Author: Le Ming

A recent figure that has stunned global financial markets has emerged: the Turkish central bank sold off approximately 58.4 tons of gold in just two weeks, worth over $8 billion. Of this, 6 tons were reduced in the week of March 13, and 52.4 tons were sharply cut in the week of March 20.

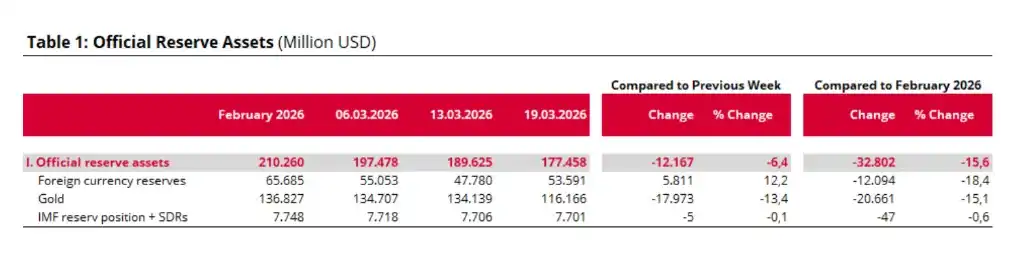

The weekly data from the Turkish central bank clearly outlines this picture: from March 13 to 19, the market value of gold reserves plummeted from $134.1 billion to $116.2 billion, evaporating nearly $18 billion in a single week; meanwhile, foreign exchange reserves (excluding gold) actually increased by $5.8 billion.

Between the decline and the rise, the traces of a "gold for foreign exchange" operation are unmistakable.

Over the past decade, Turkey has been one of the world's most aggressive gold buyers, with gold reserves rising from 116 tons in 2011 to over 820 tons.

Why suddenly sell off such hard-earned assets on a large scale within two weeks?

The answer is three words: to survive.

Trigger: A War That Pushed Turkey into a "Perfect Storm"

On February 28, the United States and Israel jointly launched a military operation codenamed "Epic Fury," launching airstrikes on Iranian nuclear facilities, military bases, and government buildings.

Iran retaliated and effectively blockaded the Strait of Hormuz—a passage for 20% of the world's seaborne oil and 20% of LNG trade.

Brent crude surged from $73 per barrel before the war to over $106, a rise of more than 40%. The International Energy Agency defined it as the "most severe global energy security challenge in history."

For most countries, this was a shock; but for Turkey, it was a survival crisis.

Turkey relies on imports for 90% of its oil and 98% of its natural gas. Every $10 increase in oil prices adds $4.5 to $7 billion to the current account deficit. Based on post-war oil prices, the annual energy import cost could surge by about $15 billion.

An even more fatal blow came on March 24—when Israel airstriked Iran's South Pars gas field, Iran subsequently halted natural gas exports to Turkey. Iran is Turkey's second-largest pipeline natural gas supplier, accounting for about 13% to 14% of its natural gas imports. The 25-year contract for this pipeline is set to expire in July 2026, and the war directly dashed prospects for renewal.

Simply put, Turkey's situation is: its energy bill suddenly doubled, a key gas source was cut off, and no equivalent replacement could be found in the short term.

Transmission Chain: Foreign Exchange Reserves Buckled First

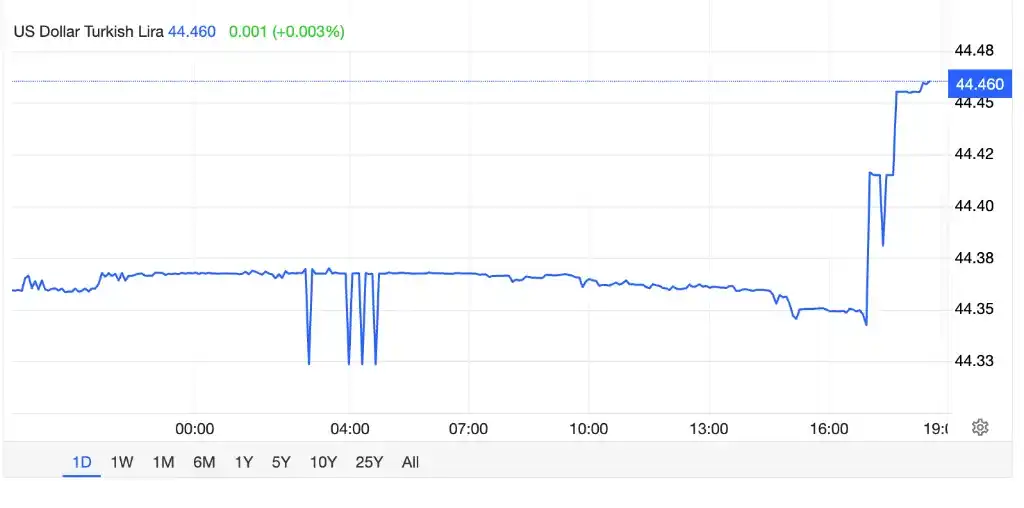

Energy imports require settlement in US dollars, so importers scrambled for dollars, and the lira plummeted.

In the 16 trading days since the conflict began, the lira hit a record low against the dollar 11 times, reaching about 44.35 lira per dollar on March 25.

Behind this was the accelerated withdrawal of foreign investors: in three weeks, foreign capital outflows from Turkish bonds reached $4.7 billion, with $1.2 billion flowing out of the stock market, while carry trade positions shrank from a record $61.2 billion in January to below $45 billion.

The Turkish central bank was thus forced to launch a "lira defense battle." In just the first week of March, it sold over $8 billion in foreign exchange. In the three weeks ending March 19, the central bank cumulatively consumed about $25 to $30 billion in foreign exchange reserves. Net reserves, after deducting swaps, plummeted from $54.3 billion before the war to $43 billion.

Turkey's weekly data fully records this process: foreign exchange reserves (excluding gold) fell from $55 billion on March 6 to $47.8 billion on March 13—first using foreign exchange ammunition. By March 19, foreign exchange reserves rebounded to $53.6 billion, but gold reserves simultaneously plummeted from $134.1 billion to $116.2 billion—foreign exchange ammunition was nearly exhausted, and gold began to be used.

This is a textbook example of an emergency defense sequence: "first use foreign exchange, then use gold."

Figure: Foreign exchange data released by the Turkish central bank

Gold Swaps: Why "Sell" Instead of "Pawn"?

The key to understanding this operation is: more than half of Turkey's gold reduction was done through swaps, not direct sales.

The essence of a gold swap is "exchanging gold for foreign exchange, with redemption upon maturity." The central bank transfers gold to the counterparty (usually a primary investment bank) in exchange for an equivalent amount of US dollars, while signing a forward contract to repurchase the gold at a slightly higher price in the future. It is a short-term financing behavior, not a permanent liquidation.

The central bank chose swaps over outright sales for at least three reasons.

First, to retain long-term positions. If the oil price surge is judged to be a temporary shock, swaps can address the urgent need, and the gold can be redeemed later, avoiding the destruction of a decade of accumulation.

Second, to reduce the impact on gold prices. Directly dumping 60 tons of gold could trigger a cliff-like plunge in the market, in turn causing a significant devaluation of its remaining over $100 billion in gold reserves. Swaps are conducted quietly in the over-the-counter market, with much less impact.

Third, a buffer at the domestic political level. Gold is an "anti-inflation totem" in the hearts of the Turkish people. Announcing large-scale gold sales could easily trigger panic, while swaps can maintain a certain degree of ambiguity technically.

This operation was completed quickly within two weeks thanks to a key pre-arrangement: Turkey stored about 111 tons of gold, worth about $30 billion, at the Bank of England. This gold could be used for foreign exchange intervention without logistical constraints—no need for cross-border physical transport, directly pledged and liquidated in the City of London.

Pressure on Gold Prices

Turkey has a historical pattern: selling gold during crises and buying back after crises.

The 2018 lira crisis, the 2020 pandemic shock, the 2023 earthquake—each time the central bank reduced gold to provide liquidity but resumed accumulation afterward. Analysts generally believe that the operation in March 2026 continues this pattern.

But this judgment has a core premise: the war cannot be prolonged.

Swap agreements come with holding costs and interest. If the war continues, energy prices remain anchored at over $100 for the long term, and Turkey's foreign exchange earning capacity cannot cover the soaring energy bill, then these "temporary swaps" will never be redeemed, effectively becoming "permanent fire sales."

Therefore, in the coming weeks, if the war continues, Turkey will need to continue turning its $135 billion in gold reserves into a lifeline.

Although Turkey prefers to "pledge" gold to obtain foreign exchange liquidity, these transactions still substantially increase the downward pressure on the gold market. In the London over-the-counter market, when the Turkish central bank transfers tens of tons of gold as collateral to international counterparties (such as investment banks) in exchange for US dollars, these financial institutions, to hedge their own position risks, typically conduct corresponding short-selling or selling operations in the spot or futures derivative markets.

Therefore, the liquidity of this batch of gold will eventually be transmitted to the market, indirectly increasing supply and depressing prices.

Conclusion

The Turkish central bank's sale of 60 tons of gold in two weeks is not panic, not speculation, but a rational self-rescue by a country highly dependent on energy imports after its ally bombed its largest energy supplier, facing the triple blow of depleted foreign exchange, a plummeting lira, and a cut-off of natural gas supply.

Figure: The market is frantically shorting the lira, partly betting that the war will not end soon and partly betting that Turkey will ultimately not hold out.

As the war prospects worsen, Turkey still needs to continue to withstand the pressure.