10月26日周三美股盘后,去年10月将母公司更名为 “元宇宙平台”的社交媒体和数字广告巨头Facebook公布了2022财年第三季度财报。

在数字广告支出疲软的宏观经济逆境和TikTok等激烈竞争中,Meta连续第二个季度收入同比下跌,二季度曾创下公司史上首次季度营收同比回落,三季度财报显示收入降幅正在加速。

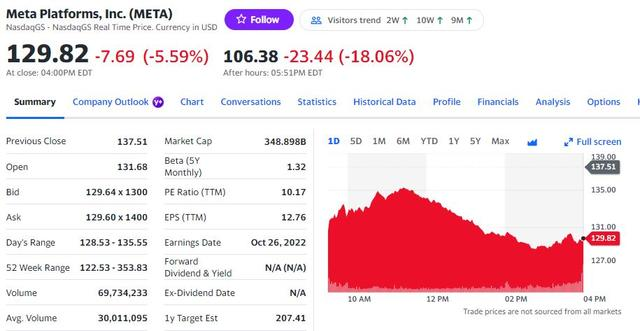

由于应用程序家族的活跃用户数超预期,Meta盘后一度涨8%,随后因其他财报指标和四季度指引不佳而快速转跌,大跌近20%,股价刷新2016年来最低,下逼114美元至2016年以来最低。有分析称,鉴于经济环境,Meta的支出远高于投资者预期或认为合适的水平,是其股价暴跌的重要原因。

Meta周三收跌5.6%,重新逼近2018年末以来低位,今年累跌超61%,同期标普500指数跌约20%、纳指跌约30%。今年或迎来Meta公司历史上最差的股价年度表现。

由于来自TikTok的竞争加剧,以及苹果更改隐私设置均影响了Meta的广告市场份额,今年以来公司市值蒸发超5500亿美元,股票市盈率降至11.4倍,在大型科技股中垫底。

Meta连续四个季度利润下降,收入连续两个季度同比下跌,元宇宙收入腰斩、亏损扩大

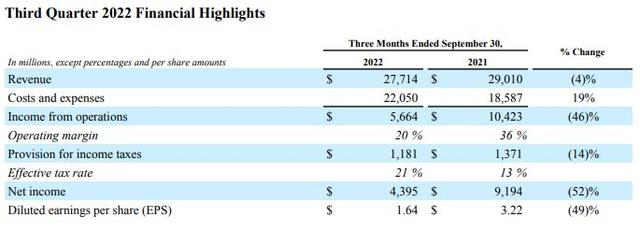

财报显示,三季度Meta营收277.1亿美元,同比下跌4%,且逊于市场预期的274亿美元,跌幅较二季度的同比回落1%加速。

调整后EPS为每股收益1.64美元,远逊于预期的1.89美元,同比下滑49%、接近腰斩。净利润43.95亿美元,同比降52%,代表公司利润连续第四个季度下降,为2012年四季度以来首次。

元宇宙核心项目Reality Labs三季度收入2.85亿美元,同比下跌49%,市场预期4亿美元。运营亏损36.7亿美元,去年同期亏损26.3亿美元,预期亏损30.9亿美元。今年前三季度该部门已亏损94亿美元,去年曾亏损超过100亿美元,这代表“元宇宙”押注的损失今年会更深。

由于Meta收入的主体广告来自其社交媒体和通讯App家族(Facebook、Instagram、Messenger、WhatsApp 和其他服务),市场聚焦关键用户增长数据:

三季度Facebook主程序的日活用户数19.8亿,持平预期,同比增3%,也高于二季度的19.7亿。更受关注的月活用户29.6亿,高于预期的29.4亿,同比增2%,二季度为29.3亿。

全应用家族的日活用户29.3亿,同比增4%,较二季度的28.8亿增长明显,月活用户37.1亿,同比增4%,二季度为36.5亿。

但衡量货币化用户群能力的另一核心指标:每用户平均收入(ARPU)为9.41美元,同比跌6%,低于预期的9.83美元,也低于二季度的9.82美元,令营业利润率从去年同期的36%降至20%。

三季度广告收入272.4亿美元,占总营收的比重为98.3%,高于市场预期的97.8%。广告收入同比降3.7%,好于市场原本预期的降近5%至269亿美元。尽管应用程序家族中投放的广告展示次数(ad impressions)同比增17%,但单位广告平均价格同比降18%。

四季度收入指引不佳,预计明年底的员工人数与现在持平,元宇宙亏损同比大幅增长

除了三季度财报除用户增长之外的主要指标均不佳,Meta给出的四季度业绩指引也令人失望。

公司预计今年四季度总收入在300亿至325亿美元区间,市场的中位数预期为322亿美元,美元升值带来的汇率波动将拖累收入7%。而三季度若按照固定汇率计算,营收原本同比增2%。

三季度成本和支出同比增19%至220.5亿美元,公司预计2022年总支出在850亿至870亿美元,低于此前预期的区间上限为880亿美元。其中,四季度存在与办公设施相关的9亿美元额外费用。

预计2023全年的总支出在960亿至1010亿美元,包括约20亿美元与合并办公场所有关的费用,“我们办公室空间的持续合理化,将在短期内导致成本增加。”

公司称,2023年底的员工人数预计与今年三季度末持平,“正在全面作出重大改变以提高运营效率”。截至今年9月30日,员工人数为8.73万人,同比增长了28%。

明年的收入成本增长预计将加速,主要受基础设施相关费用的推动,也与“明年晚些时候推出下一代消费者级Quest头显带来的Reality Labs硬件成本”有关。

Meta直言,尽管预计Reality Labs在2023年的运营亏损“将同比大幅增长”,但2023年之后将继续加快对这一业务的投资步伐,以便能够实现从长期增加分公司整体营业利润的目标。

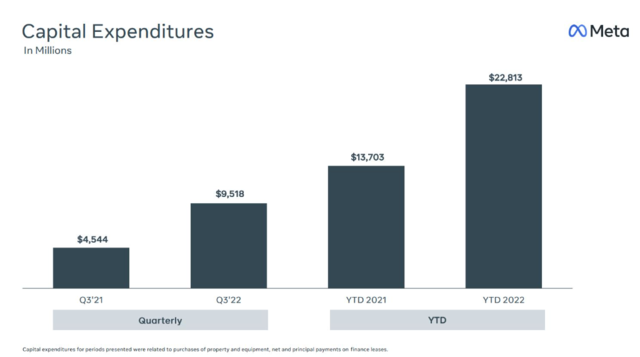

除了继续“All IN”元宇宙,人工智能的产能增长也将推高2023年大部分的资本开支增速。公司预计今年资本支出在320亿至330亿美元,高于此前预期的300亿至340亿美元。由于投资数据中心、服务器和网络基建,预计2023年资本支出进一步扩大至340亿至390亿美元。

在电话会上,Meta创始人兼CEO扎克伯格为大力投资发展元宇宙和AI辩护称,“我们显然在做一些领先的工作,那将为下一个重大的计算平台做铺垫工作。”

而继几周前任职了14年的COO Sheryl Sandberg离职后,过去8年担任首席财务官的David Wehner今日证实将于11月离职,这令Meta股价在盘后跌幅扩大至18%,失守107美元。

华尔街对今明两年Meta前景存疑,重量级股东要求对元宇宙投资砍半

分析指出,华尔街对Meta今明两年的前景持怀疑态度。

公司曾在2月警告称,苹果iOS操作系统隐私规则变更将令Meta在2022年损失约100亿美元收入。与此同时,Meta在虚拟现实和“元宇宙”方面的大量投资尚未得到回报,试图与TikTok抗衡的短视频Reels业务也仍处在创收早期,这代表短期内公司收入增长会保持失速状态。

媒体看到的内部文件显示,Meta旗下的Instagram用户每天累计花费1760万小时观看Reels短视频,不到TikTok用户每天在该平台上花费的1.978亿小时的十分之一。

而Meta面向消费者的旗舰元宇宙产品Horizon Worlds月活用户不到20万,不仅低于公司原定的到今年年底 50 万用户的目标,也逊于已经被砍半下调后的目标28万。10月初推出的价值1500美元Quest Pro虚拟现实头显,因过于昂贵和用途有限而没有斩获太多火花。

在三季报发布前,美国银行将Meta评级从“买入”下调至“中性”,认为2023年初的广告商预算削减将打压市场情绪,为苹果隐私规则变更和Reels变现初期的Meta增加不确实性,而且“在经济衰退的场景中,普遍存在一些下行风险”。

本周,股东Altimeter Capital的CEO Brad Gerstner发表公开信,要求小扎带领Meta“重获股东信任和留住技术人才”,除了要求削减成本20%,还希望将对元宇宙的投资砍半至每年50亿美元,代表重量级股东愈发对Meta押注元宇宙的战略感到不满:

“Meta 的核心业务社交媒体是全球规模最大、利润最高的业务之一,仅去年的营业利润就超过 450 亿美元。此外,Meta在人工智能和沉浸式3d等关键未来技术方面拥有行业领先的能力,这将有助于推动新产品和未来的增长。Meta需要削减成本来瘦身和重新聚焦业务重点。”