Article sourced from: a16z crypto

Compiled by: Moni, Odaily Planet Daily

Tokenized Assets, often referred to as "Real World Assets (RWA)", are altering the form of assets, how they flow, and the way financial systems are constructed.

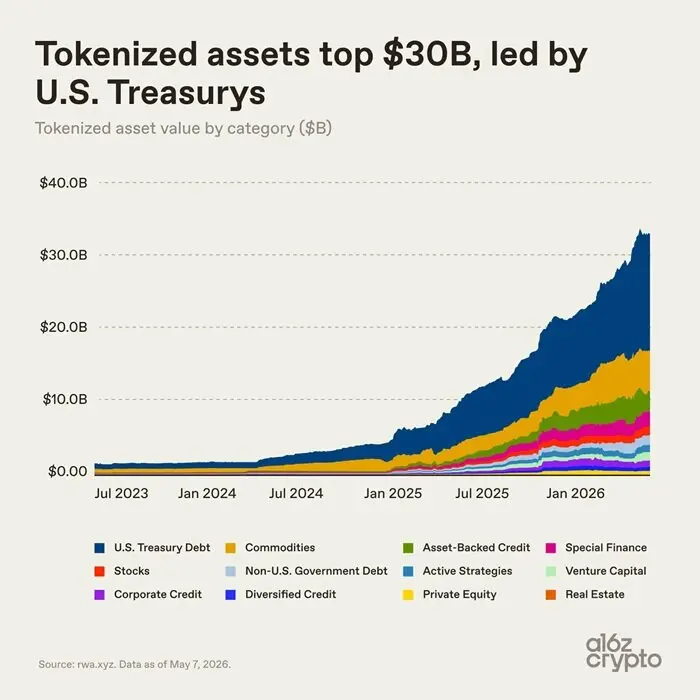

Just last month, the market size of tokenized assets surpassed $30 billion and is currently stable at around $34 billion (excluding stablecoins). This scale is roughly equivalent to a regional bank or a top-tier university endowment fund. While still minuscule compared to the global financial system, it is substantial enough to have a real-world impact.

Consider that two years ago, the tokenized asset market was less than $3 billion, but then the landscape changed dramatically: the US GENIUS Act brought a clearer regulatory framework for stablecoins, institutional-grade on-chain infrastructure matured, and a large number of financial institutions began deploying blockchain technology almost simultaneously. It was the combined force of these factors that drove the tokenized asset market to grow tenfold in under two years. (Note: Although stablecoins are not included in the above statistics, they have substantively propelled the entire market's growth by significantly simplifying on-chain payments and settlements.)

This article will use 7 charts to analyze the reasons behind the rise of tokenized assets and their future trajectory.

Tokenized Assets Take Off: US Treasuries as the Primary Growth Engine

US Treasuries have been the main driver of recent growth in the tokenized asset market.

The advantages of tokenized US Treasuries are clear and intuitive: investors can hold stable, yield-generating assets in a digital form, enabling more efficient and flexible trading and transfer; financial institutions can achieve improvements in settlement and collateral asset allocation efficiency, seamlessly connecting with digital financial markets.

Crypto investors can also leverage tokenized Treasuries to utilize idle stablecoins, gaining access to traditional money market yields. Asset management institutions like BlackRock and Franklin Templeton have followed suit with their deployments, catalyzing a trillion-dollar market.

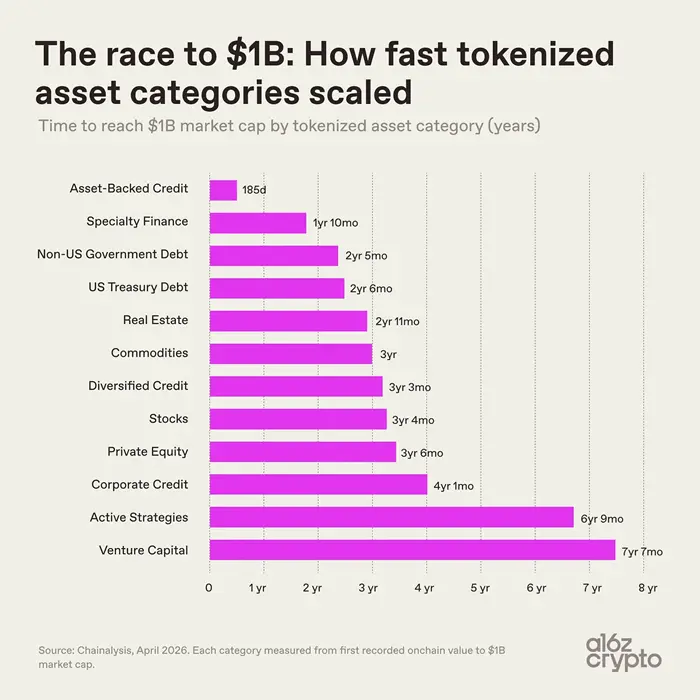

It's important to note that the growth rates vary significantly across different types of tokenized assets, stemming from both the technical and compliance challenges of bringing various assets on-chain, as well as market acceptance after product launch.

- Asset-backed credit assets lead the growth by a wide margin. These tokenized assets mainly include tokenized home equity lines of credit, lending vault tokens, with reinsurance contracts and Bitcoin mining notes among other niche financial assets following, reaching a market cap of $1 billion within two years.

- Venture capital assets took over seven years to surpass a $10 billion market cap, with active strategy assets on a similar timeline. These assets have complex structures, long investment cycles, and higher operational and regulatory barriers.

- Treasuries and commodities took a moderate pace, reaching a $10 billion market cap in 2 to 3 years and are now mainstream categories in the market.

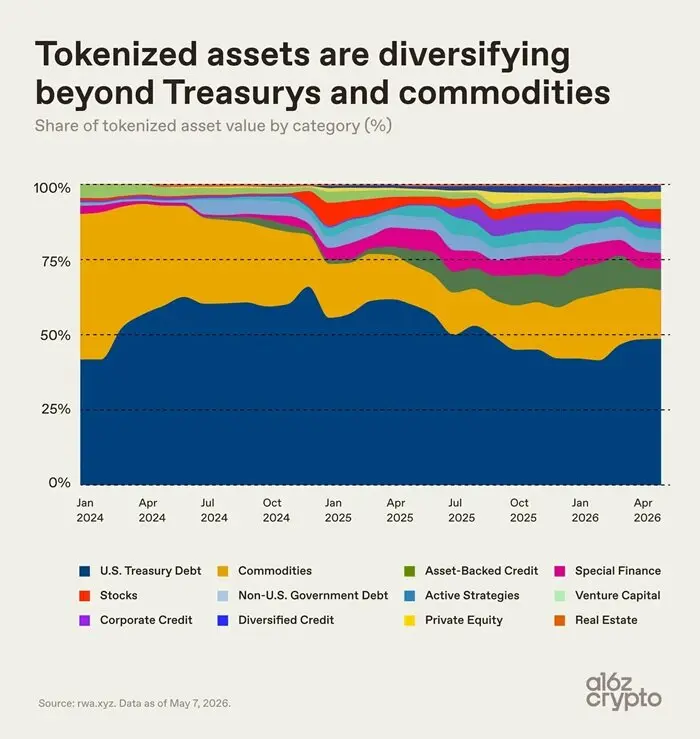

At the beginning of 2024, Treasuries and commodities almost entirely dominated the tokenized asset market share. After 2024, categories like credit, niche finance, and equities steadily increased their shares, but market concentration remains high. Currently, US tokenized Treasuries and commodities collectively account for about two-thirds of the market.

Segmented Landscape of the Tokenized Asset Market

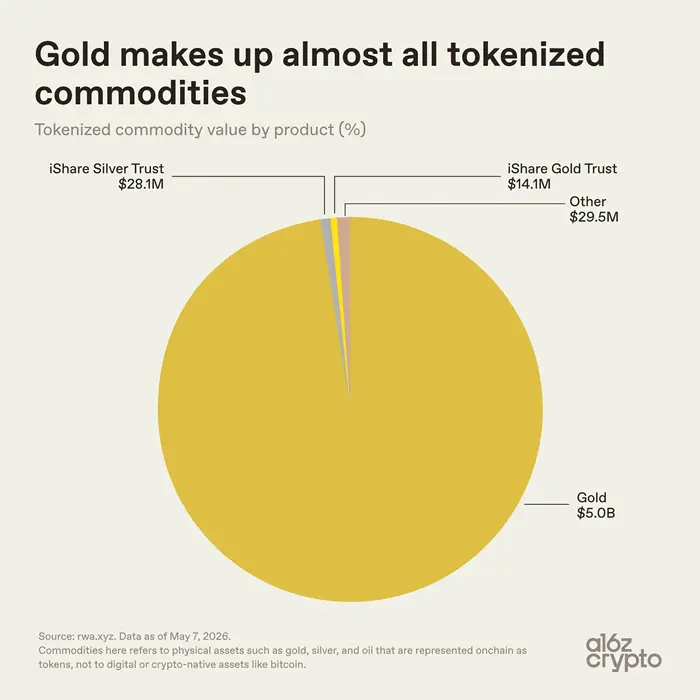

The commodity tokenization sector is highly concentrated internally, with gold tokens dominating the vast majority of the share, totaling about $5.1 billion, of which gold tokens account for $5.0 billion. Silver and other category tokens amount to only $57.6 million, constituting less than 0.01%.

Gold is inherently well-suited for the tokenized asset model. Currently, the commodity token market is essentially led by gold because it has a globally unified standard, is easy to store, not easily perishable, and has long been traded based on entitlement certificates.

Furthermore, crypto market investors have historically favored gold assets, with Bitcoin being hailed as digital gold early on. Products like Tether's gold token XAUT and Paxos' gold token PAXG map ownership of vault gold to the blockchain, converting physical gold entitlements into digital tokens that can be held in on-chain wallets.

Tokenized assets for crude oil, agricultural products, and emerging categories like energy and computing power have an extremely low market share, with the industry still in its nascent stage.

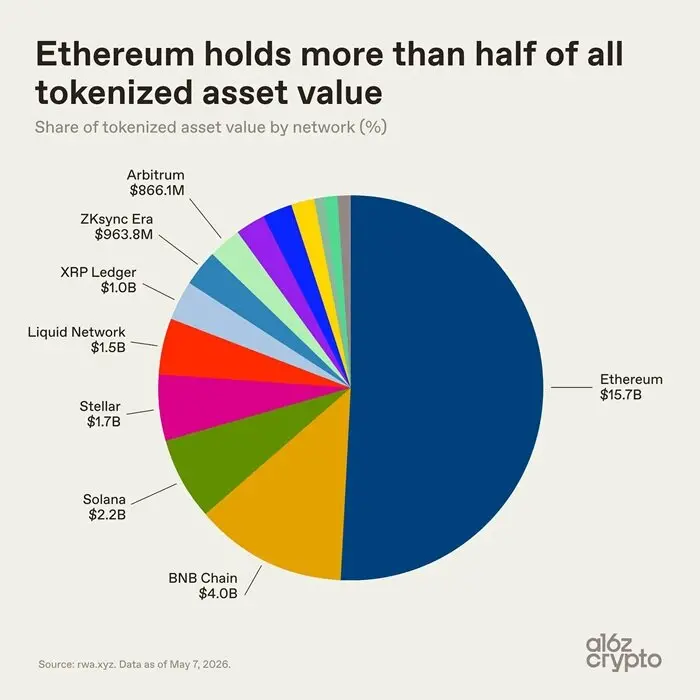

Looking at the distribution across underlying public chains, the tokenized asset ecosystem is more diverse. Ethereum, leveraging its first-mover advantage in decentralized finance and institutional adoption foundation, still holds the leading position, hosting assets worth $15.7 billion, accounting for over half of the market.

The remaining tokenized asset market is distributed across multiple public chains: BNB Chain's tokenized asset market size is about $4.0 billion, Solana about $2.2 billion, Stellar about $1.7 billion, Bitcoin sidechain Liquid Network about $1.5 billion, while XRP Ledger, ZKsync Era, and Arbitrum each have on-chain tokenized asset sizes close to $1 billion.

The tokenized asset industry has not consolidated onto a single public chain. Assets are distributed across major blockchain ecosystems based on transaction costs, liquidity, compliance requirements, and business partnerships. However, the most telling data point is not the size of the tokenized asset market... but rather how these assets are being used.

Let's continue the analysis—

Most Tokenized Assets Currently Lack "Composability"

Market size is not the only core metric; the actual application value of assets is more telling.

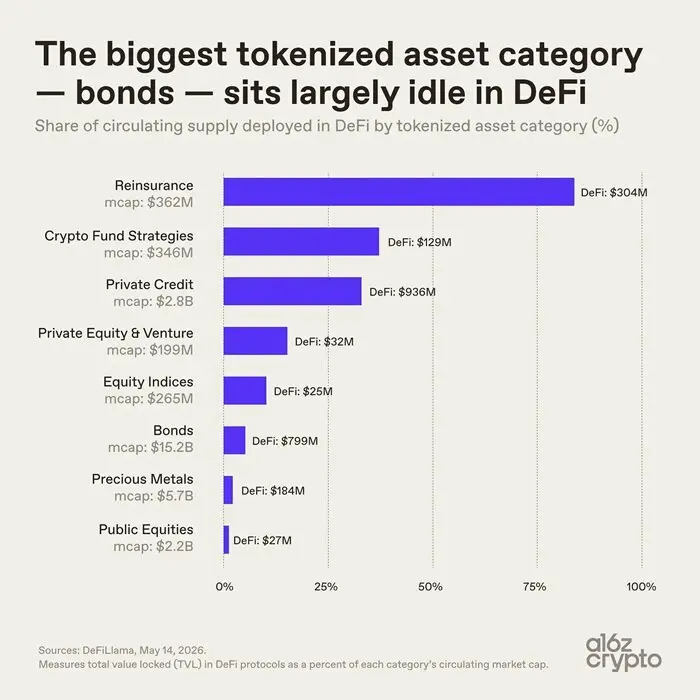

Bonds are the largest category of tokenized assets by market cap, at $15.2 billion, but only 5% of the circulating supply is utilized in DeFi protocols, amounting to just about $800 million. The utilization rate for precious metal tokenized assets is similarly low, with most tokenized assets only used for on-chain storage, not yet becoming freely composable and interactively reusable financial building blocks.

The performance of niche tokenized asset categories is starkly opposite: reinsurance tokens with a market cap of $362 million have an 84% on-chain protocol usage rate; private credit tokens have a 33% usage rate. These asset types were designed from the outset to fit composable on-chain application scenarios. In contrast, top-tier tokenized assets like Treasuries and gold are primarily positioned to simplify on-chain asset holding and transfer without altering the asset's inherent operational logic. This situation highlights a core divergence in the tokenized asset industry: varying degrees of on-chain nativity among different tokenized assets.

Some assets can flow and be applied freely across chains, while others merely use blockchain as a ledger tool, with limited asset transfer and composability functions. Currently, most tokenized assets are essentially just digitized assets, merely migrating accounts onto the chain without unleashing their composability potential. Composability is the core value of on-chain finance and a key to upgrading the financial system.

Pantera Capital's Token Native Index shows that over 70% of tokenized assets have the lowest level of on-chain nativity. A large number of tokens are merely digital certificates for offline physical assets, with actual asset control still reliant on offline ledgers and intermediary institutions.

The tokenized asset industry is still in its early developmental stage: one category consists of assets that are only formally on-chain digital records, while another comprises assets deeply integrated with blockchain characteristics as native on-chain assets.

On-chain composability technology infrastructure is already in place, and asset categories are gradually enriching, but deep integration applications have only just begun.

Future Trends for Tokenized Assets

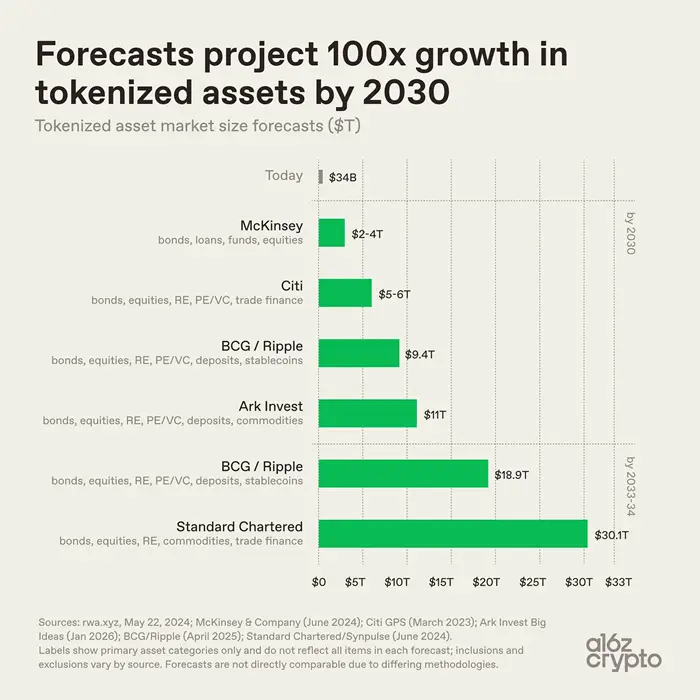

Industry predictions for the long-term scale of the tokenized asset market vary, but overall, all indicate sustained market expansion.

- McKinsey predicts the tokenized asset market will reach $2 to $4 trillion by 2030;

- Ark Invest estimates the tokenized asset market at $1.1 trillion;

- Boston Consulting Group, in collaboration with Ripple, calculates that the tokenized asset market will reach $9.4 trillion by 2030, climbing to $18.9 trillion by 2033;

- Standard Chartered forecasts that the tokenized asset market will exceed $3 trillion by 2034.

Based on the above institutional estimates, compared to the current market size of $34 billion, the tokenized asset market has a potential for hundredfold growth. Of course, the numerical differences do not stem from divergent judgments about industry adoption speed but rather from differing statistical definitions. The scopes used by various institutions vary, encompassing different asset categories, whether stablecoins and deposits are included, and the defined range of tokenization. For example: McKinsey's statistics focus on bonds, credit, funds, and stocks; Standard Chartered adds commodities and trade finance; Boston Consulting Group and Ripple additionally include deposits and stablecoins. However, despite differing statistical scopes, the industry unanimously agrees that the scale of tokenized assets will experience leapfrog expansion.

Looking at the global financial landscape, the current size of tokenized assets remains minuscule.

- The global bond market exceeds $140 trillion, while tokenized bonds are only $15.2 billion, accounting for 0.01%;

- The global market value of physical gold is in the trillions of dollars, while tokenized gold is $5 billion, less than 0.02%;

- The global stock market capitalization exceeds $100 trillion, while tokenized stocks are $1.5 billion, a mere 0.001%.

Today, emerging sectors are steadily taking shape. Assets with clear pricing, stable demand, and simple ownership like US Treasuries, gold, and private credit have been the first to achieve on-chain implementation. At this stage, tokenization has not yet overturned the underlying nature of assets; it merely optimizes asset settlement and transfer methods. The deep integration of assets with the digital financial system is still under exploration.

Currently, tokenized assets remain largely at the digitization level, with assets struggling to achieve programmable, composable applications. The industry faces a core challenge in its next phase: bringing more complex parts of the financial system on-chain and integrating tokenized assets more deeply into composable, internet-native financial infrastructure.