Another trillion-yuan market cap company.

As learned by Investment Community, today (June 26th) HKC officially listed on the Shenzhen Stock Exchange Main Board, with an issue price of 10.12 yuan per share. It opened up over 400%, with its market cap once exceeding 500 billion yuan, later fluctuating around 350 billion yuan.

Behind a small screen lies a three-decade long run in manufacturing. Founder Wang Zhiyong started from Huaqiangbei in Shenzhen, and after years of hard work, led HKC into the upstream panel sector, becoming a key player in the global display industry. Along the way, state-owned assets from Chongqing, Mianyang, Chuzhou, Guiyang, and others stood behind HKC, with BOE Technology Group's venture capital arm also appearing on the shareholder list.

Beyond HKC, more companies in Shenzhen are emerging from the depths of the industrial chain. Recently, the Shenzhen Robot Valley has gained popularity, and the "Storage Five Tigers"—Longsys, Dapu Micro, BIWIN Storage, Demingli, and Shannon Semiconductors—have reached a combined market cap in the trillion-yuan range. The next trillion-yuan market cap company is growing here.

Beginning in Shenzhen

First-Day Surge, Market Cap Once Hit 500 Billion

The story of HKC begins at Huaqiangbei.

In 1997, 27-year-old Chongqing native Wang Zhiyong headed south, starting from assembling monitors in an electronics factory, marking the beginning of HKC's own brand.

That was an era of wild growth for China's electronics manufacturing. Opportunities came fast, and淘汰 was just as swift. Wang Zhiyong later recalled that among the many enterprises that started from Huaqiangbei, few ultimately survived. HKC managed to survive by enduring the low profits and intense competition.

Over the next decade, HKC gradually grew from an OEM into a sizable finished product company, with products covering LCD TVs, LCD monitors, and more. The larger it grew, the clearer Wang Zhiyong saw the limitations of the finished goods business—thin margins, slow capital turnover, and dependence on upstream panel supply.

The turning point came in 2014. HKC, along with the Banan District Government of Chongqing, went on an inspection tour outside the region, visiting factories of AUO and Innolux. The highly automated production lines, mature factory management, and dense talent pool greatly impressed the group. That night, excitement still running high, they simply sat on the carpet discussing: Could we build a panel factory in Banan too?

This discussion later changed HKC's destiny. Subsequently, four G8.6 high-generation production lines in Chongqing, Chuzhou, Mianyang, and Changsha were successively established. HKC thus crossed over from finished product manufacturing into the more core panel segment of the display industry chain.

HKC Semiconductor Display Panel Products

Today's HKC is primarily engaged in the R&D, manufacturing, and sales of core display components like semiconductor display panels, as well as intelligent display terminals. According to Sigmaintell data, in 2024, HKC ranked third globally in TV panel shipment area, fourth in monitor panel shipment area, and third in smartphone panel shipment area; it ranked first globally in shipment area for 85-inch LCD TV panels.

This is not HKC's first attempt at entering the capital market. As early as 2022, HKC aimed for a ChiNext board IPO, planning to raise 9.5 billion yuan. At that time, the global display industry was in a downturn cycle. Affected by factors like panel price fluctuations, HKC reported a net loss of 2.093 billion yuan that year, stalling its listing process. In August 2023, HKC voluntarily withdrew its ChiNext IPO application.

From Huaqiangbei to the global top three, to ringing the bell at the Shenzhen Stock Exchange, HKC's journey has taken nearly three decades.

A Long Accompanying Run

State-Owned Capital Reaps a Super Return

HKC's ability to reach the IPO stage relies on a sufficiently large business.

The prospectus shows that from 2023 to 2025, HKC achieved revenues of approximately 35.824 billion yuan, 40.282 billion yuan, and 40.897 billion yuan, respectively. The net profit attributable to shareholders for the same periods was approximately 2.582 billion yuan, 3.320 billion yuan, and 3.801 billion yuan, respectively. Among these, semiconductor display panels consistently remained its core revenue source, accounting for over 70% during the reporting period; intelligent display terminal revenue remained stable at around one-quarter.

On one side is the panel business closer to the upstream of the industry chain, and on the other is the terminal manufacturing capability carried over from the finished product era, forming HKC's fundamental business base.

The customer list is telling. During the reporting period, sales revenue from HKC's top five customers was approximately 15.353 billion yuan, 16.280 billion yuan, and 15.299 billion yuan, accounting for roughly 40% of total revenue. These customers include well-known brands such as Samsung, TCL, Hisense, LG, Xiaomi, and Skyworth.

For a panel company, consistently entering the supply chains of top-tier manufacturers itself validates production capacity, delivery, and cost-control capabilities. This is also why local state-owned capital was willing to continue betting on it.

Display panels are a typical heavy-asset business. Production lines require large investments, have long construction cycles, and demand high capital. However, once established, they can drive entire chains involving materials, modules, terminal manufacturing, and supporting services. For local governments, introducing a panel company often means landing an entire industry chain.

The prospectus shows that since 2015, HKC successively partnered with state-owned capital platforms of local governments in Chongqing, Chuzhou, Mianyang, Changsha, etc., to jointly invest in establishing project companies, which then built four production lines. In its response to the Shenzhen Stock Exchange's inquiry letter, HKC described this model as an industry common practice, namely "using a combination of self-owned funds and state-owned or market-oriented capital for production and operation."

This model also extended into the pre-IPO equity structure. First, in 2020, Miantou Group, Liuyang Urban Construction, and Hunan Jinyang participated in HKC's capital increase.

In March of the following year, BOE Technology Group Venture Capital invested. This investment was significant: a domestic panel industry leader appeared on the shareholder roster of the industry's third-ranked player.

Subsequently, local state-owned capital continued to increase their stakes. In December 2023, HKC increased its capital by introducing Chuzhou Cheng tou (Chuzhou City Investment) and Chuzhou Tongchuang. Among them, Chuzhou Cheng tou subscribed to HKC shares with its equity in Chuzhou HKC valued at 1.151 billion yuan, and Chuzhou Tongchuang subscribed with its equity in Chuzhou HKC valued at 352 million yuan.

A year later, more local state-owned capital entered. In December 2024, HKC increased its capital by introducing shareholders such as Gui'an Industrial Development Company, Science and Innovation City Industrial Fund, Miantou Group, and Mianyang Fucheng.

Among them, Gui'an Industrial Development Company invested 2 billion yuan, Science and Innovation City Industrial Fund invested 1 billion yuan, Miantou Group invested 2.4 billion yuan, and Mianyang Fucheng invested 50 million yuan. Within a short month, state-owned platforms from Guizhou, Mianyang, and others invested a total of 5.45 billion yuan.

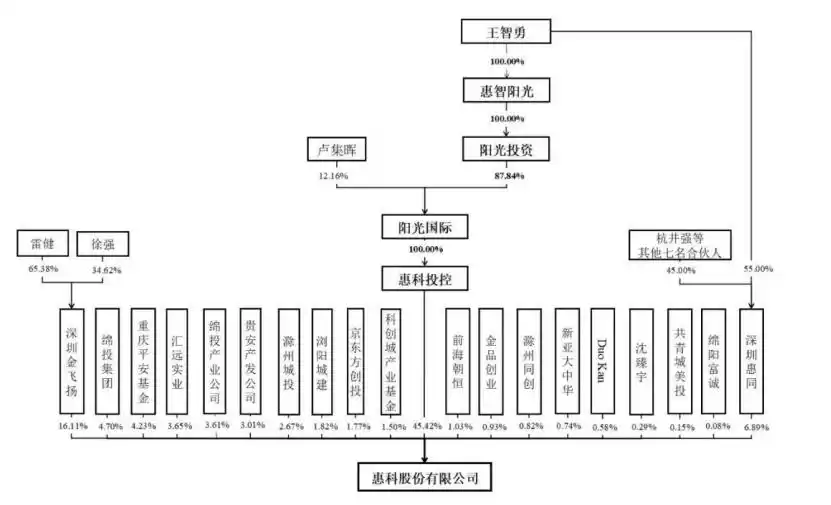

The prospectus shows that HKC is still helmed by Wang Zhiyong. Pre-IPO, he controlled 52.31% of the company's voting rights through HKC Investment Holdings and Shenzhen Huitong. Shenzhen Jinfly, Miantou Group, Chongqing Ping'an Fund, Miantou Industry Company, Gui'an Industrial Development Company, and other shareholders follow.

From Chongqing and Mianyang to Guizhou and Chuzhou, HKC's shareholder list almost maps out a local industrial landscape. Now, with HKC's successful IPO, a long bet on industrial collaboration has finally yielded a stage of returns.

A Bursting Scene

Shenzhen's Five Tigers with Trillion-Yuan Market Cap

Viewed within Shenzhen's innovation and technology landscape, HKC's IPO seems more like a footnote.

For a long time, when discussing Shenzhen-listed companies, the outside world first thought of giants like Tencent, BYD, Mindray Medical, and China Merchants Bank. They support the city's most prominent facade in the capital market and give Shenzhen a group of truly trillion-yuan and hundred-billion-yuan companies.

In fact, Shenzhen is presenting another facet. At the Summer Davos Forum held this week, Premier Li Qiang mentioned Shenzhen's Robot Valley half-hour supporting circle.

This "Robot Valley," located in Shenzhen's Nanshan District, stretches approximately 15 kilometers east-west along Liuxian Avenue, connecting key parks like Nanshan Zhiyuan, Zhigu, and International Innovation Valley, covering an area of about 28 square kilometers. It gathers many listed companies in the robotics industry chain, leading enterprises in细分 fields, and nearly 10 universities.

Among them, Ubtech's latest market cap is nearly 50 billion HKD, Dji's latest market cap is 11.5 billion HKD, and valuations for companies like Zhongqing, Paxini, Zhipingfang, and Zibianliang have also all exceeded 10 billion yuan. Shenzhen is thus pushed into the spotlight as the "first city for humanoid robots."

Then there's storage chips, where a group of capital market stars have grown in this细分赛道. Longsys, Dapu Micro, BIWIN Storage, Demingli, and Shannon Semiconductors are called the "Storage Five Tigers" of Shenzhen. In this market cycle, the combined market cap of these five companies has reached the trillion-yuan level.

Looking further out, Shenzhen's hard tech puzzle is continuing to expand: storage, robotics, 3D printing, lithium batteries, new displays, low-altitude economy... Not every company may rapidly grow into a trillion-yuan company, but together they constitute Shenzhen's new industrial depth.

As outlined in Shenzhen's "Fifteenth Five-Year" Plan, it aims to vigorously develop emerging pillar industries such as AI terminals, low-altitude economy, embodied intelligent robots, ocean economy, commercial space, etc., targeting a strategic emerging industry added value exceeding 2.3 trillion yuan by 2030.

Behind this is the evolution of Shenzhen's innovation ecosystem. In the past,超级 companies defined a city's industrial height; now, more and more细分 champions are emerging from within the industry chains.

Where is the next trillion-yuan market cap company?

The answer may not appear immediately. But in such industrial soil, the seeds of industrial giants have already broken ground.

This article is from the WeChat public account "Investment Community" (ID: pedaily2012), author: Wang Lu