole manufacturer of extreme ultraviolet (EUV) lithography machines, essential for producing advanced memory chips—entered 2026 with a backlog of €38.8 billion, exceeding its full-year projected sales. The delivery lead time for a single EUV machine exceeds 12 months. This bottleneck cannot be resolved in the short term.

Fundamentals: Memory Manufacturers Poised to Join Ranks of World's Most Profitable Companies

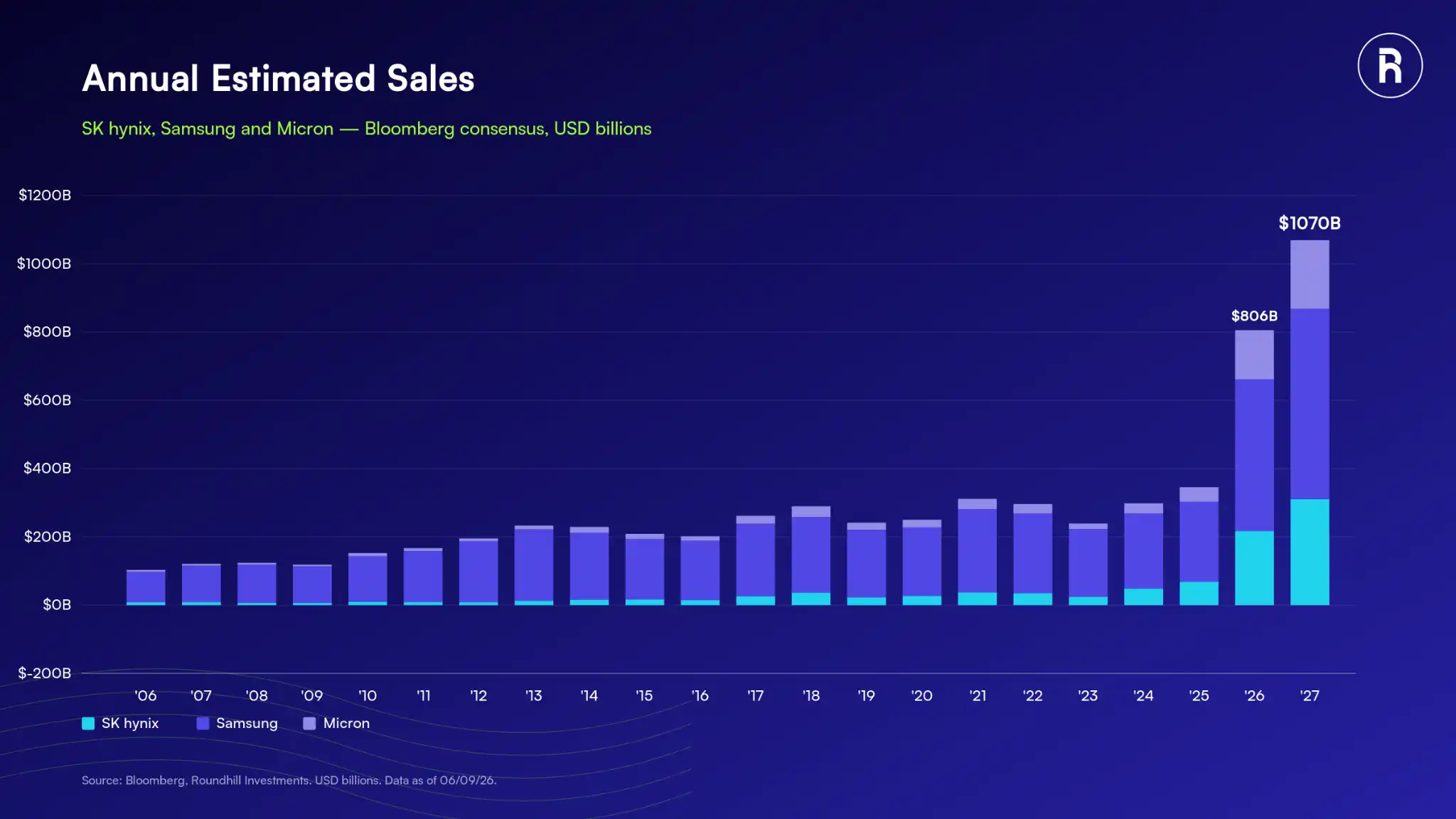

The earnings, revenue, and margin expectations for Samsung, SK Hynix, and Micron reflect the secular wave of AI adoption. Bloomberg consensus estimates show that by 2027, these three companies will rank among the world's top ten most profitable companies.

Caption: Forecast of the World's Most Profitable Companies for 2027 (Bloomberg Consensus)

The combined bottom-line profit forecast for the three companies for 2027 is $704 billion, with total revenue exceeding $1 trillion.

Caption: Revenue Forecast for the Three Major Memory Manufacturers

Caption: Profit Forecast for the Three Major Memory Manufacturers

In terms of margins, the operating gross margins of Samsung, SK Hynix, and Micron have reached historical records, surpassing the previous highs of 2018.

Caption: Historical Gross Margin Trends for the Three Major Memory Manufacturers

Numbers like these have never been seen in the history of the memory industry. Even if growth slows, in the context of generative AI's continued integration into the global economy, the memory industry is expected to settle on an unprecedentedly high baseline.

Valuation Reassessment in the New Era of Profitability

Historic stock price performance combined with substantial upward revisions to fundamentals suggests the industry is undergoing a significant revaluation driven by earnings growth and margin expansion.

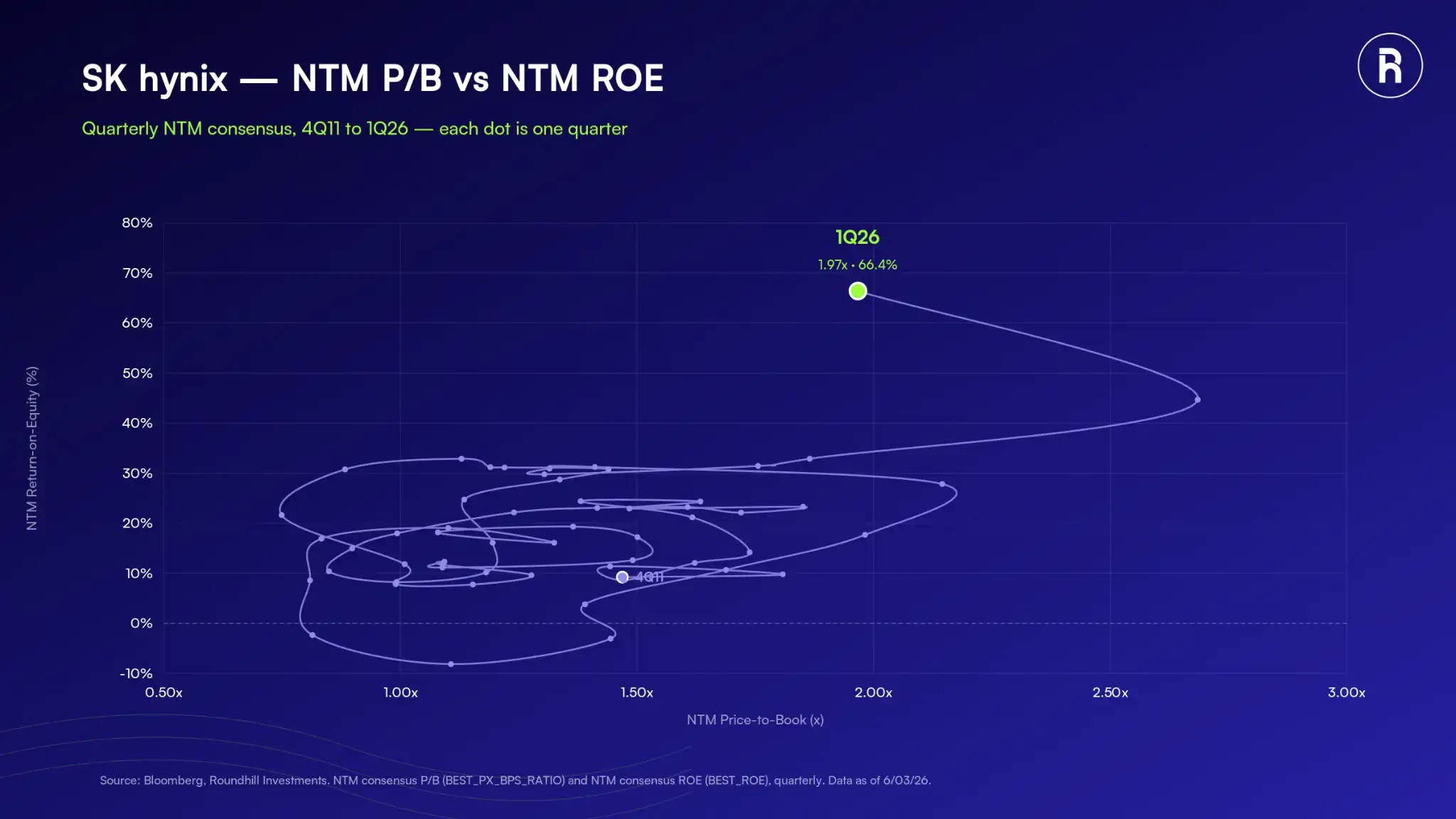

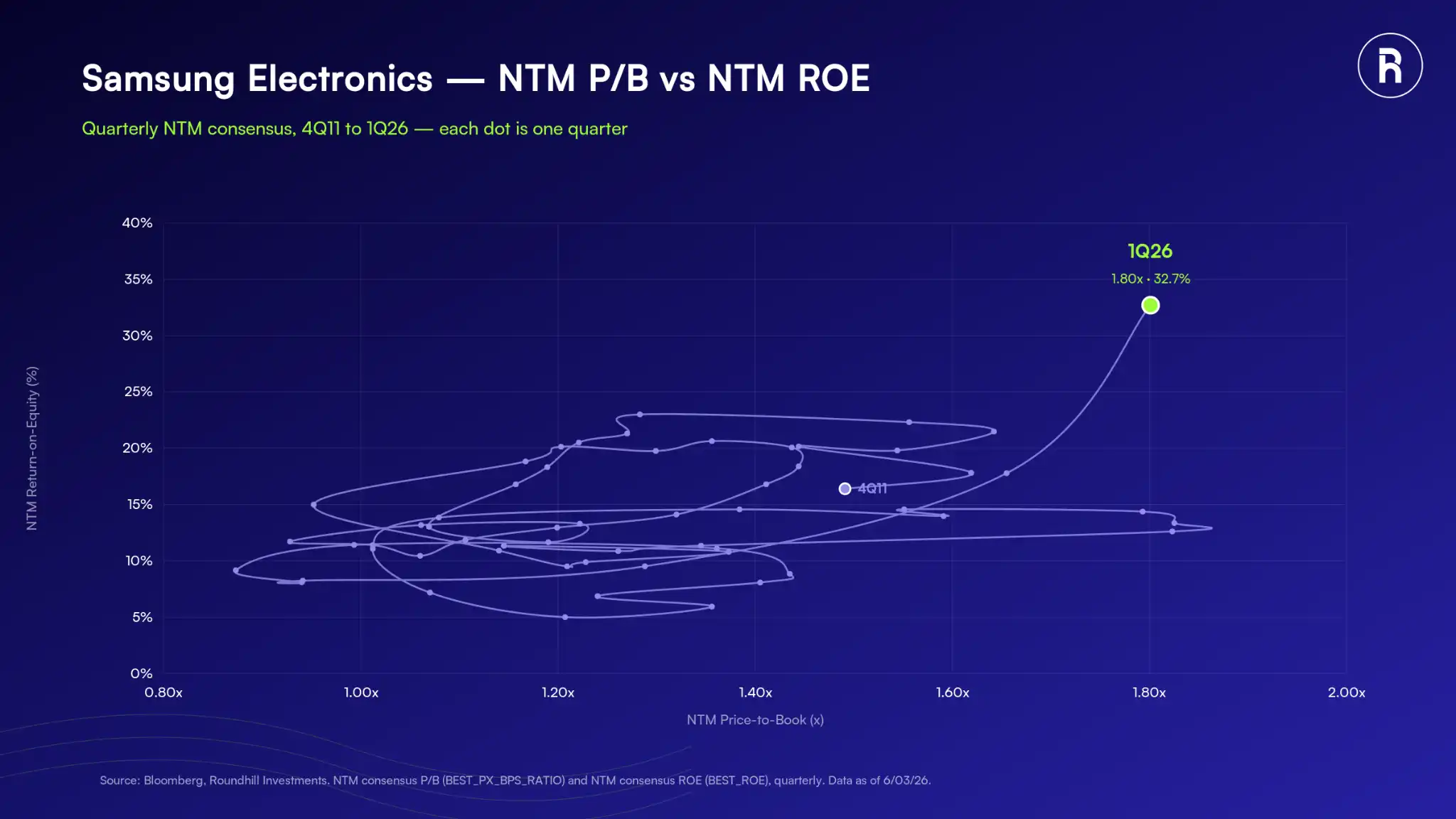

SK Hynix and Samsung are two case studies. For nearly a decade, the NTM (Next Twelve Months) price-to-book ratios of both stocks fluctuated within a certain range, constrained by the boom-bust earnings characteristics of the memory industry. But this ceiling may no longer apply. The expected ROE (Return on Equity) for both companies has surged to levels never before seen in the history of the memory industry. The valuation frameworks investors have long used to judge these stocks need to be re-examined.

Caption: SK Hynix NTM Price-to-Book Ratio and ROE Trend

Caption: Samsung Electronics NTM Price-to-Book Ratio and ROE Trend

Despite the recent dramatic stock price gains, the median NTM P/E ratio of the DRAM ETF's holdings is only 8.37x, which is attractive compared to the broader tech sector. Meanwhile, the median current fiscal year EPS growth rate for the portfolio is 632%. Arguing that memory stocks are overvalued is essentially applying old data to a new industry. In Roundhill's view, the gap between historical valuation conventions and current fundamental performance represents opportunity.

Caption: DRAM ETF Holdings Valuation and Earnings Growth Overview

Conclusion: Why Roundhill Isn't Worried

Being skeptical of surging stock prices is reasonable; fundamentals always matter in the long run. But in this case, fundamentals are precisely the reason for the rise in memory stocks.

The old cycles were characterized by: demand explosions without an upper bound, manufacturers over-expanding, and an inevitable price collapse. Today's situation is structurally different: manufacturing barriers limit new entrants; industry leaders themselves say supply shortages will persist until 2030; and the earnings cycle has just begun to reflect the scale of AI infrastructure buildout.

Roundhill believes the market is currently pricing not a bubble, but an industry that has struggled through booms and busts for decades entering a new era.

⚠️ Editor's Note: The authors of this article, Dave Mazza and Thomas DiFazio, are both members of Roundhill Investments, the issuer and manager of the DRAM ETF (Roundhill Memory ETF). The article's position is naturally bullish. Readers should form their judgment by considering third-party views such as those from Morningstar. The ETF risk disclosures and legal disclaimers from the end of the original article have been omitted. Please refer to the original link for complete information.