US spot Bitcoin ETFs struggled through August while Ethereum funds dominated the scene. Now, the storm has settled, and capital is flowing back into crypto investment products.

The Bitcoin ETFs seem to be back enjoying the attention of US investors in the month of September, as seen with some significant performances over the past two weeks. The past week was particularly impressive, as the Bitcoin funds recorded no single outflow day.

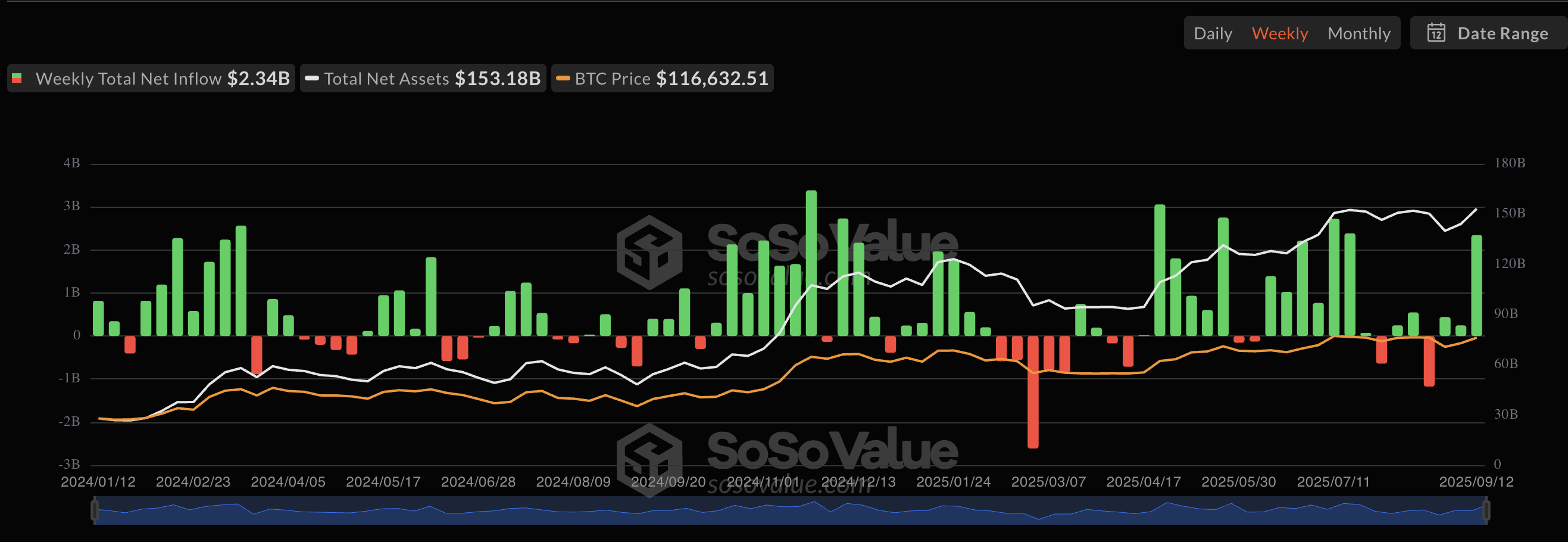

Bitcoin ETFs Close Week With $642-M Inflow

According to the latest market data, the US-based Bitcoin ETFs posted a total net inflow of $642.35 million on Friday, September 12. This single-day performance marked the fifth consecutive day of positive capital influx for the exchange-traded funds.

Surprisingly, Fidelity Wise Origin Bitcoin Fund (with the ticker FBTC) led the pack on Friday, closing the week with a net inflow of over $315 million. Meanwhile, BlackRock’s iShares Bitcoin Trust (with the ticker IBIT) came in second with a daily net inflow of $264.71 million on Friday. This impressive daily performance pushed the largest Bitcoin exchange-traded fund closer to reaching a net assets valuation of $90 billion.

Bitwise Bitcoin ETF (BITB) with a $29.16 million net inflow and ARK 21Shares Bitcoin ETF (ARKB) with a $19.37 million net inflow also added value in double digits on Friday. Grayscale Bitcoin Mini Trust (BTC) and VanEck Bitcoin ETF (HODL) were the only Bitcoin ETFs that recorded any activity, with $5.69 million and $8.24 million, respectively, on the day.

As inferred earlier, Friday’s $642-million performance was only the latest in a line of strong performances by the US-based Bitcoin ETFs. The latest market data shows that the BTC exchange-traded funds added $2.34 billion in value over the past week.

Source: SoSoValue

This past week’s performance represents the first time that the Bitcoin ETFs would be crossing the billion-dollar mark on the inflow chart. Also, the BTC-linked investment products outperformed the US Ethereum ETF market, which closed the week with a net weekly inflow of $637.69.

Bitcoin Price At A Glance

This positive performance of the spot Bitcoin ETFs is a reflection of the resurgence that the BTC price went through over the past week. According to data from CoinGecko, the premier cryptocurrency is up by more than 5%. As of this writing, Bitcoin is valued at around $115,990, with no substantial price change in the past 24 hours.

The price of BTC on the daily timeframe | Source: BTCUSDT chart on TradingView

Related Posts