2024年到2025年,传统金融领域发生了一个重要的变化:越来越多的传统资产开始以代币化的形式出现在链上。

比如,全球最大的资产管理公司贝莱德推出了自己的代币化基金,各大公链上部署的RWA项目总锁仓价值持续增长。高盛、摩根大通等华尔街巨头也纷纷启动了代币化试点项目。

什么意思呢?就是以前你要买美国国债,得去找银行、开账户、换美元,现在你可以直接在链上买到代表美国国债收益权的代币。以前你想投私募股权,门槛动辄百万美元,现在通过代币化,小额也可以参与。

代币化TradFi资产的四种形态

第一类:合规稳定币与国债代币

像USDC、USDT本身就是法币在链上的映射。而更新鲜的是国债代币——比如美国政府短期国债被代币化之后,持有者可以赚到约4-5%的无风险收益,这在DeFi收益波动巨大的今天显得格外有吸引力。

第二类:大宗商品代币化

黄金、白银等贵金属已经有多种链上代币版本,每个代币锚定一盎司的实物黄金,由托管机构持有实物并接受审计。这让你可以像交易山寨币一样交易实物黄金。

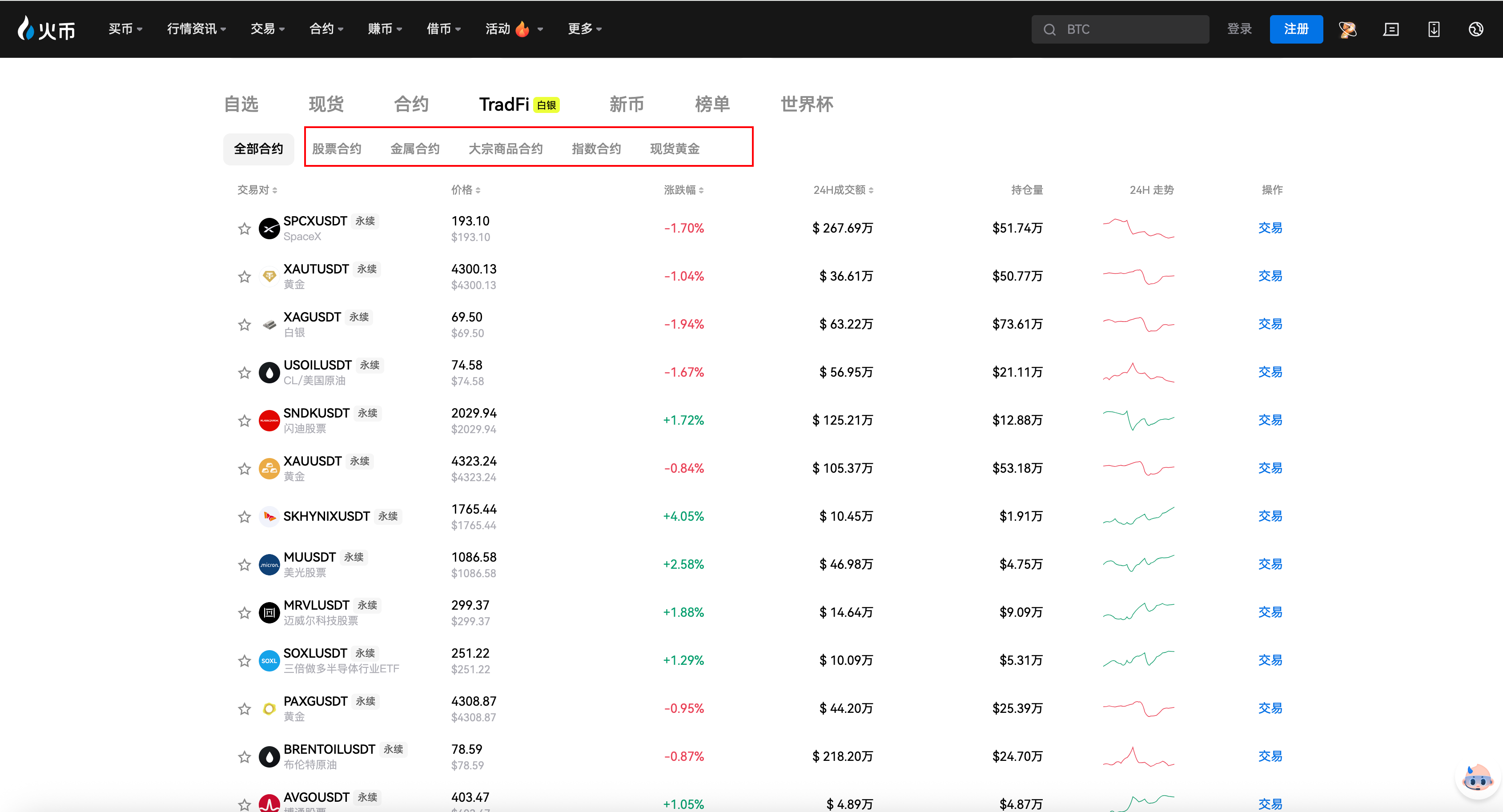

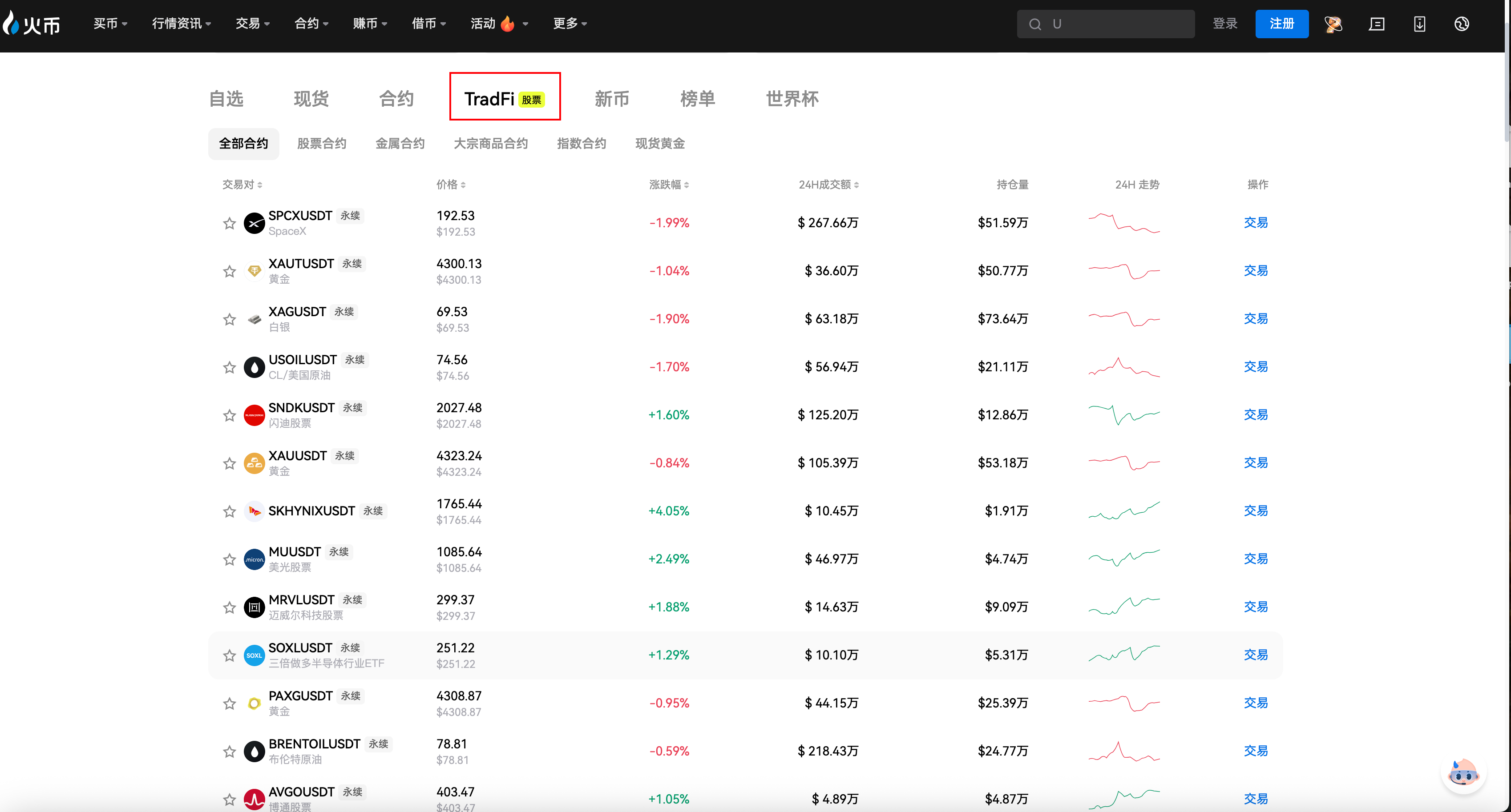

第三类:股票代币化(HTX TradFi正在做的事)

HTX的TradFi专区采取了“永续合约”形式,让用户可以用USDT作为保证金,交易SPX500、NVDA、TSLAX等标的的价格。虽然不是直接持有底层股票,但价格完全锚定对应资产,且拥有24小时交易、支持做多做空、操作体验与加密合约一致等优势。

第四类:私募信贷与另类资产

这部分更进阶一些——包括代币化的私募股权、房地产REITs、基础设施项目等。通过碎片化代币,原本需要百万美元起投的资产变成了普通人也能小额参与的机会。

为什么这很重要?

因为对于普通的Crypto用户来说:

第一,收益来源多元化。 不再只有“持币等涨”和“DeFi挖矿”两条路。你可以配置一部分资金在TradFi资产上,获取与传统经济挂钩的收益。

第二,风险分散工具。 当加密市场进入深熊时,TradFi资产往往表现出完全不同的走势。黄金可能在涨,国债收益可能在升,这些都可以对冲你Crypto仓位的风险。

第三,进入门槛大幅降低。 以前你要在传统券商开户,需要身份认证、银行转账、等待几个工作日。现在在HTX上,只要你有USDT,三秒钟就可以开始交易TradFi资产。

链上TradFi的潜在风险

任何新趋势都有风险,你需要了解这几点:

- 流动性风险:部分代币化资产交易量较小,买卖价差可能较大

- 托管风险:锚定实物资产的代币,依赖底层托管机构的信用

- 监管不确定性:各国对RWA的监管政策仍在变化中

- 协议风险:如果涉及跨链桥或智能合约,存在技术风险

HTX TradFi的优势在于:所有标的都是永续合约形式,由平台统一提供流动性,不存在底层托管或跨链桥的额外风险,价格透明锚定国际市场。

实操:如何在HTX体验TradFi链上交易?

第一步:打开HTX App,确保账户中有USDT

第二步:进入“合约”页面,点击顶部“TradFi”标签

第三步:浏览所有可交易标的(目前75+),点击任意一个进入交易界面,设置杠杆(建议首次使用1-3x),设置止损价,输入仓位数量

然后选择“买入开多”或“卖出开空”,确认开仓。

TradFi的链上化不是“会不会发生”的问题,而是“速度有多快”的问题。当华尔街和Crypto之间的墙被推倒,普通人第一次可以像机构一样——用手机、用USDT、用三秒钟的时间——配置全球最主流的资产。

这就是HTX TradFi正在做的事情。