Original | Odaily Planet Daily (@OdailyChina)

Author | Azuma (@azuma_eth)

At midnight Beijing time on June 25th, the highly anticipated Micron Q3 FY2026 earnings report was officially released.

Prior to this quarter's report, Micron found itself in a somewhat awkward position. On one hand, everyone knew it would deliver an outstanding report. On the other hand, everyone also knew that the market had already priced in such "outstanding" performance.

Over the past few weeks, various market participants have been speculating around the same question — for a memory giant already at the heart of the AI wave, just how strong do its results need to be to continue driving its stock price higher and inject further confidence into the already frenzied semiconductor bull market?

The answer is — more exaggerated than anyone expected!

The Market Was Aggressive Enough, But Still Conservative

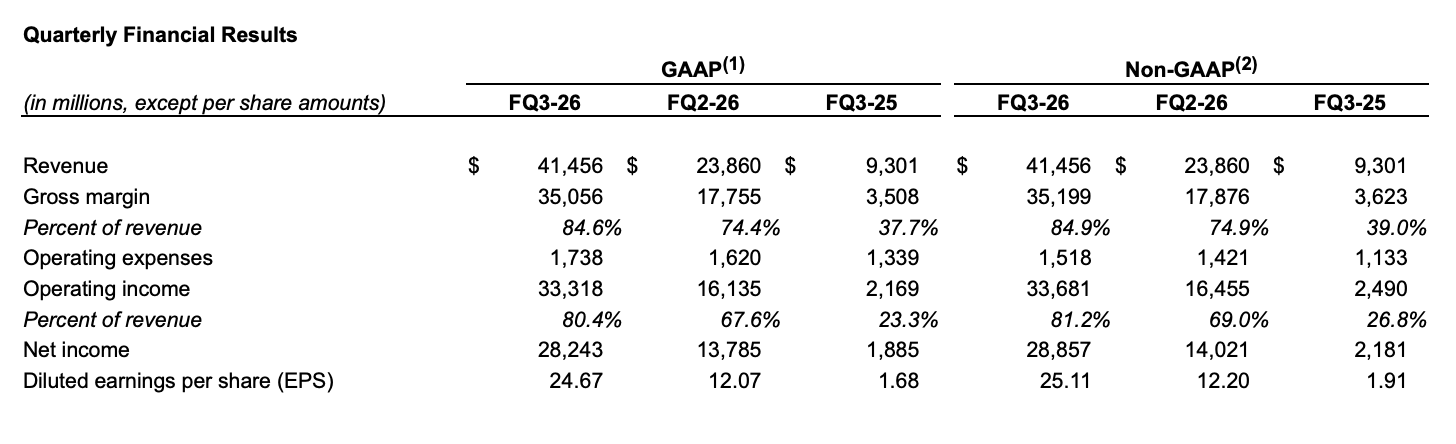

The Q3 report released this morning shows that Micron's third-quarter revenue reached $41.456 billion (consensus estimates were around $35.4 billion), a staggering year-over-year increase of 346%; GAAP net profit was $28.243 billion, up nearly 15 times year-over-year; adjusted earnings per share were $25.11.

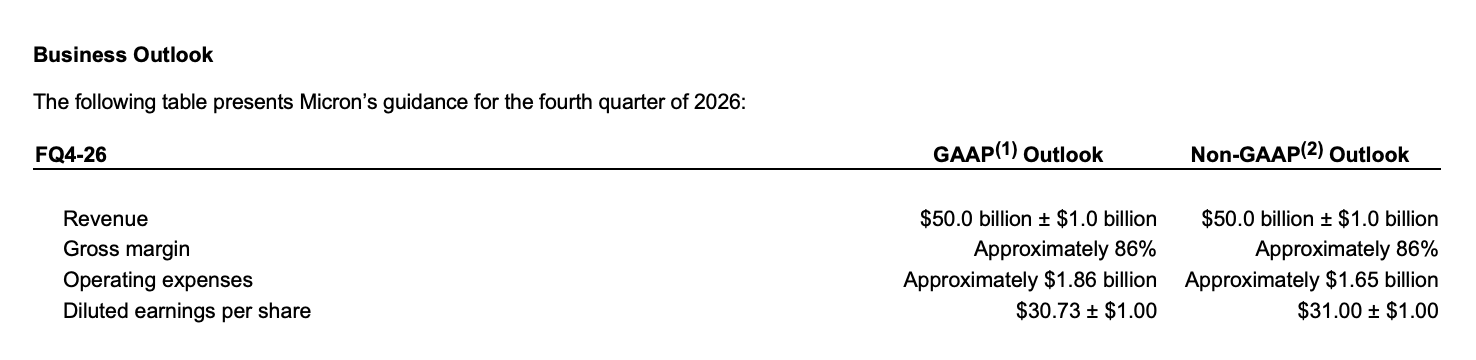

Even more exaggerated is the next quarter's guidance. Micron expects its Q4 revenue to reach $50 billion (plus or minus $1 billion), far exceeding the market's previous expectation of about $42.9 billion and even Goldman Sachs's aggressive forecast of $48.8 billion (widely seen as the most optimistic scenario); Q4 gross margin is expected to be about 86%, with EPS expected to reach around $31.

This is why many investors exclaimed the same sentiment immediately after the report's release: this is what you call a super, invincible, spiral, explosive, sky-rocketing earnings report!

From HBM to SSD, the Entire Memory Stack is Sprinting

If one were to identify a core driver for this round of growth, the answer remains, of course, AI. However, compared to the HBM that the market has repeatedly discussed over the past year, a more noteworthy point in this report is — AI's influence has begun to spread throughout the entire memory supply chain.

From a business structure perspective, almost all of Micron's core businesses are growing simultaneously, including:

- Cloud memory business revenue reached $13.77 billion, up over 300% year-over-year;

- Core data center business revenue reached $11.52 billion, up over 600% year-over-year;

- Data center SSD revenue exceeded $5 billion;

- Mobile and client business grew over 250% year-over-year;

- Automotive and embedded business also achieved over 300% growth;

- Gross margins across business lines generally remained around 80% or higher.

This signifies that the current AI wave is benefiting not just a single product, but the entire memory industry chain comprehensively.

On one hand, HBM remains the most direct beneficiary. Micron stated that HBM4 has begun volume shipments to core customers, with samples already delivered to multiple end customers; HBM4E is progressing as planned and is expected to enter mass production in 2027. Simultaneously, the company reiterated that its 2026 HBM capacity is completely sold out.

On the other hand, the continued expansion of AI training and inference demand is also driving concurrent growth in high-end DRAM, enterprise SSD, and NAND product demand. As more advanced capacity is prioritized for HBM, supply in the traditional DRAM and NAND markets tightens further, propelling the entire memory market into its strongest pricing cycle in recent years.

This is also why Micron remains extremely optimistic about the industry's outlook. Management expects the tight supply-demand situation in the DRAM and NAND markets to persist beyond 2027. In other words, in Micron's view, the industry is not nearing a cycle peak, but rather resembles the early stages of the AI infrastructure construction cycle.

Long-Term Agreements Locked In as Far Out as 2030

If we merely interpret this earnings report as a victory for HBM, we might still be underestimating its true significance. Because compared to the $50 billion revenue guidance, perhaps the most noteworthy numbers in this report are another set — $100 billion.

On the earnings call, Micron disclosed that to date, the company has signed 16 long-term strategic customer agreements (SCAs) covering data center, consumer electronics, and automotive customers. Most of these agreements have terms of up to 5 years, with some automotive client agreements lasting 3 years, extending as far out as the end of 2030.

These agreements already cover approximately 20% of DRAM shipments and about one-third of NAND shipments. As more agreements are finalized, over half of future revenue is expected to fall under the long-term agreement framework.

It is important to emphasize that these agreements are not traditional supply contracts. Management confirmed that the agreements utilize a strongly binding Take-or-Pay model. Even if customers do not fully take delivery in the future, they are still obligated to fulfill the agreed purchase commitments. Some major agreements even incorporate price ceiling and floor mechanisms, with the ceiling anchored to Q2 FY2026 market prices. Even at the agreement's price floor, the corresponding gross margin level remains significantly higher than Micron's historical cycle peaks.

Based on data disclosed by Micron management, 14 of these agreements currently correspond to guaranteed revenue of approximately $100 billion; concurrently, customers will also provide a total of about $22 billion in performance guarantees, with roughly $18 billion in cash form, which can be directly used to support future capacity construction and R&D investment.

For the memory industry, this is almost a historic change. For decades, the industry's operating logic has been "expand capacity first, then wait for demand to catch up"; now, Micron is gradually shifting to another model — lock in orders first, then expand capacity.

This is also what excites the capital market the most. Because it means Micron's current profitability is no longer based solely on expectations for a cyclical upturn, but is underpinned by long-term contracts.

Capacity Expansion, Expansion, and More Expansion, $10 Billion to be Spent in Q4

If long-term agreements answer "where is the demand coming from?", then capital expenditure answers another question — how does Micron plan to meet this demand?

The report shows that Micron expects Q4 capital expenditure to reach approximately $10 billion (higher than Wall Street's previous expectation of about $8.9 billion). Full-year FY2026 capital expenditure is projected to be around $27 billion, and quarterly capital expenditure in FY2027 will be higher than the Q4 FY2026 level. New investments will primarily be used for HBM, advanced DRAM, and advanced packaging capacity construction.

In the past, such capital expenditure figures might have raised market concerns. After all, for the memory industry, "large-scale capacity expansion" is hardly an unfamiliar phrase. Historically, whether it's Samsung, SK Hynix, or Micron itself, companies have ramped up investment at industry peaks, ultimately leading to oversupply, price collapses, and亲手 ending the previous bull market.

But this time, things seem to be changing. The reason is simple — this new capacity is not based on optimistic forecasts of future demand, but on long-term orders already signed.

On one side is $100 billion in guaranteed revenue, $22 billion in performance guarantees, and long-term agreements extending to 2030; on the other side is continuously expanding HBM, advanced DRAM, and advanced packaging capacity. Comparing these data points, the current capacity expansion appears more like executing already locked-in orders, rather than the traditional cycle-betting expansion based on demand forecasts.

Micron's Earnings Report Rekindles the Semiconductor Bull Market

Prior to the release of Micron's quarterly report, market sentiment surrounding the ongoing semiconductor bull run had shown signs of wavering.

Earlier this week, the South Korean semiconductor sector experienced a noticeable pullback, with leading companies like SK Hynix and Samsung Electronics collectively under pressure. Some investors began to worry whether the AI trade had become too crowded after over a year of frenzied gains.

And Micron's answer was quite direct — demand hasn't peaked; the market is still underestimating demand.

From the far-exceeding-expectations Q3 performance and the high $50 billion Q4 revenue guidance; from the sold-out HBM capacity to the long-term strategic agreements extending to 2030 — all convey the same signal: AI infrastructure construction is accelerating, not slowing down.

Following the report's release, Micron's stock surged 16% in after-hours trading, driving collective gains for other U.S. semiconductor companies like Intel, ASML, Marvell, and Qualcomm. Japanese and South Korean markets also opened higher and rose today, with the South Korean market experiencing another trading halt, and Samsung and Hynix both rebounding significantly. After the A-share market opened, the semiconductor industry chain also strengthened, led by memory and advanced packaging sectors.

In a sense, this is no longer just an earnings report belonging to Micron, but another confidence booster for the entire semiconductor industry. Because the market has reconfirmed one thing — the AI story is far from over, and memory is becoming an increasingly important protagonist in this story.