Корпоративные запасы биткоинов продолжают расти, но руководители казначейства утверждают, что эта тенденция усиливает, а не ослабляет децентрализацию в сети.

По словам нескольких руководителей, выступивших на конференции Bitcoin Amsterdam 2025, владельцы активов, новые корпоративные казначейские компании и новые институциональные игроки способствуют более широкому распространению в экосистеме.

«В конечном счете, мы фактически децентрализуем биткоин. Со стороны это может показаться неочевидным, но это действительно так, судя по спросу, который мы создаем на рынке», — заявил Александр Лайзе, директор по стратегии биткоина в Capital B.

Лайзе заявил, что все больше банков, предлагающих варианты хранения биткоинов, предоставляют частным лицам и корпорациям новые возможности хранения и снижают зависимость от небольшой группы кастодианов.

На фото слева направо: Кинг Оэй, Сандер Андерсен, Александр Лайзе, Гарет Дженкинсон на Bitcoin Amsterdam 2025. Источник: Гарет Дженкинсон.

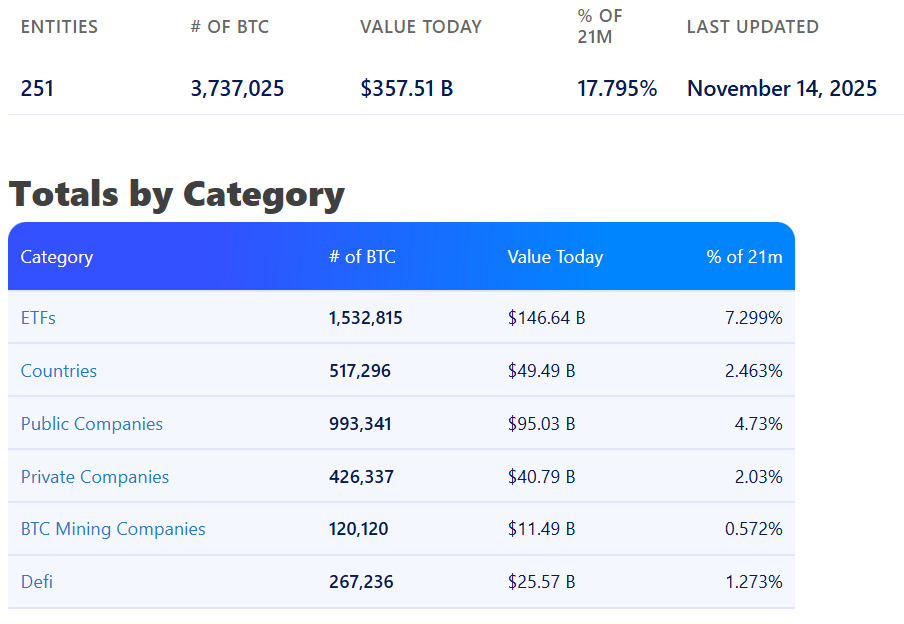

Корпорации концентрируют почти 7% от общего объема предложения биткоинов

Корпорации и биржевые фонды биткоинов (ETF) постепенно накапливают запасы биткоинов, все больше централизуя распределение первой в мире криптовалюты.

По данным поставщика казначейских данных bitbo.io, корпоративные участники уже накопили 6,7% от общего объема предложения биткоинов, в том числе 4,73% через публичные компании и 2,03% через частные компании.

Общий запас биткоинов, находящихся в распоряжении различных организаций. Источник: Bitbo.io.

Спотовые биткоин-ETF также аккумулировали почти 7,3% предложения биткоинов, став крупнейшим сегментом держателей менее чем за два года с момента их дебюта в январе 2024 года.

«Растущие централизованные активы не представляют собой непосредственной угрозы для биткоина, поскольку его экономическая собственность по-прежнему распределена между многими базовыми инвесторами, а не одним субъектом, — рассказал аналитик криптоаналитической платформы Nansen Николай Зондергаард. — Это не меняет фундаментальных свойств Биткоина. Сеть остается децентрализованной, даже если хранение становится более централизованным».

Он добавил, что это и не является «ахиллесовой пятой» для биткоина, но подчеркивает, что крупные игроки, занимающиеся кастодиальными операциями, могут иметь «больше влияния на ликвидность и поведение рынка», поскольку их активы в BTC продолжают расти.

Тем не менее, некоторые отраслевые обозреватели все больше обеспокоены растущим институциональным принятием биткоина, поскольку в августе объем корпоративных криптовалютных активов превысил 100 миллиардов долларов.

По словам криптоаналитика Вилли Ву, растущая корпоративная концентрация Bitcoin может стать новой централизованной точкой уязвимости, направив BTC на тот же «путь национализации», что и золото в 1971 году.

«Если доллар США структурно слабеет, а Китай набирает обороты, то вполне справедливо, что США могли бы сделать предложение всем казначейским компаниям и централизовать его, чтобы затем перевести в цифровую форму, а не создавать новый золотой стандарт, — сказал Ву в ходе панельной дискуссии на Baltic Honeybadger 2025. — Тогда можно было бы повторить то же самое, что произошло в 1971 году. И все это будет сосредоточено вокруг цифрового биткоина. Вся история повторяется снова и снова».

В 1971 году президент США Ричард Никсон положил конец действию Бреттон-Вудской системы, приостановив конвертируемость доллара в золото и отказавшись от фиксированного курса в 35 долларов за унцию, фактически положив конец золотому стандарту.