撰文:Tiger Research

编译:AididiaoJP,Foresight News

摘要

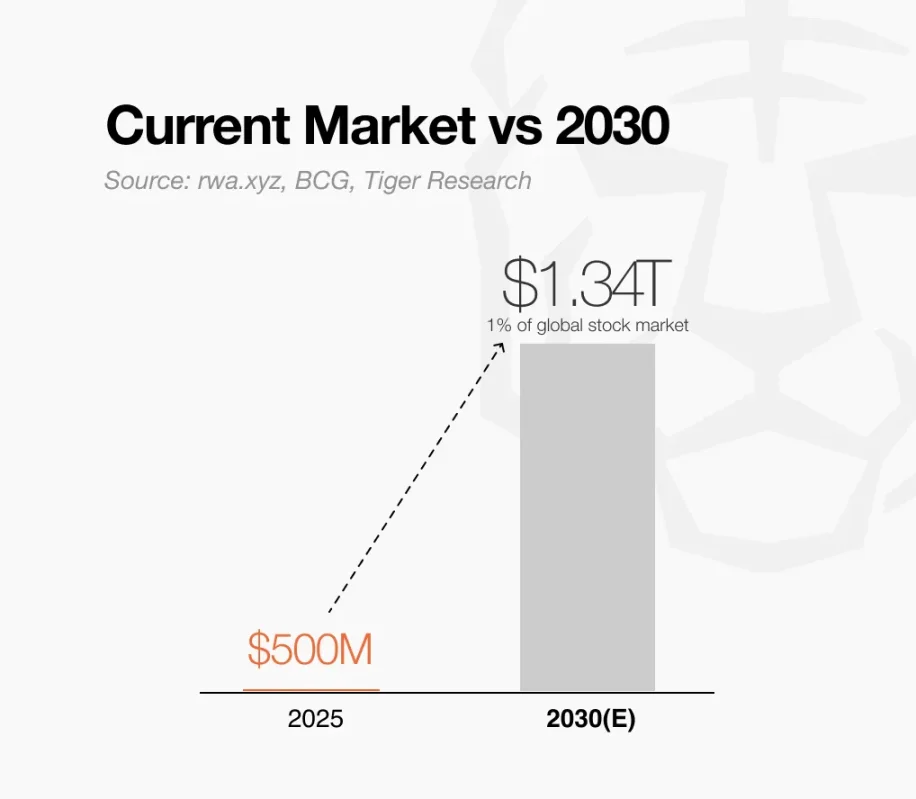

市场机遇:代币化股票市场目前规模为 5 亿美元,但如果全球股票中能够有 1% 的市场实现代币化,到 2030 年市场规模可能达到 1.34 万亿美元。这意味着 2,680 倍潜在增长,主要驱动力是 2025 年监管明确性和成熟的基础设施的双重推动。

价值主张:代币化股票支持全天候全球交易,并允许代币化股票所有权。其关键差异化在于与去中心化金融(DeFi)的整合,使投资者能够在不抛售股票的情况下,将其作为抵押品用于借贷和获取收益。

成功原因:与其他需要从零创造需求的现实世界资产(RWA)不同,代币化股票直接切入规模达 134 万亿美元的全球股票市场,并针对明确的痛点。现有需求与可解决的痛点相结合,使其成为最具大规模采用潜力的 RWA 类别。

加密行业和传统金融的融合:边界模糊化

传统金融与加密行业正在相互靠拢。

一方面花旗集团和美国银行等机构正在准备发行稳定币。另一方面,Injective 和 Backed Finance 等项目正在将苹果和特斯拉等股票代币化并上链。

随着传统机构采用加密技术,以及 Web3 项目将股票代币化,两个行业之间的边界正在逐渐消失。

这种融合在美国“加密周”之后加速。“加密周”是一段以数字资产为重点的监管活动期,《GENIUS 法案》的通过将稳定币纳入联邦监管框架。华尔街与 DeFi 之间不再是竞争关系,而是日益相辅相成。

传统金融有明确的动力整合加密技术。除了潜在的创新外,加密市场已证明其盈利能力,而传统金融品牌可以提供加密行业目前缺乏的信任。但反方向的逻辑即加密平台为何要代币化股票则不那么明显。市场仍处于早期阶段,动机多种多样且具有投机性。

本报告通过分析代币化股票市场的结构及其主要参与者,探讨这一问题。

什么是代币化股票市场?

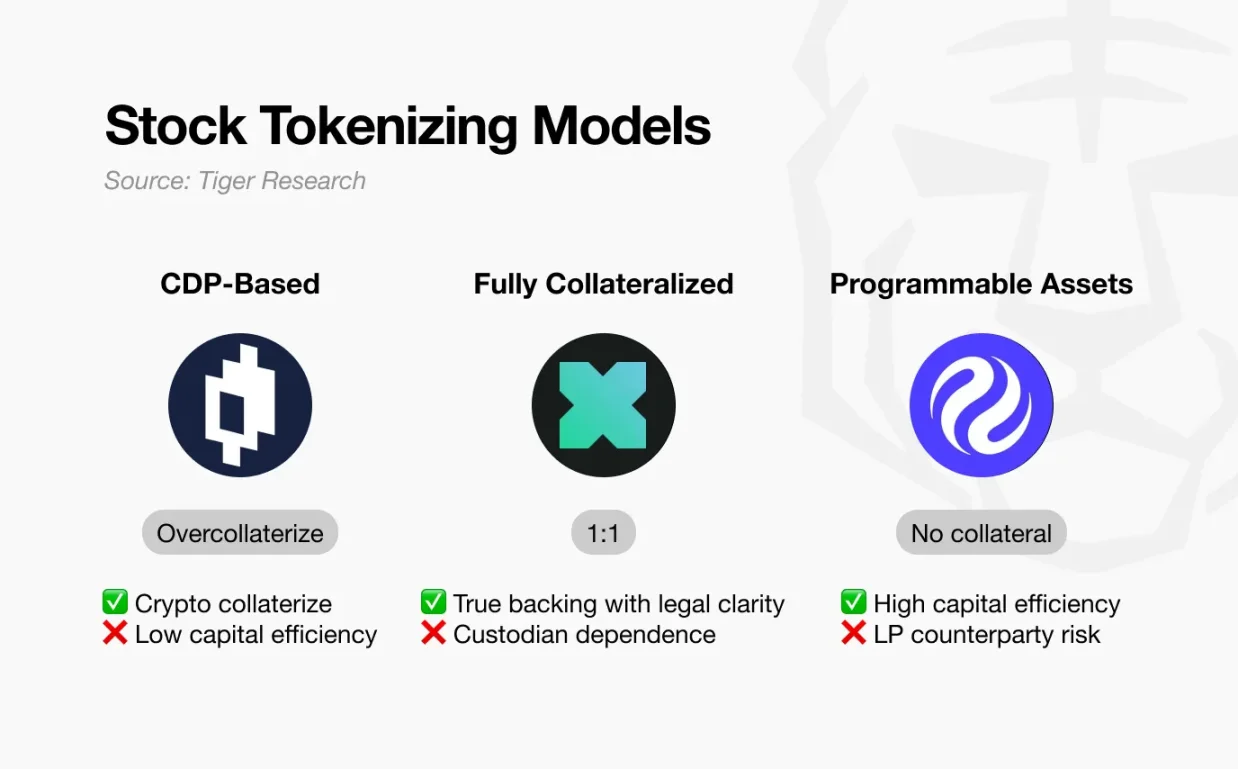

代币化股票市场是指将传统股票转换为区块链上的数字代币。这些代币旨在反映标的股票的价值,但通常不附带股东权利。大多数代币化股票以衍生品形式存在,而非直接持有股票。

尽管第一波代币化股票在 2021 年就已出现,但大多数早期模型(如 Mirror Protocol)由于低效率和系统性风险(尤其是在 Terra 等生态系统中)未能实现规模化。近期的方法引入了改进机制,具有更强的资本动态和合规框架,以 Injective 和 xStocks 为代表。

代币化股票的关注度随着 RWA(现实世界资产)趋势的兴起而急剧增长,RWA 已成为加密市场的关键叙事。

除了这些直接优势外,代币化股票通过可组合性实现了新的用例。由于它们存在于传统监管框架之外,可以作为借贷协议的抵押品,或在 DeFi 应用中生成收益。

例如印度尼西亚的投资者若想获得特斯拉股票的敞口,传统方式需要开设外国经纪账户、填写文件并支付货币转换费用,且只能在有限的交易时间内操作。通过代币化股票,同一投资者可以通过智能手机即时购买特斯拉代币,并将其部署于 DeFi 协议中用于借贷、提供流动性或生成收益。

可行情景:全球股票 1% 的代币化

代币化股票市场仍处于早期阶段。根据 rwa.xyz 的数据,当前市场规模约为 5 亿美元。与 134 万亿美元的全球股票市场相比,这一数字仅占 0.0004%。然而如果未来十年内全球股票中仅有 1% 实现代币化,市场规模可能增长至 1.34 万亿美元,是目前规模的 2,680 倍。

2025 年的转折点

2025 年下半年可能成为关键转折点。尽管仍处于早期阶段,但 Solana 生态系统内的代币化股票交易量在一个月内从 1,500 万美元飙升至 1 亿美元,增长 566%。

更重要的是受监管参与者的入场。主要金融科技公司正在全球范围内扩展代币化服务,Robinhood 宣布在欧洲推出相关业务。随着市场从北美扩展到欧洲和亚洲,监管明确性将成为催化剂。特别是一旦股票代币化在欧盟的 MiCA 框架下启动,市场预计将迅速扩大。

2030 年成功的条件

到 2030 年实现全球股票市场 1% 的代币化需要明确的理由。投资者必须有强烈的动力从传统系统转向代币化平台。这一转变只有在四个关键条件共同作用下才会发生。

第一,必须证明成本节约。

理论上,经纪、结算和管理费用可减少 50%-70%,这需要在实践中得到验证。如果代币化能显著降低外汇和跨境交易成本,将为全球投资者提供强有力的替代方案。

第二,全天候交易的实用性需得到验证。

代币化股票应支持亚洲、欧洲和美国市场的连续交易。通过消除传统交易所的时间限制,它们可以提供更高的流动性,并实时响应全球事件,从而提高整体交易效率。

第三,基于 DeFi 的二次收益生成必须成为核心功能。

代币化股票不仅应作为可交易资产,还应成为 DeFi 协议的基础组成部分。如果投资者能将其用于抵押借贷、基于 AMM 的期权、流动性提供和自动化投资组合策略,他们就能在不抛售的情况下获得额外收益。随着这些机制的成熟,它们将强化代币化的主要优势成本效率、可访问性和连续交易使脱离传统系统的吸引力日益增强。

代币化股票市场的关键参与者

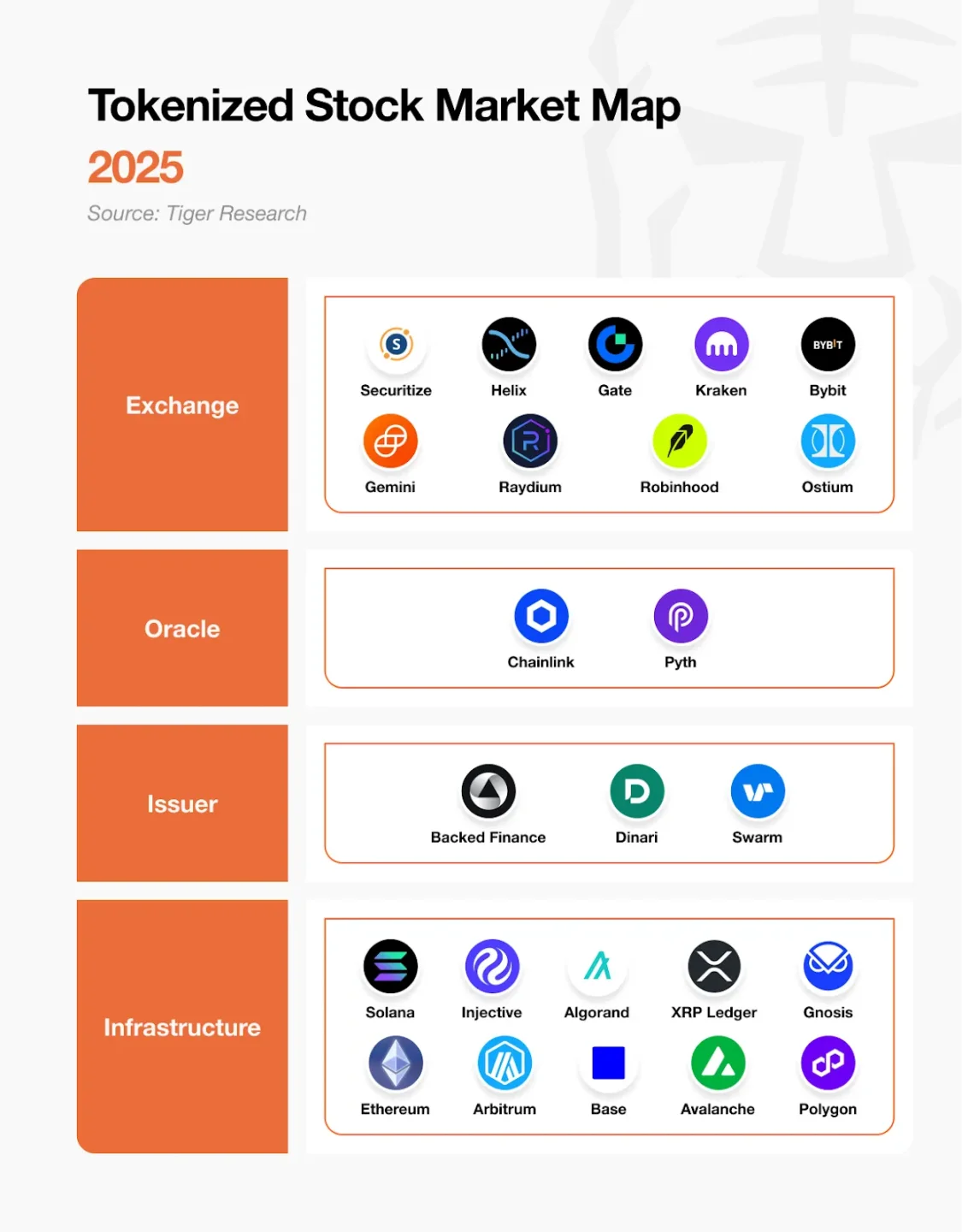

代币化股票市场建立在四个协调运作的核心层级之上。

最底层是基础设施层,提供所有交易发生的区块链网络。其上是发行方,负责创建传统股票的代币化表示。为了确保准确的价格跟踪,预言机提供实时市场数据并维护与标的资产的链接。最后交易所允许投资者买卖代币化股票。

一个功能完善的代币化股票生态系统需要所有四个层级。缺少任何一层,系统都将缺乏安全发行、定价和交易的必要组件。

代币化的实践

假设一位投资者希望通过代币化形式获得苹果($AAPL)股票的敞口。他们可以在 Helix 上以高达 25 倍杠杆交易 iAAPL,在 Kraken 上购买 Backed Finance 发行的 $xAAPL 现货代币,或作为欧洲居民通过 Robinhood EU 全天候访问美国股票。每家交易所都在不同的监管环境和交易模式下运作,满足不同投资者的需求。

为了使代币化股票准确反映真实股票价格,可靠的市场数据至关重要。例如,Chainlink 从纳斯达克获取苹果股票的实时价格并上传至链上。它还提供储备证明,验证每个代币是否以 1:1 的比例由相应的苹果股票支持。这确保了投资者可以信任代币的价格完整性。

发行方将传统股票转换为代币化资产。Backed Finance 在瑞士银行托管实际的苹果股票,并以 1:1 的比例发行 $xAAPL 代币。相比之下,Injective 的 $iAAPL 使用 iAssets 而不持有标的股票,通过预言机数据合成跟踪价格,实现无需实物结算的杠杆交易。这两种方法代表了将传统股票与区块链基础设施连接的不同路径。

所有交易和代币转移均在区块链网络上进行。在 Solana 上,Backed Finance 的 xStocks 以低延迟和最低费用交易。Injective 支持基于订单簿的高性能交易。在以太坊和 Arbitrum 上,Dinari 的 dShares 在美国监管合规下运作。每条链提供不同的技术能力,以满足代币化股票平台的基础设施需求。

代币化股票市场的主要参与者

代币化股票市场的关键参与者基于不同的策略和能力塑造生态系统。以下是主要公司及其当前定位的总结:

Injective:代币化股票永续合约领域的领导者。截至 2025 年上半年,累计交易量超过 10 亿美元。通过其 Helix DEX,提供高达 25 倍的杠杆,推动衍生品领域的流动性。

xStocks(Backed Finance):占据市值前 10 的代币化股票的 80%。采用 1:1 支持模型,股票托管于瑞士银行,并在 Solana 生态系统中广泛采用。

Robinhood:2025 年扩展至欧洲,提供超过 200 种代币化的美国股票和私人股票。在 Arbitrum 上提供零费用交易,支持 24/5 交易。

Gemini:与 Dinari Global 合作,为欧盟投资者提供 60 多种代币化股票。符合 MiFID II,在欧洲监管框架内提供服务。

Securitize:代币化现实世界资产的领先者,包括美国国债代币如 $BUDIL。还提供总计 3.12 亿美元的股票代币化产品,其中最大的单一资产部署在 Algorand 上。

Chainlink:提供关键的数据基础设施,包括实时股票和 ETF 价格馈送,以及资产支持的储备证明验证。

代币化股票在 RWA 市场中的作用

有限但最具可行性的细分市场

代币化股票只是更广泛的现实世界资产(RWA)市场中的一个细分领域。如果没有监管明确性,其采用将受到限制。然而这一障碍已经开始松动。Robinhood 已宣布在欧洲提供代币化股票服务,其他主要平台也在跟进。随着更多司法管辖区与这些发展保持一致,监管接受度可能会扩大。

已验证的需求与明确的痛点

这一市场的优势在于其基本面。股票已经是广泛交易的资产,需求明确。同时交易过程长期存在低效问题,尤其是在访问、结算速度和地理限制方面。已验证的需求与可解决的痛点相结合,使股票成为代币化的理想起点。

与其他需要首先生成需求的 RWA 类别不同,代币化股票直接建立在 134 万亿美元的全球股票基础上。代币化的案例因其切实优势而增强:更低的成本、更广泛的访问、全天候交易和 DeFi 整合。随着监管框架的成熟,这些优势将推动代币化股票的加速采用。

声明:本内容为作者独立观点,不代表 CoinVoice 立场,且不构成投资建议,请谨慎对待,如需报道或加入交流群,请联系微信:VOICE-V。