8月初,上市公司陆续公布了2025年第二季度财报,其中较为亮眼的当属Strategy(MSTR),在Michael Saylor的带领下,Strategy在2025 年第二季度营业收入创历史新高,约为 140.3 亿美元,较去年同期增长 7106%。而 Strategy 持有的加密资产浮盈为 140 亿美元。

这一切都基于Saylor选择BTC作为储备的决定,从Strategy、Metaplanet到各种转型为加密储备的公司,从储备再BTC到ETH、BNB,SOL和SUI等。正如加密热点赛道发展一样,加密代币储备的类型和公司也在短短几个月之内陆续涌现。而对于散户来说,除了投资被列入储备的代币,也可以买入储备公司的股票。为此,为大家整理并测评了常用的加密储备公司数据查询网址/工具,如下:

综合查询网址

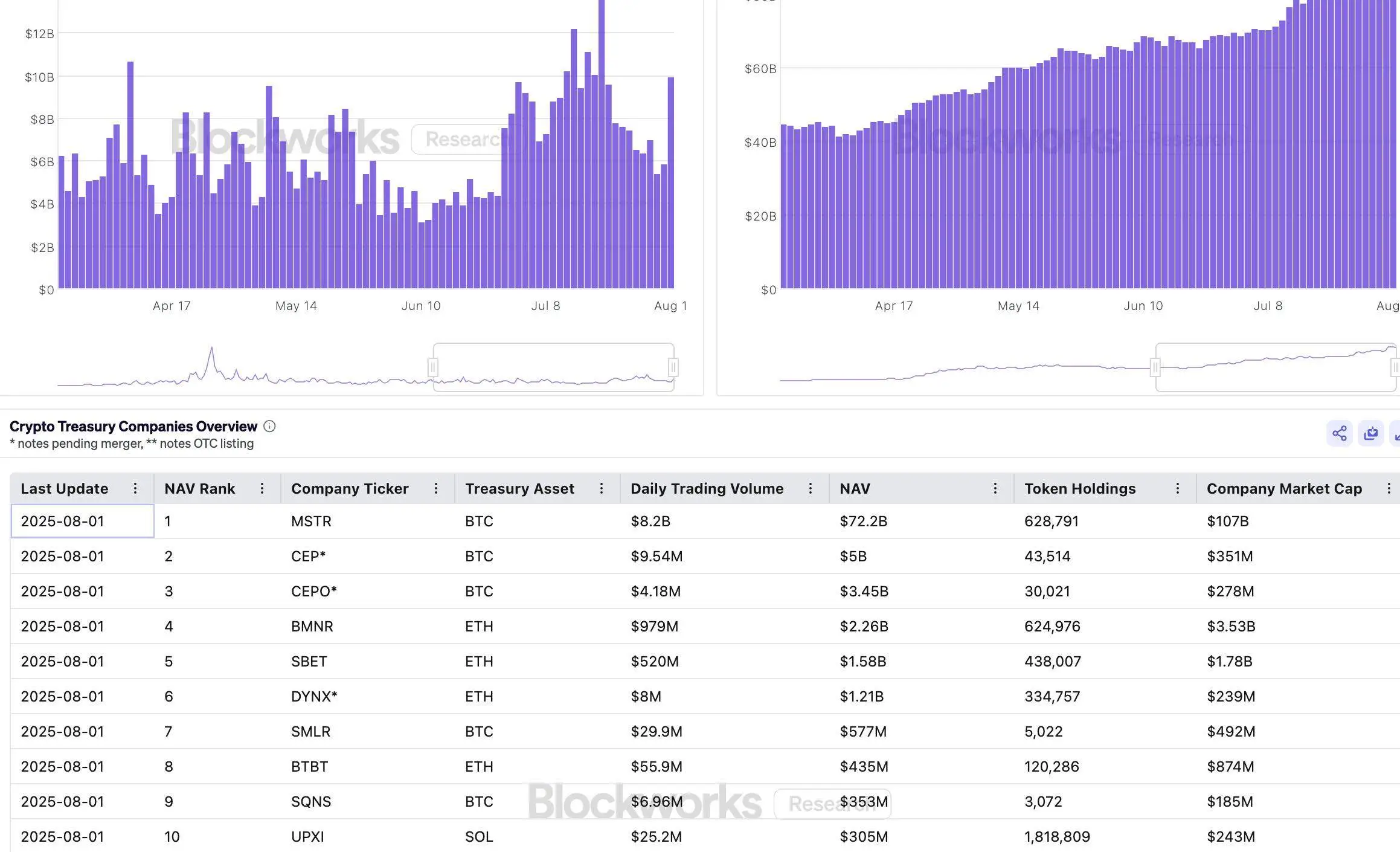

1、Blockworks

简介:Blockworks的加密储备公司数据涵盖BTC、ETH、SOL、HYPE、XRP、SUI和多代币储备,共录入26家加密储备公司,数据栏包括加密财务公司的交易量、加密净资产值 (NAV) 等关键指标。用户可以清晰查询到:

加密储备公司股票Ticker、储备代币名称、股票日交易量、NAV、持有代币数量和公司市值。Blockworks也根据持有的加密资产净值为储备公司进行排名。(其股票数据来源为Polygon.io——一个提供美国股票市场数据的API服务。)

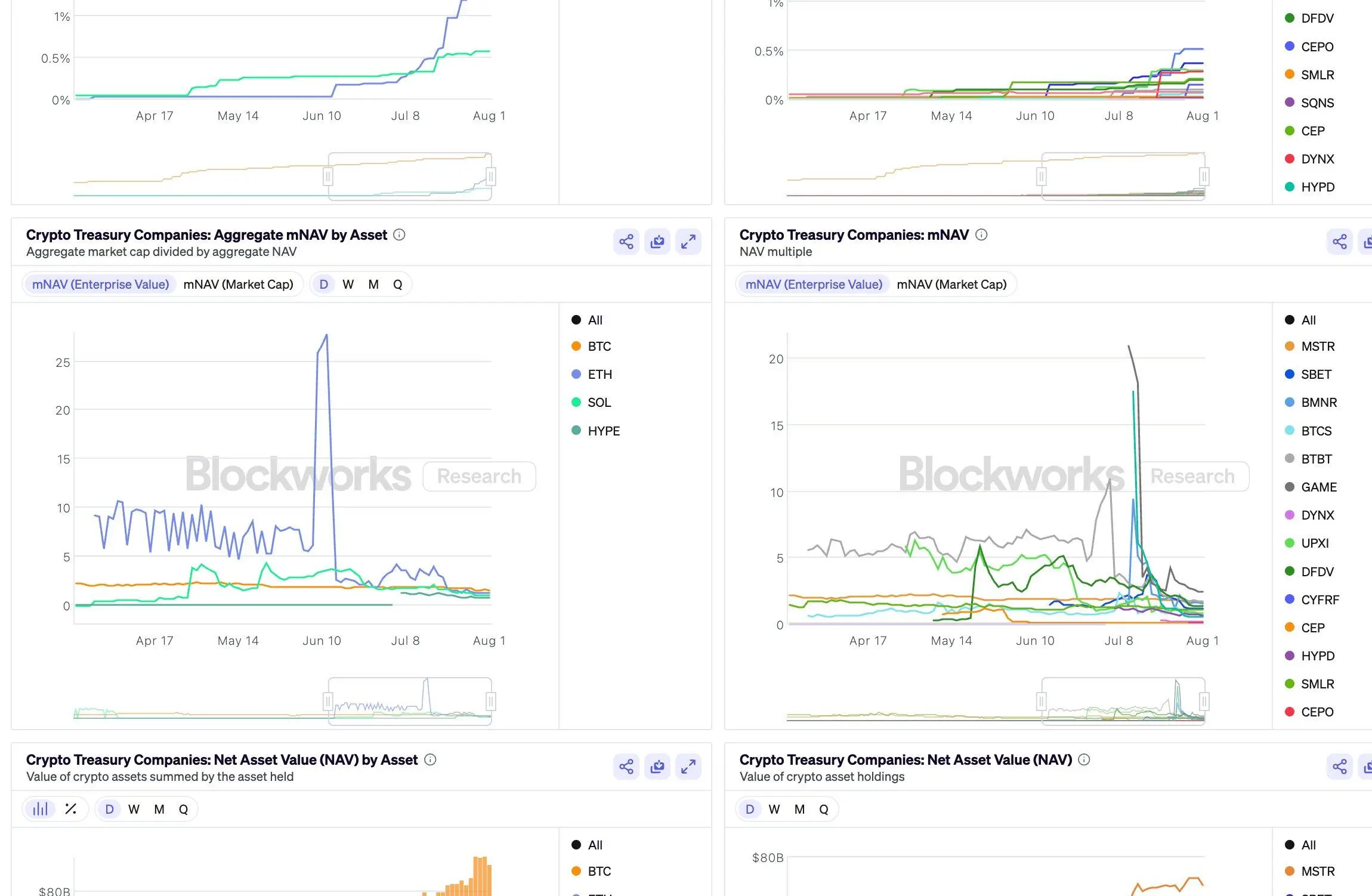

Blockworks还对以上数据绘制了数据表,除了上述提到的数据图表外,值得关注的是Blockworks还绘制了MNAV数据表,给出M(资产净值倍数)值的数据走势,包括企业价值和公司市值的M值,M(市值)就是公司总市值除以加密资产价值,M(企业价值)就是公司市值+总债务-现金除以加密资产价值,比如Strategy的M(市值)为1.48,Strategy 的 M(企业价值)为1.68,M也是加密储备健康度的一种风险指标。

此外,Blockworks还给出了公司净资产值溢价(市值减去加密储备价值)的数据表(比如Strategy的净资产值溢价为343.6亿美元)。还有每种加密储备公司的总净资产值溢价数据表(比如BTC储备公司的净资产值溢价为 262.9亿美元),因部分BTC储备公司的股票价值小于其持有的加密资产价值,也就是其M低于1。

评价:综合来看,Blockworks在综合数据上较为全面,单项数据和风险指标上较为细致,录入的加密储备公司数量较多。其资产净值溢价和MNAV的数据表可以很直观的看出加密储备公司的风险指标数据,略有不足就是该网址只给出了股票Ticker而非公司全称,对于一些不太熟悉美股的用户还需要先查询股票Ticker再了解公司。

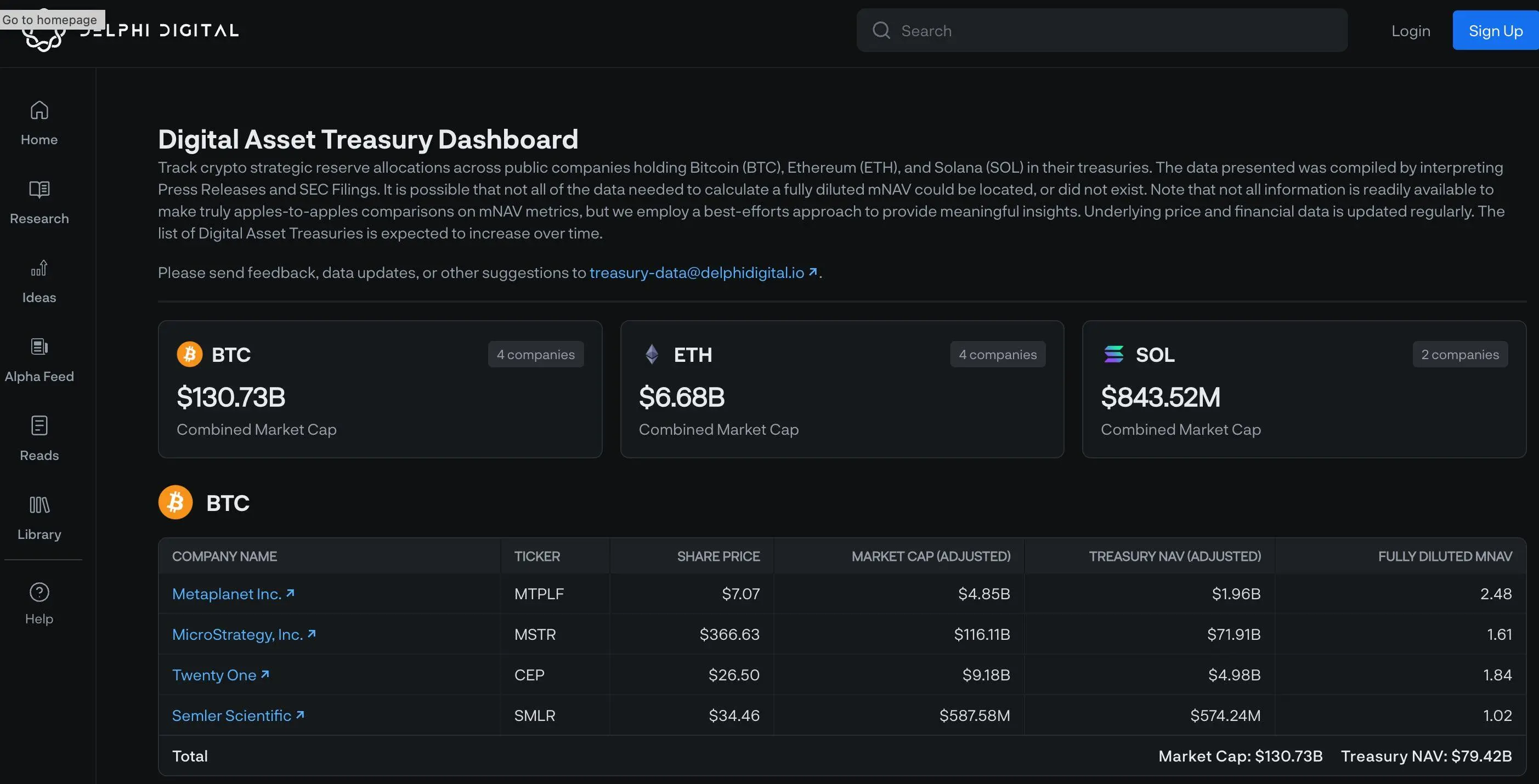

2、Delphi Digital

简介:Delphi Digital的加密储备公司数据表包括BTC、ETH和SOL三种,但录入公司较少,其中录入BTC储备公司共4种(Strategy、Metaplanet、Twenty One和Semler Scientific),录入ETH储备公司4种(Sharplink Gaming、BitMine Immersion Tech、BTCS Inc和Bit Digital Inc)、录入SOL储备公司2种(DeFi Development Corp和Upexi)。Delphi Digital的数据表包括公司名称、股票Ticker、股价、市值、加密资产价值和M(上文中市值除以加密资产价值的M值)。(数据来自SEC和新闻公告。)

评价:Delphi Digital 的数据表较为简单,只能查到一些较早或知名的加密储备公司,对于一些新晋储备公司未录入数据,且对于Blockworks,Delphi Digital的MANV的数据也较为单一,只能算作一个普通的加密储备公司数据查询备选。

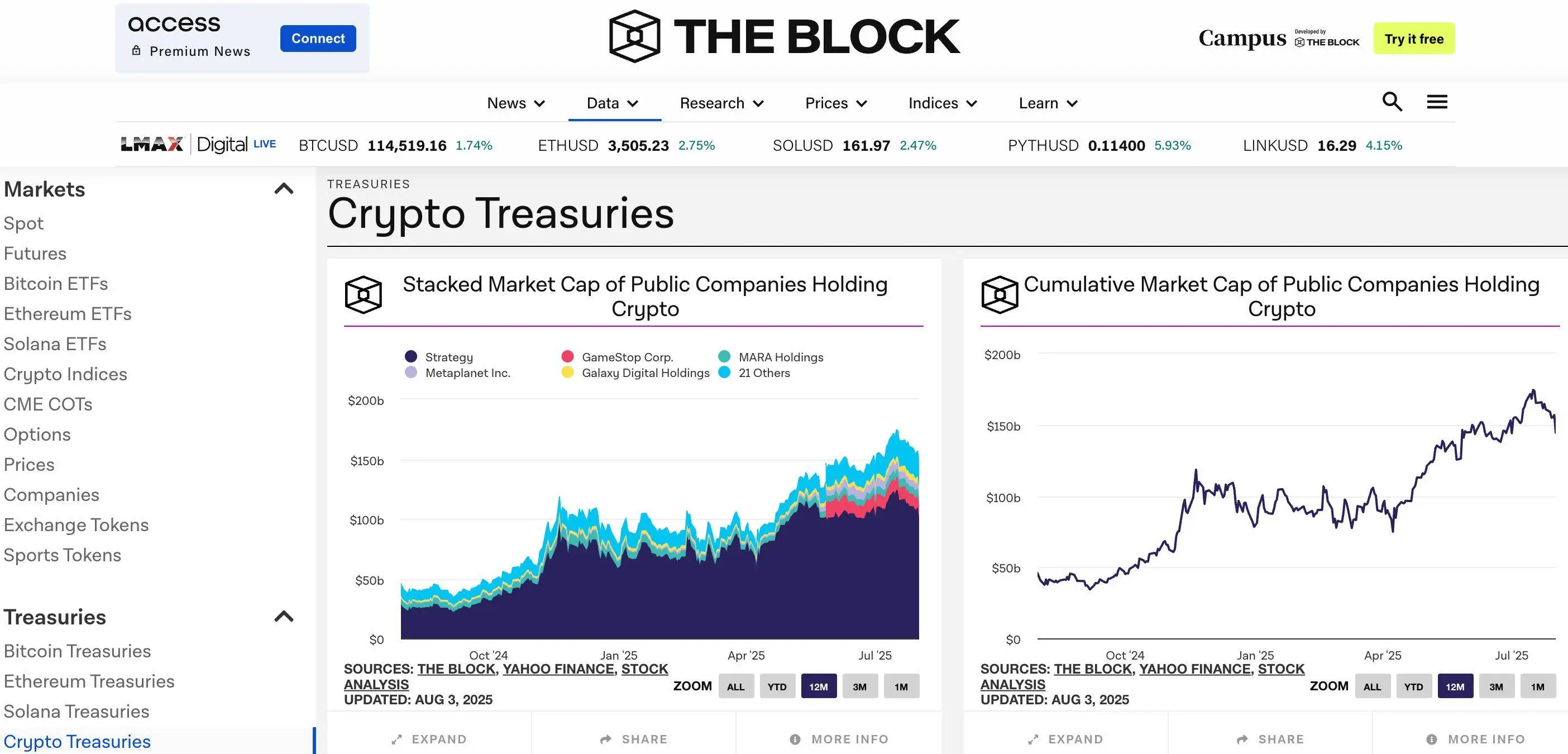

3、The Block

简介:The Block的加密储备公司数据表分为四部分,BTC、ETH和SOL还有综合加密储备企业数据,共录入了 26 个加密储备公司。其数据涵盖主流的加密储备公司,数据表包括:加密储备公司市值、加密储备公司持有代币市值、单个主流储备公司的代币持仓、单个代币的储备公司总持有量。

评价:图表上看不如Blockworks。部分加密储备数据来源于DUNE平台,所以持仓更新较慢,数据并不算特别准确。

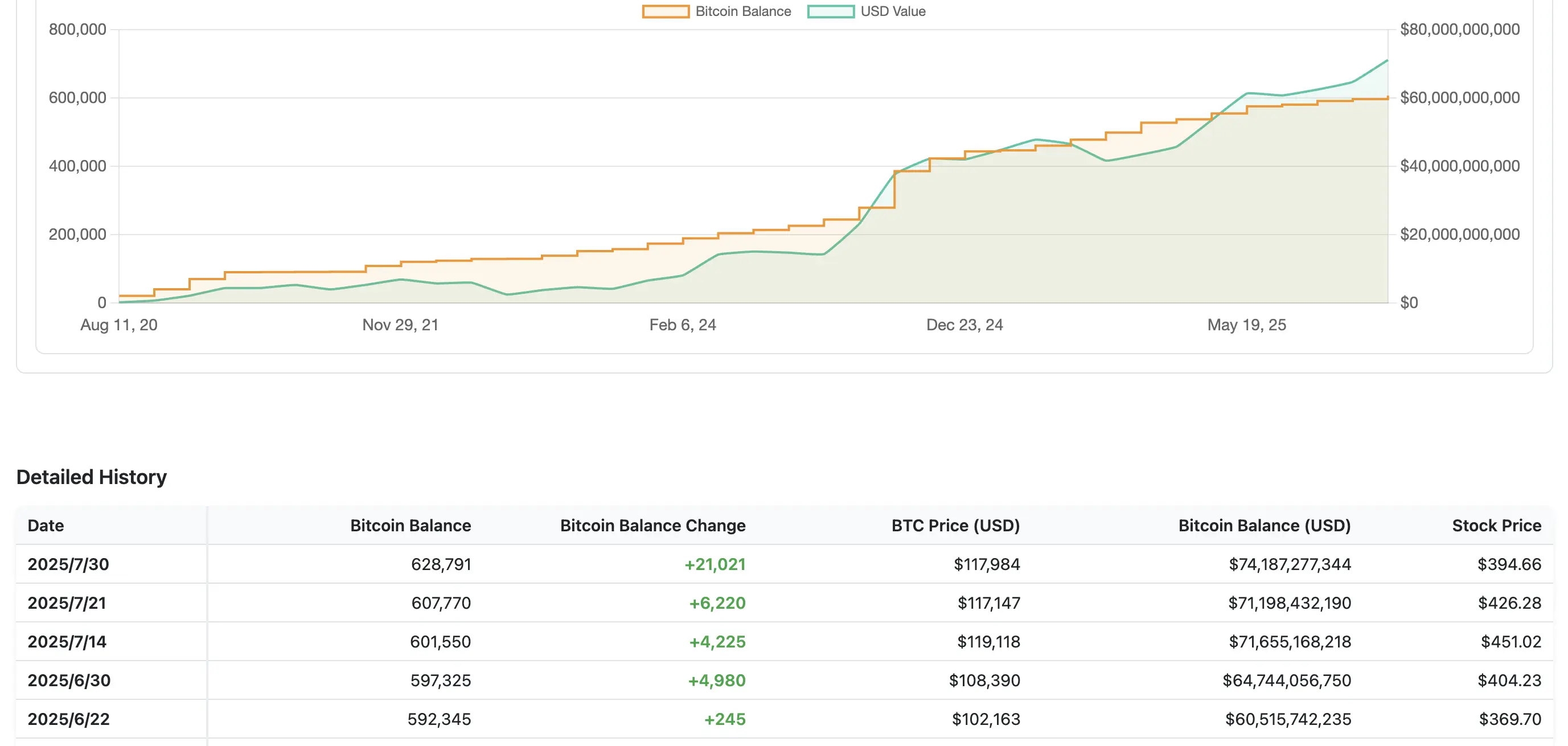

4、cryptotreasuries.info

简介:cryptotreasuries.info共分为三类加密储备,BTC、ETH和SOL,但SOL并未录入任何公司,其中BTC储备公司录入较多,此外,平台还给出了相关代币的价格走势。

该平台数据栏包括:公司名称和股票Ticker、代币持有量和总价值、30/90天和1年的每股BTC收益和MNAV。

评价:cryptotreasuries.info为今日所有查询工具中录入BTC储备公司最多的平台,但ETH储备较少,且SOL储备公司暂无(未更新),该平台还绘制了储备公司增持代币数据和股价走势对比图。

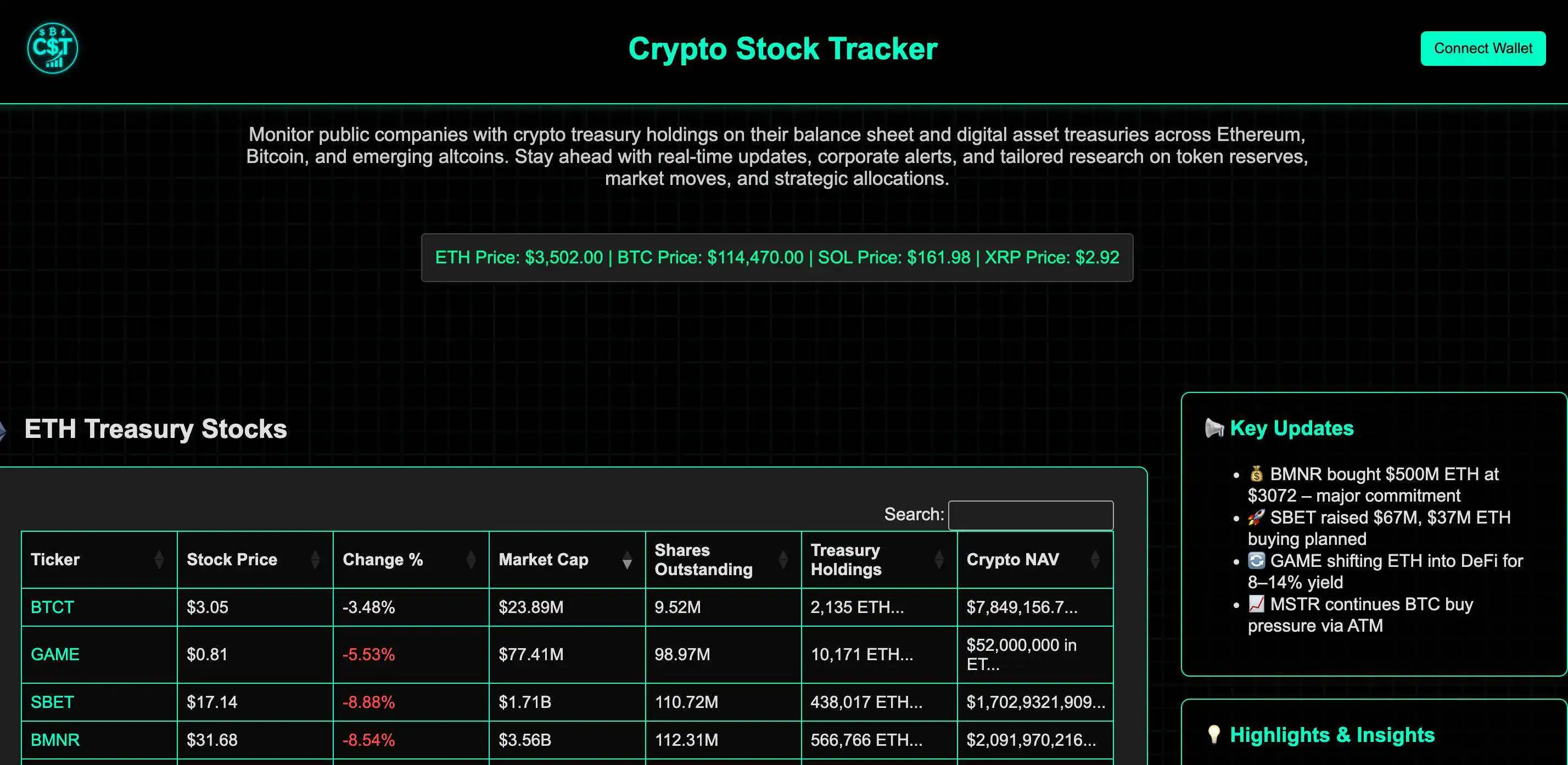

5、Crypto Stock Tracker

简介:Crypto Stock Tracker数据表包括股票Ticker、股价和股价日内涨跌幅、市值和流通股、持有加密代币数量和总价值。目前涵盖BTC、ETH、SOL和XRP储备公司,每种代币的储备公司录入较多,界面右侧有近期增持的消息和即将进行增持的加密储备公司最新消息,还包括其平台近期更新信息。

评价:Crypto Stock Tracker的 X 账号创建于 7 月,属于加密储备火热时顺势建立的新数据平台,录入的加密储备公司较多,加密储备相关观点部分还不错,相比其他平台,其多出了股价和流通股数据,也就是储备公司市值数据,对考虑买入美股玩家较为友好,若未来更新及时,可列入未来加密储备数据观察列表。

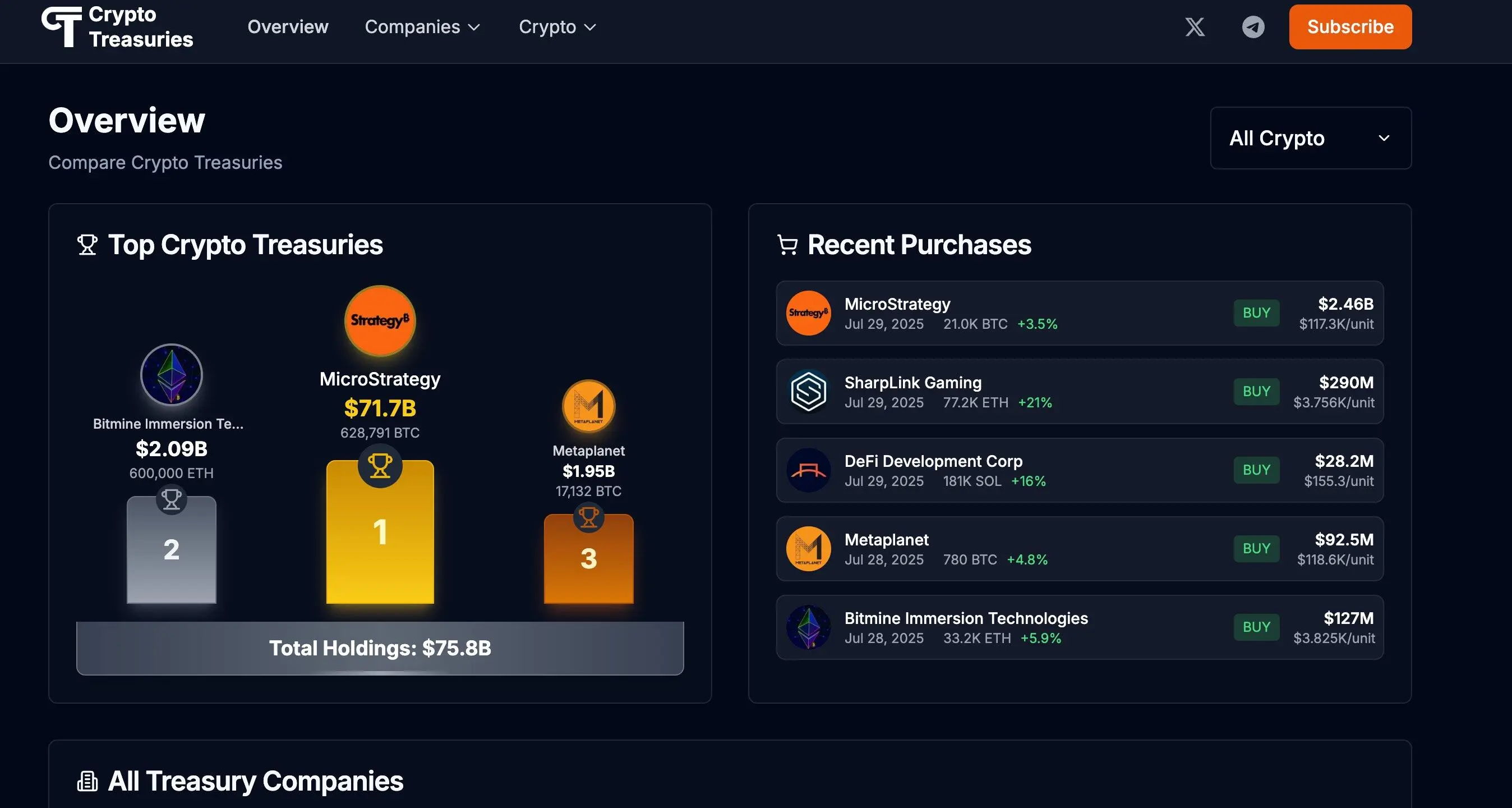

6、cryptotreasuries.com

简介:cryptotreasuries.com是7月份新出的加密战略储备公司数据和分析平台,目前录入的加密储备公司数量较少,包括2个BTC储备公司Strategy和Metaplanet,2个ETH储备公司Bitmine和Sharplink、2个SOL储备公司Upexi和DeFiDevelopment Corp,还有一个HYPE储备公司Hypreion DeFi。

其综合数据栏包括:公司名称、股票Ticker、持有的加密储备代币数量和总价值、股价、市值和MNAV。

评价:cryptotreasuries.com界面简单直观,录入公司较少,优势在于平台列出了近期增持代币的储备公司数据和增持比例。作为新平台,未来或将增加更多加密储备公司数据,属于“潜力股”。

结语

目前上市公司转型或进阶为加密储备公司的实体的更新速度相对快,比如基本每周都会有几家新的上市公司宣布买入或即将 BTC 作为战略储备,除了直接买入外,还有包括融资或增发股票的方式来增持加密储备(新闻公布后需要一定时间来筹集资金)。还有一些部分即将合并的实体并不容易计算其市值和加密储备数量,所以很难列出特别细致的数据,现实的总加密储备公司数据上有一定偏差。此外,以上部分平台还录入了加密矿企的储备数据。

但总体来说还不错,以上提到的储备公司查询网址/工具中,Blockworks 较为领先,无论是在图表还是数据图上,此外,几个新平台的界面和数据分类上也各有优势,Crypto Stock Tracker是以上平台中唯一录入了XRP储备的平台,cryptotreasuries.com 是以上所有平台中唯一录入 HYPE 的平台,cryptotreasuries.info 为今日所有查询工具中录入 BTC 储备公司最多的平台。

值得注意的是,以上所有平台均未更新 Sharplink 的 ETH 持仓数据(昨日 Sharplink Gaming 增持 15,822 枚 ETH,其 ETH 储备升至 480,204 枚,总价值达 16.2 亿美元)。