撰文:Nicky,Foresight News

近日,谷歌 Web3 战略负责人 Rich Widmann 通过社交媒体宣布,谷歌云正式推出其区块链网络 Google Cloud Universal Ledger(GCUL),并将其定义为「Layer1 区块链」。围绕其技术定位的讨论随之浮现:GCUL 究竟是一条真正的 Layer1 公链,还是更接近传统意义上的联盟链?

官方定位与核心特性

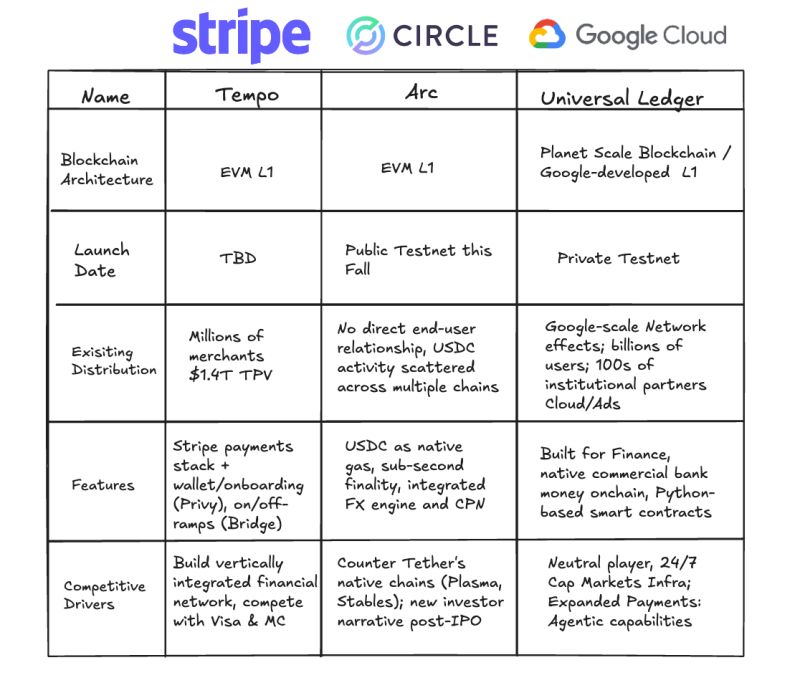

根据官方描述,GCUL 被设计为一个「高性能、可信中立且支持 Python 智能合约」的分布式账本平台,目前处于私有测试网阶段,主要面向金融机构提供服务。谷歌云强调,GCUL 旨在简化商业银行货币账户的管理,并通过分布式账本技术实现多货币、多资产的转账和结算,同时支持可编程支付和数字资产管理。

在官方发布的《稳定币之外:数字货币的演变》一文中,谷歌进一步阐释了 GCUL 的定位:它并非要「重新发明货币」,而是通过升级基础设施来解决传统金融系统的碎片化、高成本和低效率问题。GCUL 被包装为一项服务,通过 API 接口提供,强调其易用性、灵活性和安全性,尤其是在合规性(如 KYC 验证)和私有化部署方面的优势。

值得注意的是,GCUL 的早期测试已与芝加哥商品交易所(CME Group)展开合作。双方于 2025 年 3 月宣布启动分布式账本试点,探索批发支付与资产代币化的解决方案。

CME 首席执行官 Terry Duffy 表示,GCUL 有望在「24/7 交易趋势下」提升抵押品管理、保证金结算等环节的效率;谷歌云金融服务总经理 Rohit Bhat 则强调,此次合作是「传统金融机构通过现代基础设施实现业务转型的典型案例」。

Layer1 与联盟链:定义与分歧

在区块链领域,Layer1 通常指底层基础公链,如以太坊、Solana 等,其核心特征包括去中心化、无需许可和公开透明。任何用户均可自由参与网络验证、交易或部署智能合约,且链上数据对所有人可见。

相比之下,联盟链(Consortium Blockchain)是一种需许可(Permissioned)的分布式账本,由特定组织或机构共同维护,节点准入受控,数据访问权限可定制。典型应用包括 Hyperledger Fabric、蚂蚁链等。联盟链的优势在于合规可控、性能较高,但牺牲了开放性和抗审查性。

GCUL 更符合哪种模式?

从目前已披露的信息看,GCUL 表现出明显的联盟链特征:

-

私有与许可性:GCUL 明确运行在「私有且需许可的网络」上,节点准入和账号权限由管理机构控制。

-

目标用户:专注于金融机构(如 CME Group),而非公众自由参与。

-

合规优先:设计初衷包含 KYC 验证、交易费用符合外包规定等传统金融合规要求。

-

技术架构:尽管支持智能合约(基于 Python),但其底层基础设施由谷歌云采取中心化的方式维护,与「去中心化」的 Layer1 理念存在差异。

然而,谷歌云官方仍坚持将其称为「Layer1」,并强调「可信中立」和「基础设施中立」 — 即任何金融机构均可使用,而非仅限于特定利益集团。这种表述试图在叙事上模糊公链与联盟链的边界。

第三方观点:质疑与观望

行业从业者对 GCUL 的定位提出了不同看法:

-

BODL Ventures 合伙人刘锋认为,GCUL 更符合「联盟链」特征,与去中心化、无需许可的公链存在本质区别。

-

Dragonfly 合伙人 Omar 表示,此前谷歌对 GCUL 的表述较为模糊,如今团队明显倾向于将其包装为「Layer1」,但实际技术细节尚未完全公开。

-

Helius CEO Mert 指出,GCUL 目前仍是「私有且需许可」的系统,与公链的开放模型不同。

尽管存在质疑,也有观点认为 GCUL 可能代表一种「渐进式创新」。例如,谷歌与 CME 集团的合作试点显示,机构对分布式账本技术在结算、抵押品管理等场景的应用存在需求。GCUL 若能整合谷歌的技术能力和金融合规经验,或许能在传统金融与区块链之间找到一条实用化路径。

免责声明:本文基于公开信息分析,GCUL 的具体技术架构和运营模式仍需以谷歌官方后续披露为准。