From $35 to $1: PIPE deals are crushing Bitcoin treasury stocks.

— CryptoQuant.com (@cryptoquant_com) September 25, 2025

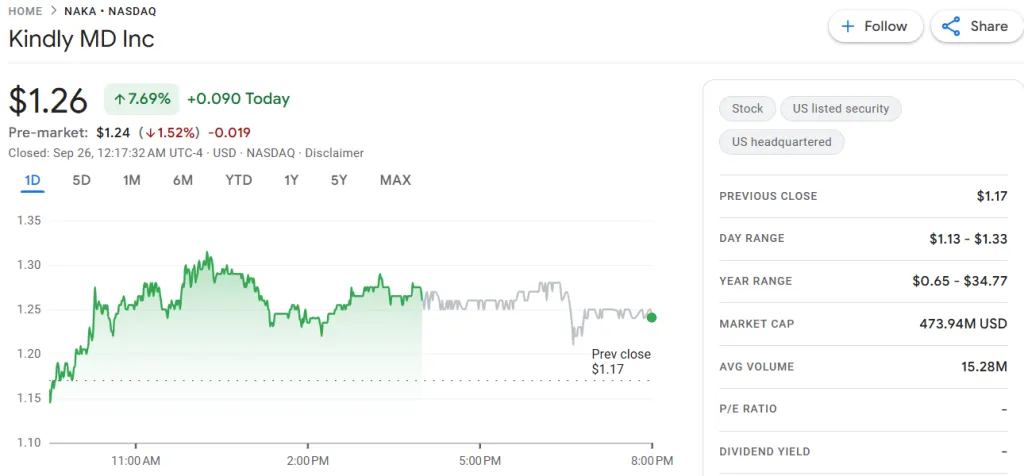

Kindly MD (NAKA) soared 18.5x in weeks, then fell 97%, back to its $1.12 PIPE price.

PIPE price gravity is brutal. pic.twitter.com/84KGVQLRHi

Исследователи отметили, что фирмы, выпускавшие новые бумаги через PIPE, часто сталкивались с заметными просадками: котировки со временем возвращались к ценам размещения. В отдельных случаях падение может достигать 50%, поскольку инвесторы выходят из лок-апа и готовятся к продаже.

PIPE-сделки позволяют участникам рынка покупать акции ниже рыночной цены и дают компаниям быстрый доступ к ликвидности. В криптоиндустрии этот инструмент обрел популярность как способ привлечь капитал в условиях высокой конкуренции.

Однако, как подчеркивает CryptoQuant, подобные размещения разбавляют долю текущих акционеров. Более того, они формируют навес предложения, давящий на цену бумаг.

Примеры падений

Анализ котировок ряда сфокусированных на биткоине компаний показал: часто снижение происходит именно после разблокировки PIPE-бумаг.

Так, акции Kindly MD (NAKA), преобразованной из медицинской в «казначейскую», рухнули более чем вдвое за день после снятия ограничений на продажу. До этого бумаги взлетели с $1,8 до почти $35 на фоне анонса сделки, но затем обвалились на 97%, до $1,16 — почти к цене PIPE в $1,12.

Акции Strive Inc. (ASST) с мая подешевели на 78% — с $13 до $2,75. При этом PIPE-раунд компании проходил по цене $1,35, что оставляет возможность дополнительного снижения примерно на 55% после открытия продаж в следующем месяце.

Схожая ситуация наблюдается у Cantor Equity Partners (CEP), которая объединяется с Twenty One Capital. Ее PIPE прошел по $10, акции потеряли почти 70% от максимума. Это указывает на риск дальнейшего снижения — вплоть до половины текущей стоимости.

CryptoQuant и другие аналитики отмечают, что даже крупные «казначейские» компании находятся под давлением: стоимость их криптоактивов постепенно приближается к рыночной капитализации. В такой ситуации только устойчивый рост цифрового золота способен остановить снижение котировок к уровням PIPE или даже ниже.

Напомним, аналитики CryptoQuant уже предупреждали о существенном замедлении роста корпоративных биткоин-резервов.

Криптоказначейства теряют темп, а блокчейны достигли «технического потолка»