Binance 与 FTX 的剧情在一夜间经历了两次翻转,从争论到收购再到监管的不确定性,整个大盘也随之短暂上涨后又急剧下跌。BNB 在昨夜一度冲到 398 USDT,后又下跌至 326 USDT;FTT 在经历了昨天一天的下跌后上涨至 21 USDT,而后狂跌至 6.1 USDT,最低跌至 2.5 USDT 附近,24H 跌幅 75%,距离崩盘只差一步之遥。受该事件影响,BTC 从 20700 USDT 下跌至 18466 USDT,ETH 也从 1579 USDT 下跌至 1325 USDT。其它 FTX 关联代币和山寨币都有约 10%-20% 的跌幅。由此可见,FTX 目前所面临的流动性紧缩问题(以及会造成的影响)可能比预想还要严重。

“”

目前,就大家都比较关心的 FTX 及 Alameda Research 的债务问题,RWA.xyz 通过数据分析了后者在 DeFi 领域的债务情况。

“”

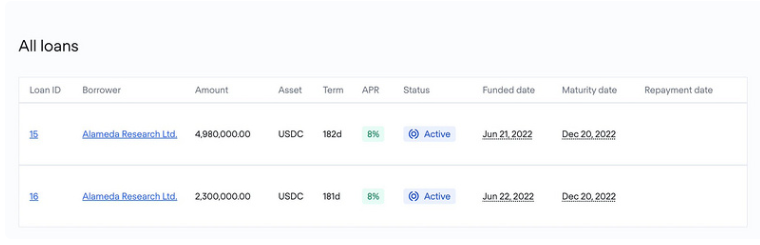

首先,有 728 万美元贷款来自 TrueFiDAO pool,他们在一周前成功支付了利息,但本金将在 50 天内到期。

乐观来看,Alameda 仍有 476 万美元的闲置资金。但不幸的是,储户似乎已经在可能会出现拖欠还款之前就开始撤出资金。

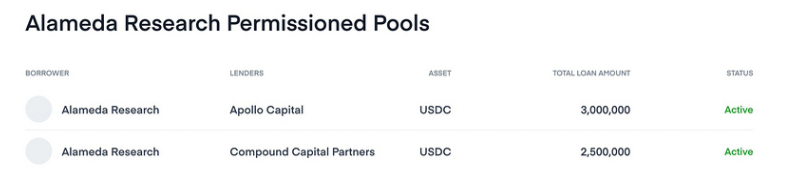

550 万美元贷款是 Alameda 于 2016 年 9 月 15 日从 ClearpoolFi pool 2 借出的 ,放款方:Apollo 和 Compound。由于 Clearpool 的机制设计,Alameda 既不需要支付利息,也没有设定的到期日。

“”

且 Alameda 的流动性问题正在蔓延到加密贷方,多家机构加密资本公司在 Clearpool 上的信贷池达到了最大值。Amber Group、Auros 和 LedgerPrime 在 Clearpool 上各自的 Polygon Permissionless Pools 上收到了“警告”标签,因为它们达到了协议上可使用的最大信用额度的 99%。Folkvang 和 Nibbio 在他们的以太坊无许可池上也收到了“警告”状态。Clearpool 的贷款仪表盘显示,这些贷款的债务总额为 1,480 万美元。

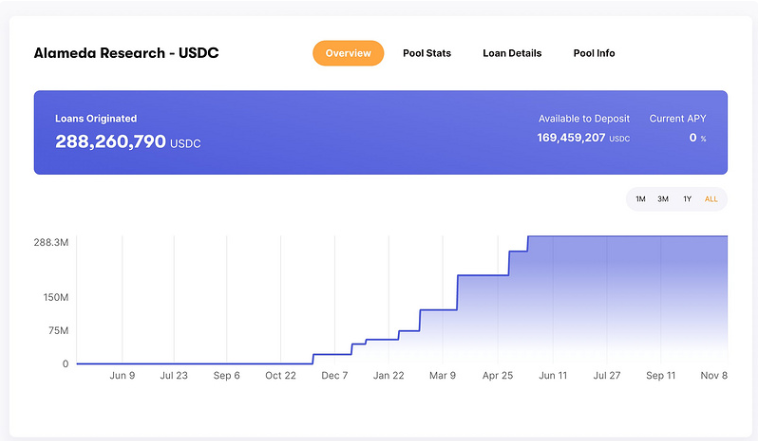

MapleFinanc 向他们提供近 3 亿美元贷款的资金池,但目前没有活跃的贷款。

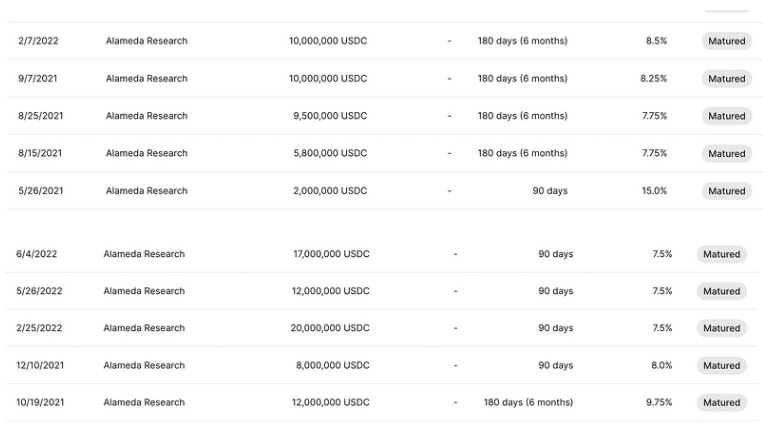

下面是由 Ortho Credit 和 M11 Credit 管理的 Maple pools,尽管 Alameda 在过去有超过 1 亿美元的贷款,但没有未偿还贷款。

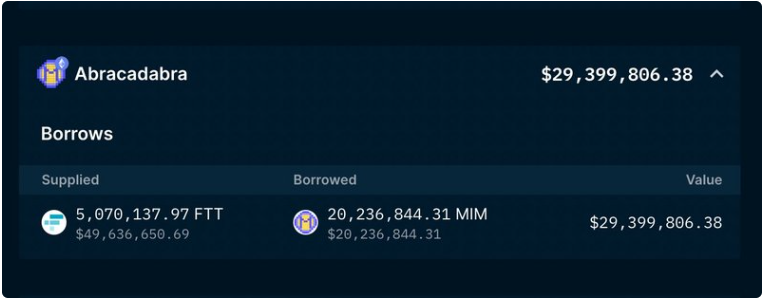

Alameda 还用价值 5000 多万美元的 FTT 借了 2000 多万 MIM 代币。这可能只是 DeFi 借贷市场上无数个类似头寸中的一个,由于其超额抵押的性质,这些头寸的损失可能会很小。

回顾三箭资本破产期间,像 Genesis 这样的贷款机构公开向 3AC 提出索赔。而切换到 DeFi 世界中,我们可以更确切地看到风险敞口是多少。