On-chain shows Bitcoin miners have been in a phase of distribution recently, a sign that could prove to be bearish for the price of the crypto.

Bitcoin Miner Reserve Observes Downtrend As Miners Look To Dump

As pointed out by an analyst in a CryptoQuant post, the latest selling from BTC miners may force the price down in the short term.

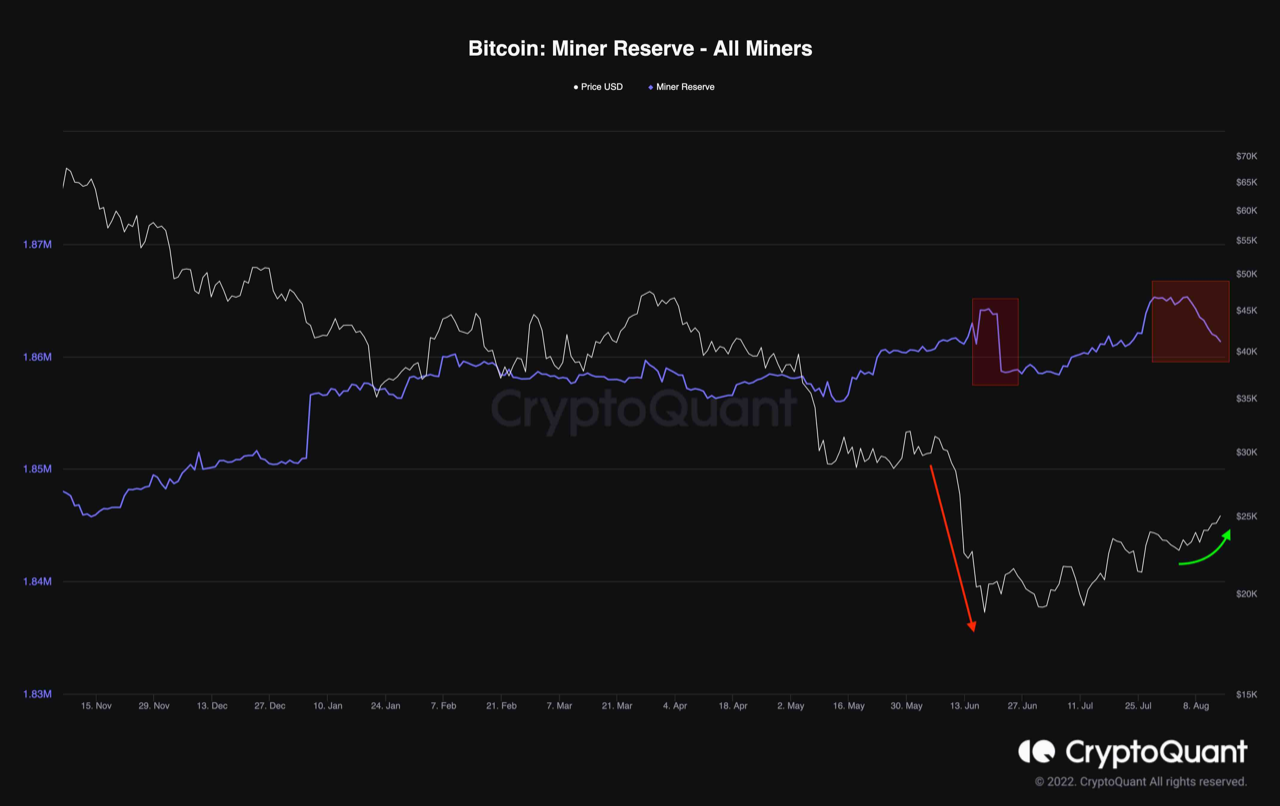

The “miner reserve” is an indicator that measures the total amount of Bitcoin currently stored in the wallets of all miners.

When the value of this indicator goes up, it means miners are depositing coins into their wallets right now. Such a trend, when prolonged, can be a sign of accumulation from these network validators, and could thus be bullish for the price of BTC.

On the other hand, declining values of the metric suggest miners are transferring a net number of coins out of their reserves at the moment. Since miners usually withdraw their BTC for selling purposes, this kind of trend can be bearish for the value of the crypto.

Now, here is a chart that shows the trend in the Bitcoin miner reserve over the last several months:

Source: CryptoQuant

As you can see in the above graph, the Bitcoin miner reserves have been trending downwards during the past couple of weeks, while the price has been going up.

This could suggest that miners may be participating in distribution recently, taking advantage of the higher prices.

This selling from the miners can dampen this latest rally and take the value of the coin down, at least in the short term.

The reason behind such dumping from this cohort is the recent shrinking revenues in Bitcoin mining. Many miners might need to sell more than usual to pay off their running costs at these lower revenues.

Some other miners would also have remaining payments for their mining rigs so they will have to sell more of their reserve to pay them off in the current environment.

BTC Price

At the time of writing, Bitcoin’s price floats around $24.5k, up 6% in the last seven days. Over the past month, the crypto has gained 21% in value.

The below chart shows the trend in the price of the coin over the last five days.

Source: BTCUSD on TradingView