撰文:BiyaMews

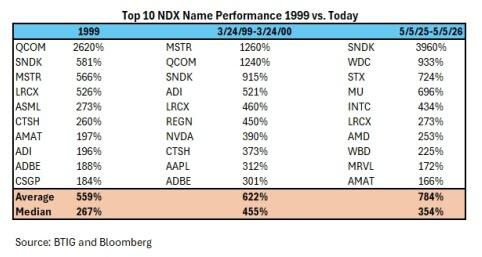

看着纳斯达克 100 指数前 10 大成分股过去一年平均涨了 784%,我脑海里浮现的是 2000 年互联网泡沫破裂前那些疯狂的日子。当时高通一年涨了 2600%,人们说这次不一样。现在,闪迪一年涨了 3960%,比高通当年还猛 1300 个百分点,而人们又说这次不一样。

历史从不会简单重复,但押韵得让人后背发凉。

这轮涨幅到底有多夸张?

先看一组让人窒息的数据。根据 BTIG 首席技术分析师 Jonathan Krinsky 的最新报告,过去一年纳斯达克 100 指数表现最好的前 10 只股票平均涨幅高达 784%。作为对比,1999 年这个数字是 559%,2000 年 3 月市场见顶前一年是 622%。

更扎心的是,1999 年表现最好的高通,52 周涨幅 2600%;2000 年见顶前最好的 Strategy,涨幅 1260%。而现在,闪迪以 3960% 的涨幅碾压了这两个纪录。

我曾在 2020 年 3 月美股熔断时抄底,当时觉得那是十年一遇的机会。但说实话,看到这种涨幅,我更多是恐惧而不是兴奋。因为上次见到这种级别的疯狂,还是在 2000 年 3 月,之后纳斯达克跌了 78%。

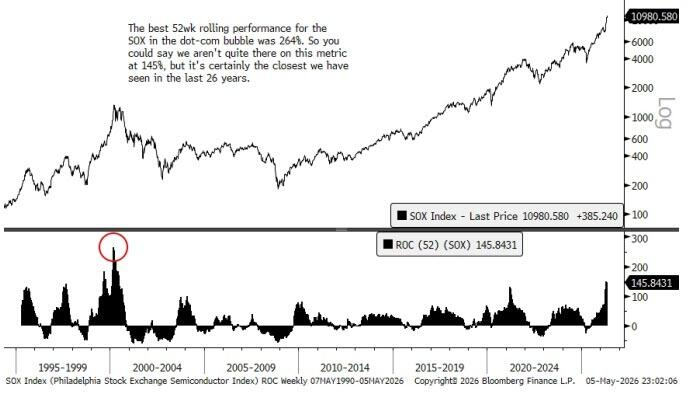

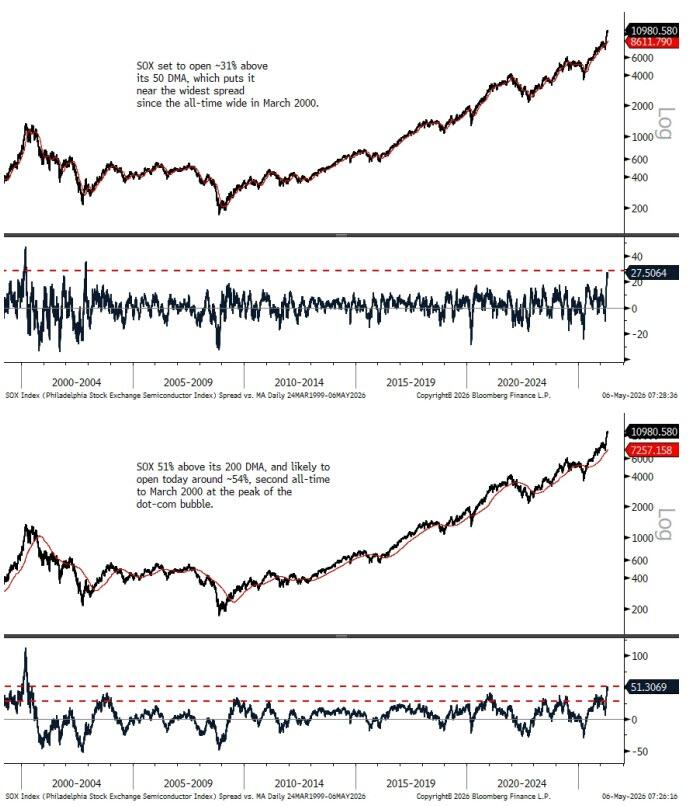

作为本轮上涨的核心引擎,费城半导体指数(SOX)的表现同样逼近历史极值。互联网泡沫时期,该指数最佳 52 周滚动回报率为 264%,而现在这个数字是 145%。虽然还没破纪录,但已经是过去 26 年来最接近极值的水平。

市场为什么不讲理地涨?

就在我写这篇文章时,中东局势出现缓和迹象,油价大跌,美债收益率跟着走低。市场对美联储年内加息的预期基本消失,AMD 等芯片巨头交出亮眼财报。这一切让股市环境显得「完美」。

但问题在于,这种「完美」让我想起 2018 年 1 月时的情况。当时所有人都觉得经济好、企业盈利强、减税利好,结果 2 月份市场突然暴跌,标普 500 单周跌了 10%。

彭博宏观策略师 Cameron Crise 说得对,这种宏观与微观层面的完美共振,让持怀疑态度的投资者感到背脊发凉。因为股市往往在好消息中见顶,而不是坏消息。

这次和 2000 年有什么不同?

最大的不同是基本面。2000 年互联网泡沫破裂时,很多公司根本没有盈利,全靠讲故事撑估值。而现在,AI 和半导体公司的业绩是实实在在的。英伟达、AMD 的财报数据摆在那里,营收和利润都在增长。

但这也正是我担心的。因为当所有人都用「基本面好」来论证市场不会跌的时候,往往就是调整的前兆。我记得 2021 年牛市时,所有人都在说「这次不一样,有基本面支撑」,结果 2022 年纳斯达克跌了 33%。

BTIG 预计,半导体板块可能会出现 25% 至 30% 的修正,这将使费城半导体指数回落至其 50 日移动平均线附近。这个判断和我观察到的技术指标基本一致。

投资者应该怎么办?

说实话,我无法预测市场何时见顶。但有几个信号值得关注:

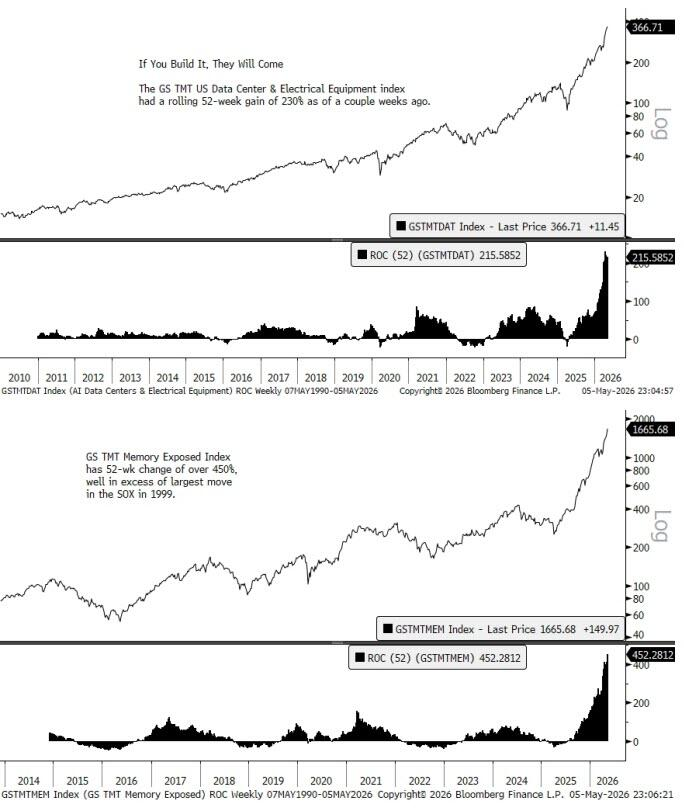

第一,当所有人都觉得「这次不一样」时,往往就是最危险的时候。第二,当半导体板块内部,数据中心相关股票涨了 230%,存储芯片类股票涨了超过 450% 时,获利盘的压力会越来越大。

第三,也是最关键的,美联储的政策转向存在不确定性。虽然市场现在预期年内不会加息,但如果通胀数据意外走高,一切可能瞬间反转。

我的建议是:如果你已经赚了不少,可以考虑逐步锁定利润。如果你还在犹豫要不要追高,不妨等等回调。因为即使这次真的不一样,市场也会给你更好的买入机会。

记住,2000 年互联网泡沫破裂前,很多人也觉得「这次不一样」。结果呢?纳斯达克从 5048 点跌到 1114 点,用了整整两年半才见底。而当年表现最好的那些股票,跌幅往往最大。

这次会不会重演?我不知道。但历史告诉我们,当涨幅超越 1999 年时,谨慎永远不是坏事。