⠀

The question at hand is whether the current price for Bitcoin is at the “bottom”. Bitcoin is the purest and most battle-tested form of crypto money — and while it may not fall the most, its role as crypto’s reserve asset will ensure that it’s Bitcoin that leads us out of the shadow of darkness. Therefore, we must focus on Bitcoin’s price action to divine whether this market’s bottom has occurred or not.

⠀

There are three cohorts that were forced to puke their Bitcoin into the righteous hands of the true believers: the centralised lending and trading firms, Bitcoin mining operations, and ordinary speculators. In every case, misuse of leverage — whether it was in their business operating model or they used it to finance their trades — was the cause of the liquidations. With short-term US Treasury yields moving from 0% in Q3 2021 to 5% at present, everyone has suffered bigly for their uber-bullish convictions.

⠀

After walking through how leverage destroyed each cohort’s position as rates rose, I will then explain why I think they have no more Bitcoin left to sell — And why, therefore, at the margin, we likely already hit the lows of this cycle during the recent FTX / Alameda catastrophe.

⠀

In the final section of this essay, I will then lay out the way in which I plan to trade this possible bottom. To that end, I recently participated in a webinar with my macro daddy Felix Zulauf. At the end of the broadcast, he said something that hit home. He said that investors and traders need to be concerned with recognising the tops and bottoms, but that most focus on the noise in the middle, and that calling a bottom is usually a fool’s errand. Since I’m embarking on that very fool’s errand, I intend to try to call it in a way that protects my portfolio, with the maximum amount of cushion to be wrong on the level and/or timing.

⠀

With that in mind, let’s dive in.

⠀

Bankruptcy Order of Operations

⠀

Most of us are probably not as gifted as Caroline Ellison, so we had to learn maths the hard way. Do you remember PEMDAS? It’s the acronym that describes the order of operations when solving equations:

⠀

P — Parentheses

E — Exponents

M — Multiplication

D — Division

A — Addition

S — Subtraction

The fact that I still remember this acronym many decades after first learning it speaks to its sticking power.

⠀

But equations aren’t the only thing with a static order of operations — bankruptcies (and the contagion that follows) occur in a very specific order, too. Let me start by explaining what that order looks like, and why it occurs in that sequence.

⠀

Before I do, though, I want to acknowledge that no one wants or intends to go bankrupt. So, I apologise in advance if I come across as insensitive to the strife of those who lost money because of Sam “I mislabeled my bank accounts” Bankman-Fried (SBF). But, this scammer just keeps opening his mouth and saying dumb shit that he needs to be called out for — so the rest of this essay will be peppered with references to our “right kind of white” boy and the sad melodrama he is responsible for. Now, let’s get back to it.

⠀

Centralised lending firms (CEL) usually go bankrupt because they either lent money to entities that can’t pay them back, or they have duration mismatches in their lending books. Duration mismatches occur because the lenders receive deposits that can be recalled by their depositors on a short time frame, but they make loans using those deposits on a longer time frame. If the depositors want their money back or demand a higher rate of interest due to changing market conditions, then the CEL — absent an injection from some white knight firm — becomes insolvent and bankruptcy quickly follows.

⠀

Before a CEL becomes insolvent or goes bankrupt, they will attempt to raise funds to ameliorate the situation. The first thing they will do is call all loans that they can. This mainly affects anyone who borrowed money from them with a short time horizon.

⠀

Imagine you are a trading firm that borrowed money from Celsius — but within a week, Celsius asks for those funds back, and you have to oblige. As a trading firm, getting recalled in a bull market is no biggie. There are plenty of other CELs who will lend you funds so that you don’t have to liquidate your existing positions. But when the bull market fades and there’s a market-wide credit crunch, all CELs typically recall their loans at around the same time. With no one to turn to for additional credit, trading firms are forced to liquidate their positions to meet capital calls. They will liquidate their most liquid assets first (i.e., Bitcoin and ETH), and hopefully their portfolio doesn’t contain too many illiquid shitcoins like Serum, MAPS, and Oxygen (*cough* Alameda and 3AC *cough*).

⠀

After a CEL recalls all the short-term loans that it can, it will begin liquidating the collateral that underpins its loans (assuming it actually asked for any — looking at you, Voyager). In the crypto markets, the biggest collateralised lending category prior to the recent implosions was loans secured by Bitcoin and Bitcoin mining machines. So once things start to go south, CELs start by selling Bitcoin, as it’s the asset most used to collaterlise loans AND it’s the most liquid cryptocurrency. They also turn to the mining firms that they have lent to and ask them to pony up either Bitcoin, or their mining rigs — but if those CELs don’t operate a data centre with cheap electricity, the mining rigs are about as useful as SBF’s accounting skills.

⠀

So while the credit crunch is ongoing, we see large physical sales of Bitcoin hitting the centralised and decentralised exchanges from both a) CELs trying to avoid bankruptcy by selling the Bitcoin they have received as collateral, and b) trading firms who have seen their loans recalled and must liquidate their positions. This is why the price of Bitcoin swoons BEFORE CELs go bankrupt. That’s the big move. The second move down — if there is one — is driven by the fear that occurs when firms which were once thought to be unshakable suddenly start posturing as zombies that are on the cusp of liquidating their assets. This tends to be a smaller move, as any firms at risk of bankruptcy are already busy liquidating Bitcoin so that they can survive the crash.

⠀

⠀

The above chart of Binance’s BTC/BUSD trading volume illustrates that volumes spiked during the two credit crashes of 2022. It is in this span of time that all these once storied firms bit the dust.

⠀

To summarise, as CELs transition from solvency, to insolvency, to bankruptcy, these other ecosystem players are affected:

⠀

1. Trading firms who borrowed short-term money from CELs and saw their loans recalled.

2. Bitcoin mining firms who borrowed what was typically fiat collateralised by either Bitcoin on their balance sheet, future Bitcoin to be mined, and/or Bitcoin mining rigs.

⠀

The two largest muppet crypto trading firms, Alameda and 3AC, both grew to such a gargantuan size because of cheap borrowed money. In the case of Alameda, the polite way to put it is that they “borrowed” it from FTX customers — although others might call it theft. In the case of 3AC, they hoodwinked gullible and desperate CELs to lend them funds with little-to-no collateral. In both cases, the lenders believed these and other trading firms were engaged in super-duper-smart arbitrage trades that rendered these firms immune to the vicissitudes of the markets. However, we know now these firms were just a bunch of degen, long-only punters in meth mode. The only difference between them and the masses was that they had billions of dollars to play with.

⠀

When these two firms got into trouble, what did we see? We saw large transfers of the most liquid cryptos — Bitcoin (WBTC in DeFi) and Ether (WETH in DeFi) — to centralised and decentralised exchanges that were then sold. This happened during the big move down. When the dust settled and neither firm could boost the asset side of their balance sheet higher than the liability side, their remaining assets consisted almost purely of the most illiquid shitcoins. Looking through the bankruptcy filings of centralisd lenders and trading firms, it is not entirely obvious what crypto assets remain. The filings lump everything together. So I can’t demonstratively prove that all Bitcoin held by these failed institutions was sold during the multiple crashes, but it does look as if they tried their best to liquidate the most liquid crypto collateral they could right before they went under.

⠀

The CELs and all large trading firms already sold most of their Bitcoin. All that is left now are illiquid shitcoins, private stakes in crypto companies, and locked pre-sale tokens. It’s irrelevant to the progression of the crypto bear market how a bankruptcy court eventually deals with these assets. I have comfort that these entities have little to no additional Bitcoin to sell. Next, let’s look at the Bitcoin miners.

⠀

Bitcoin Mining Firms

⠀

Electricity is priced and sold in fiat, and it is the key input to any Bitcoin mining business. Therefore, if a mining firm wants to expand, they either need to borrow fiat or sell Bitcoin on their balance sheet for fiat in order to pay their electricity bills. Most miners want to avoid selling Bitcoin at all costs, and therefore take out fiat loans collateralised by either Bitcoin on their balance sheets, yet-to-be-produced Bitcoin, or Bitcoin mining rigs.

⠀

As Bitcoin’s price rises, lenders feel emboldened to lend more and more fiat to mining firms. The miners are profitable and have hard assets to lend against. However, the ongoing quality of the loans is directly connected to Bitcoin’s price level. If the Bitcoin price falls quickly, then the loans will breach minimum margin levels before the mining firms can earn enough income to service the loans. And if that happens, the lenders will step in and liquidate the miner’s collateral (as I described in the previous section).

⠀

We anecdotally know this happened because the massive downturn in asset prices, particularly in the crypto bear market, have — along with rising energy prices — squeezed miners across the industry. Iris Energy is facing a default claim from creditors on $103M of equipment loans. September saw the first Chapter 11 bankruptcy from a major player, Compute North, with other big firms including Argo Blockchain (ARBK) seemingly teetering on the edge of solvency.

⠀

But, let’s look at some charts to examine how these waves of crypto credit crunches affected the miners and what they did in response.

⠀

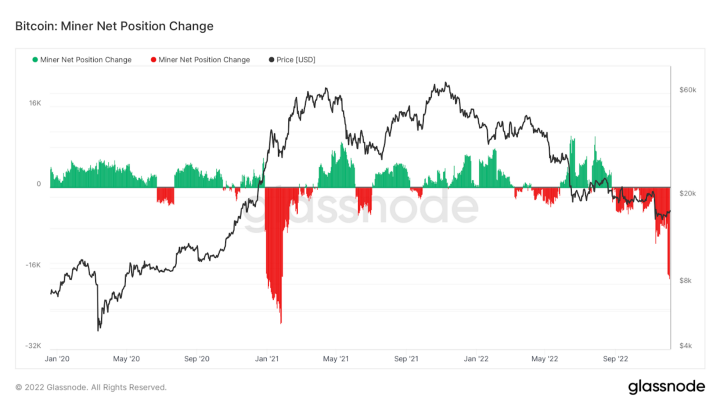

Glassnode publishes an excellent chart which shows the net 30-day change in Bitcoin held by miners.

⠀

⠀

As we can see, miners have been net selling a large amount of Bitcoin since the first credit crunch in the summer. They must do this in an attempt to stay current on their big fiat debt loads. And if they don’t have debt, they still need to pay electricity bills — and since the price of Bitcoin is so low, they have to sell even more of it to keep the facility operational.

⠀

While we don’t — and never will — know if we have hit the maximum amount of net selling, at least we can see that the mining firms are behaving as we would expect given the circumstances.

⠀

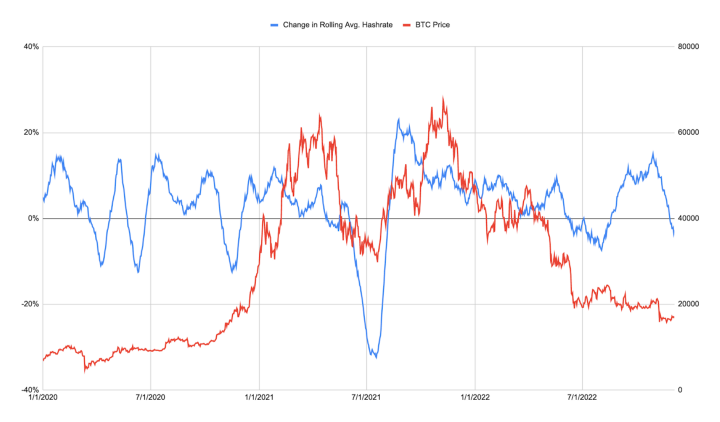

Some miners didn’t make it, or they had to downsize their operations. That is evident in the change in hashrate. I took the hashrate and first computed a rolling 30-day average. I then took that rolling average and looked at the 30-day change. I did this because the hashrate is quite volatile, and it needed some smoothing.

⠀

⠀

In general, the hashrate has trended higher over time. But, there are periods where the 30-day growth is negative. The hashrate declined right after the summer meltdown, and then most recently plunged due to the FTX / Alameda fallout. Again, this confirms our theory that miners will downsize operations when there is no more credit available to fund their electricity bills.

⠀

We also know that some high-cost miners had to cease operations because they defaulted on their loans. Any lender who took mining machines as collateral will likely find it difficult to make use of them, since they aren’t already in the business of operating data centres. And since they can’t use them, the lenders must then sell these machines in the secondary market, and that process takes time. This also contributes to the hashrate falling for a period of time.

⠀

⠀

This is a chart of the price of a Bitmain S19 or other comparable mining machine with under 38 Joules (J) / Terahash (TH) efficiency. As we can see, the collateral value of an S19 has plummeted alongside the price of Bitcoin. Imagine you lent USD against these rigs. The miners you lent to tried to sell Bitcoin to provide more fiat to service your loan, but in the end couldn’t do so because marginal profitability declined. The miners then defaulted on their loans and handed over their machines — which are worth almost 80% less now than when the loan was undertaken — as repayment. We can guess that the most feverish point of loan origination was near the top of the market. Muppet lenders always buy the top and sell the bottom … every single fucking time!

⠀

Now that CELs have collections of mining rigs that they can’t easily sell and can’t operate, they can try to sell them and recover some funds — but it’s going to be single digit cents on the dollar, given that new machines are trading 80% off from a year ago. They can’t operate a mining farm because they lack a data centre with cheap electricity. And that’s why the hashrate just disappears — because of an inability to turn the machines back on.

⠀

Going forward, if we believe that most — if not all — mining loans have been extinguished, and there is no new capital to be lent to miners, then we can expect miners to sell most — if not all — of the block reward they receive.

⠀

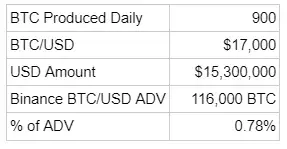

⠀

As the table above shows, if miners sold all the Bitcoin they produced each day, it would barely impact the markets at all. Therefore, we can ignore this ongoing selling pressure, as it is easily absorbed by the markets.

⠀

I believe that the forced selling of Bitcoin by CELs and miners is over. If you had to sell, you would have already done so. There is no reason why you would hold on if you had an urgent need for fiat to remain a going concern. Given that almost every major CEL has either ceased withdrawals (pointing to insolvency at best) or gone bankrupt, there are no more miner loans or collateral to be liquidated.

⠀

Small Scale Speculators

⠀

These punters are your run-of-the mill traders. While many of these individuals and firms definitely imploded, the failure of these entities would not be expected to send massive negative reverberations through the ecosystem. That being said, their behaviour can still help us form a guess as to where the bottom is.

⠀

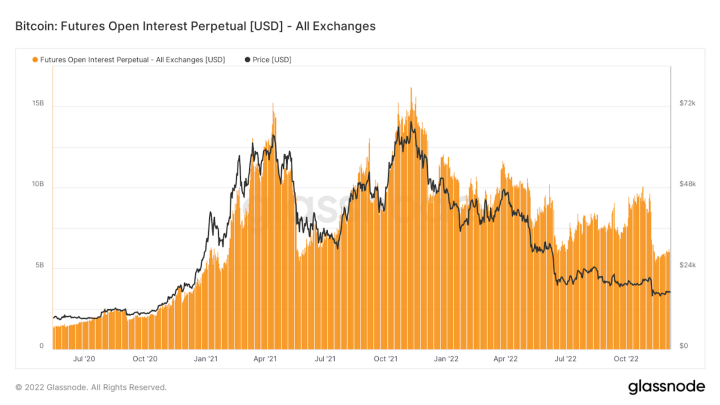

The Bitcoin / USD perpetual swap (invented by BitMEX) is the most traded of any crypto instrument. The number of open long and short contracts — called the open interest (OI) — tells us how speculative the market is. The more speculative it is, the more leverage is being used. And as we know, when the price changes directions quickly, it leads to large amounts of liquidations. In this case, the all-time high in OI coincided with the all-time high of Bitcoin. And as the market fell, longs at the margin got liquidated or closed their losing positions, which resulted in OI falling, too.

⠀

⠀

Taking a look at the sum of OI across all major crypto derivatives centralised exchanges, we can see that the OI local low also coincided with the sub $16,000 stab of Bitcoin on Monday November 14th. Now, the OI is back to levels not seen since early 2021.

⠀

The timing and magnitude of the reduction of the OI leads me to believe that most of the over-leveraged long positions have been extinguished. What remains are traders using derivatives as a hedge, and those using very low leverage. This gives us a bedrock to move higher.

⠀

Could the OI fall further as we enter the sideways, non-volatile part of the bear market? Absolutely. But the OI’s rate of change will slow, which means chaotic trading periods featuring large amounts of liquidations (particularly on the long side) are not likely to occur.

⠀

Timing Re-entry

What I Don’t Know

⠀

I don’t know if $15,900 was this cycle’s bottom. But, I do have confidence that it was due to the cessation of forced selling brought on by a credit contraction.

⠀

I don’t know when or if the US Federal Reserve will start printing money again. However, I believe the US Treasury market will become dysfunctional at some point in 2023 due to the Fed’s tightening monetary policies. At that point, I expect the Fed will turn the printer bank on, and then boom shaka-laka — Bitcoin and all other risk assets will spike higher.

⠀

What I Do Know

⠀

Everything is cyclical. What goes down, will go up again.

⠀

I like earning close to 5% by investing in US Treasury bills with durations shorter than 12 months. And therefore, I want to be earning a yield while I wait for the crypto bull market to return.

⠀

What to Do?

⠀

My ideal crypto asset must have beta to Bitcoin, and to a lesser extent, Ether. These are the reserve assets of crypto. If they are rising, my asset should rise by at least the same amount — this is called crypto beta. This asset must produce revenue that I can claim as a token holder. And this yield must be much greater than the 5% I can earn buying 6- or 12-month treasury bills.

⠀

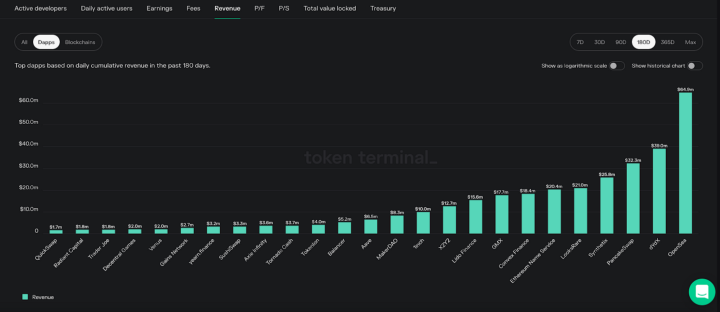

I have a few super-powered assets such as GMX and LOOKS in my portfolio. This is not the essay where I go into why I will be opportunistically selling my T-bills and purchasing these during the upcoming months of the hopefully sideways bear market. But if you want to start down the path towards finding the right asset to both participate in the upside and earn income while you wait for the return of the bull market, pull up a site like Token Terminal and look at which protocols generate actual revenue. It is then up to you to investigate which protocols have appealing tokenomics. Some may earn a lot of revenue, but it is very hard for a token holder to extract their share of that revenue to their own wallet. Some protocols pay out a majority of revenue continuously, directly to token holders.

⠀

⠀

The best part about some of these projects is that all things DeFi got shellacked during the two downward waves of the 2022 crypto credit crunch. Investors threw out good projects along with the bad as they rushed to raise fiat to repay loans. As a result, many of these projects trade at a truely bombed out price to fees (P/F) ratio.

⠀

If I can earn 5% in treasuries, then I should at least earn 4x of that — i.e., 20% — when purchasing one of these tokens. A 20% per annum yield means I should only invest in projects with a P/F ratio of 5x or lower. Everyone will have a different hurdle rate, but that is mine.

⠀

I could purchase Bitcoin and or Ether, but neither of these cryptos pays me enough yield. And if I’m not getting sufficient yield, I’m hoping that the price appreciation in fiat terms will be stupendous when the market turns. While I do believe that will occur, if there are cheaply priced protocols where I get the return profile of Bitcoin and Ether plus yield from the actual usage of the service, happy days!

⠀

Investing at what you think is the bottom is certainly risky. You are out there all alone, spreading the good word of Satoshi against the sweet siren song of the TradFi devil and their harpies. But be not afraid, intrepid and righteous warrior, for to the faithful the spoils of war shall accrue.