Past trend of the Bitcoin actual/realized price ratio may be forming a pattern that could hint at a possible bottom for the crypto at $17k.

Bitcoin Actual/Realized Price Ratio Currently Has A Value Of 0.8

As pointed out by an analyst in a CryptoQuant post, historical data of this BTC ratio may have interesting implications for the current market.

The realized cap is a capitalization model for Bitcoin that multiplies each coin in the circulating supply with the price at which the coin was last moved and takes the sum of all the values. This is different from the usual market cap, where the entire supply is simply multiplied by the current price of BTC to get the capitalization.

Now, from this realized cap, a “realized price” can also be obtained by dividing the metric with the total amount of coins in circulation.

The “actual/realized price ratio” is, therefore, an indicator that measures the ratio between the normal price of BTC and this new realized price.

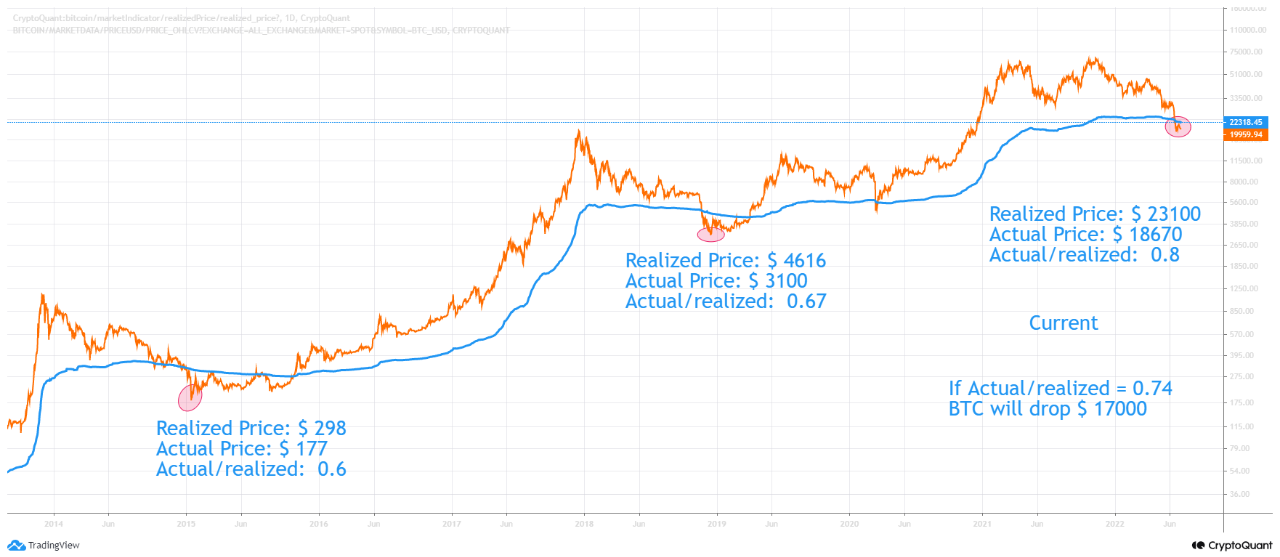

Here is a chart that shows the trend in this Bitcoin ratio over the last few years:

Looks like the actual price is lesser than the realized one at the moment | Source: CryptoQuant

In the above graph, the quant has highlighted the major bottoms during previous Bitcoin cycles and the value of the actual/realized price ratio at which they occurred.

Currently, the metric has a value of 0.8, which means the price of the crypto is around 80% of the realized price right now.

If there is a pattern here with the actual/realized price ratio, then the bottom this time may also form at a value 0.07 higher than the previous time.

This would put the ratio at about 0.74, which implies Bitcoin will need to decline further until $17k before this “bottom” value is reached.

Naturally, this would only happen if there really is such a pattern present here. Another indicator, the delta capitalization model, suggests that $15k could be a possible lower bound for a Bitcoin bottom.

BTC Price

At the time of writing, Bitcoin’s price floats around $19.2k, down 10% in the last seven days. Over the past month, the crypto has lost 35% in value.

The below chart shows the trend in the price of the coin over the last five days.

The value of the crypto seems to have been going down over the last couple of days | Source: BTCUSD on TradingView