Федеральная резервная система в среду снизила базовую процентную ставку на 25 б.п., до 3,75–4,00%. Это второе снижение ставки в этом году.

Центробанк отметил, что рост экономики остается умеренным. При этом темпы создания рабочих мест замедлились, а безработица немного выросла. Однако инфляция остается «несколько повышенной», поэтому ФРС осторожна в отношении дальнейшего смягчения политики.

ФРС балансирует между рисками инфляции и рынка труда

Решение также подтвердило, что ФРС завершит количественное ужесточение 1 декабря. Таким образом, сокращение баланса будет приостановлено раньше ожидаемого.

В заявлении подчеркнуты растущие риски для занятости. Это отличается от прошлых заседаний, где основной акцент делался на инфляции.

ФРС заявила, что будет определять дальнейшую политику «на основе поступающих данных». Также она учтет «баланс рисков» относительно двойного мандата.

Председатель Джером Пауэлл и большинство членов комитета поддержали решение, тогда как двое не согласились. Стивен Миран настаивал на снижении на 50 б.п. Он сослался на слабые данные по занятости.

Экономический контекст

Имеющиеся индикаторы показывают, что рост продолжает оставаться умеренным. При этом ключевые показатели рынка труда слабеют. Уровень безработицы остается низким, хотя ФРС признает, что с лета он немного вырос.

С начала 2025 года инфляция ускорилась, что усиливает опасения. Цены могут дольше оставаться выше целевого уровня в 2%.

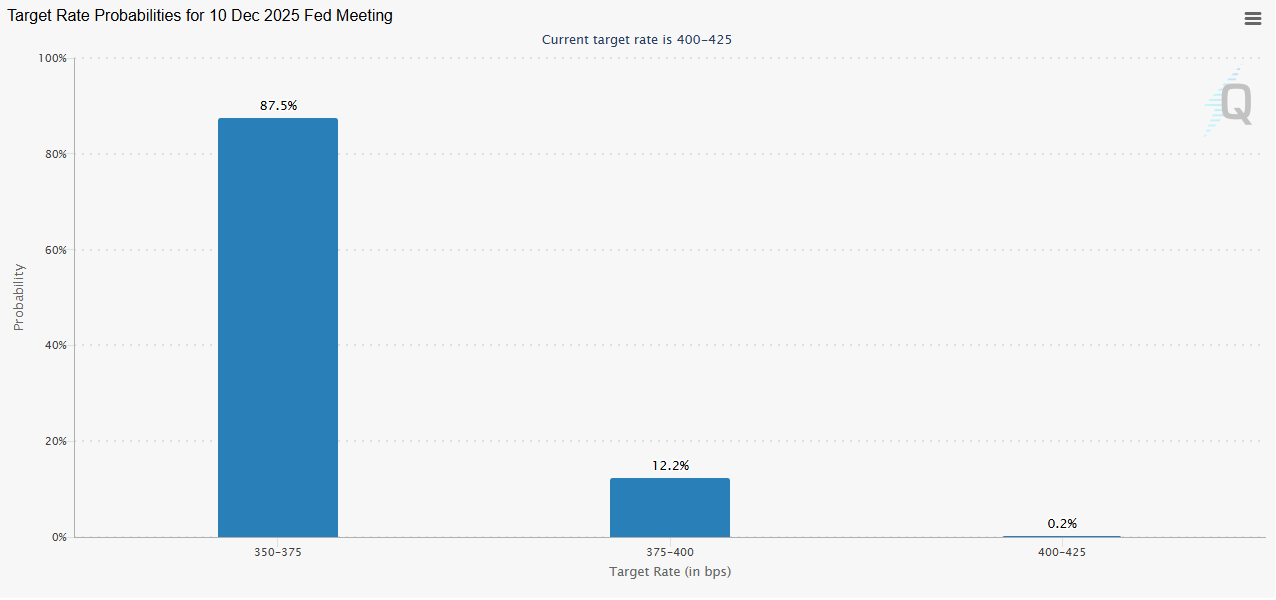

Фьючерсный рынок теперь закладывает 70% вероятность еще одного снижения на 25 б.п. Это может произойти в декабре.

Однако на пресс-конференции Пауэлл, вероятно, подчеркнет подход, основанный на данных.

Прогноз для рынка криптовалют

Такой поворот политики может краткосрочно усилить спрос на риск. Биткоин и крупные альткоины часто выигрывают, когда растет ликвидность. Также им помогает снижение доходности облигаций.

Крупные лидеры мнений, такие как Майкл Сейлор из MicroStrategy и Роберт Кийосаки ранее прогнозировали. По их оценкам, цена биткоина превысит $150,000 к концу 2025 года.

Однако устойчивая инфляция может сдержать общий энтузиазм. Если инфляционные ожидания снова повысятся, рисковые активы, включая крипто, столкнутся с новым давлением. Его усилит приток капитала в доллар.

По мнению аналитиков, баланс между смягчением и инфляцией определит следующую фазу крипторынка.

Длительная поддержка ликвидности способна поднять биткоин выше ключевых уровней сопротивления. Однако жесткий тон в декабре может развернуть эти достижения.

The post ФРС снизила процентные ставки и прекратила сокращение баланса. appeared first on BeInCrypto.