作者:BitMEX

原文标题:虽迟但到的山寨季:四大信号揭示早期轮动已启动

不是梗图,是数据在说话。我们判断一轮早期山寨季正在展开,理由很简单:

-

市场结构: TOTAL3(剔除 BTC/ETH 的山寨总市值)相对两大主流币企稳;即便没有 BTC/ETH 的放量突破,市场宽度也在扩散。

-

领涨方向: SOL/ETH 上行、资金费率温和、强平不多——真买盘,不是挤空。

-

催化因素: 美国政府推进区块链应用,商务部将 GDP、PCE 等官方数据上链(经 Chainlink/Pyth),平台币阶段性重估等基本面把“场外”资金带回场内。

-

ETF 资金面: ETF 仍净流入但明显降温;ETH 相关 DAT(币股)的市值/净值比(m/NAV)偏低 → 增发吸引力下降,可能给山寨留出更多空间。

信号 1|市场结构与 TOTAL3 的韧性

过去 5 天的走势,更像山寨季开端而不是“只涨主流”的轮动。TOTAL3 在 BTC、ETH 震荡时未创新低;衍生品侧保持有序:资金费率接近中性、被动平仓有限——指向现货主导的真实需求。对交易员而言,重点很明确:不等 BTC/ETH 创新高,广度也能扩散;在配对交易里挑选山寨,性价比更高。

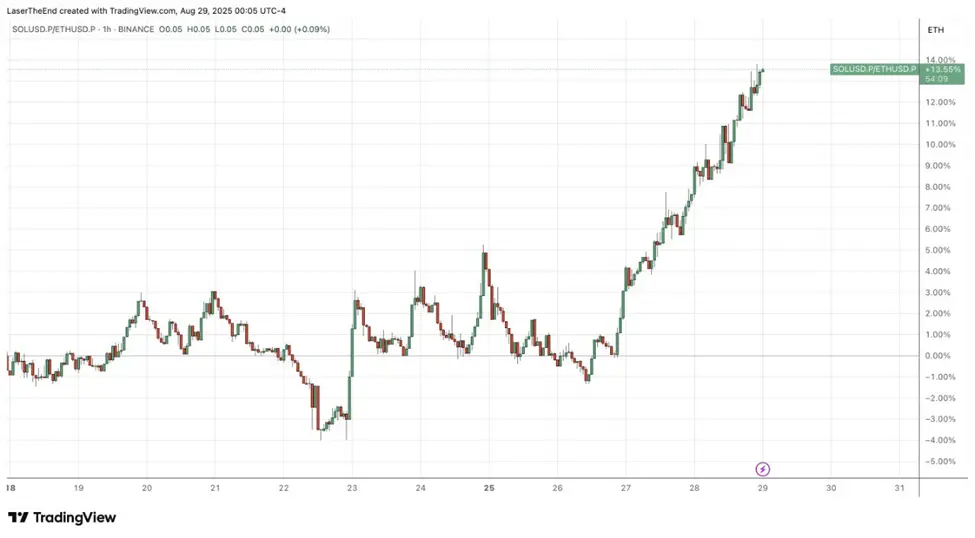

信号 2| SOL跑赢ETH,开始轮动

SOL/ETH 上行同时资金费率平稳、没有明显挤空痕迹,说明是主动配置的真实买盘。历史上,这常常领先于高流动中盘和功能赛道的配对轮动;同时提供更低 β的表达:做多 SOL / 做空 ETH。

信号 3|主流币“稳,但不带节奏”

来源:https://www.strategicethreserve.xyz/

主流币的基本面依旧正面,但 ETH、BTC 的边际动能在下降:回调有承接、上攻缺追涨,难以直接推高新高。

以 以太坊币股 为例,m/NAV 多在 1.0–1.1×,跑输现货 ETH,难以支撑继续“增发+被动现货买入”的链条。我们的判断是:主流抄底盘足、追高盘弱,边际风险下沉到有事件催化的山寨更合理。

信号 4|可落地的区块链应用在推进

政策与基础设施两端都有硬催化:美国商务部宣布将实际 GDP、PCE 等官方系列上链(经 Chainlink、Pyth,覆盖 Arbitrum、Avalanche、Base 等),权威且可机读的数据为数据驱动型 DeFi、代币化风控、事件市场打开新场景。

同时,区块链为底层的应用也获得了主流机构的认可和采用,Numerai(以 $NMR 激励、AI 驱动的对冲基金)获 摩根大通资管 5 亿美元策略容量承诺。

平台币阶段性走强:OKB 受代币模型调整提振,CRO 因特朗普家族基金投资等相关消息面而受关注。以上进展都不依赖 BTC/ETH 创新高——这正是山寨季早期的典型特征。

结论|交易框架

当前画面:主流有序、ETF 净流入降温、DAT 溢价偏薄、硬催化把资金往下游带。

策略上继续坚持配对优先、新闻优先:

-

核心仓位: 多 SOL / 空 ETH;关注新币上涨

-

卫星仓位: 以事件催化为锚,回调分批配置新闻驱动的山寨;直到资金流、资金费率或关键代理指标明确提示风格切换为止。

-

比推 TG 交流群:https://t.me/BitPushCommunity

-

比推 TG 订阅: https://t.me/bitpush