Недавно обнародованная жалоба обанкротившегося криптокредитора Genesis раскрывает внутренние коммуникации в его материнской компании Digital Currency Group (DCG), свидетельствующие о том, что руководители знали о финансовых злоупотреблениях и надвигающихся юридических рисках, связанных с их контролем над Genesis.

Согласно заявлению, поданному в Канцелярию суда штата Делавэр, финансовый директор DCG Майкл Крэйнс признал риск того, что Genesis может считаться «альтер эго» DCG.

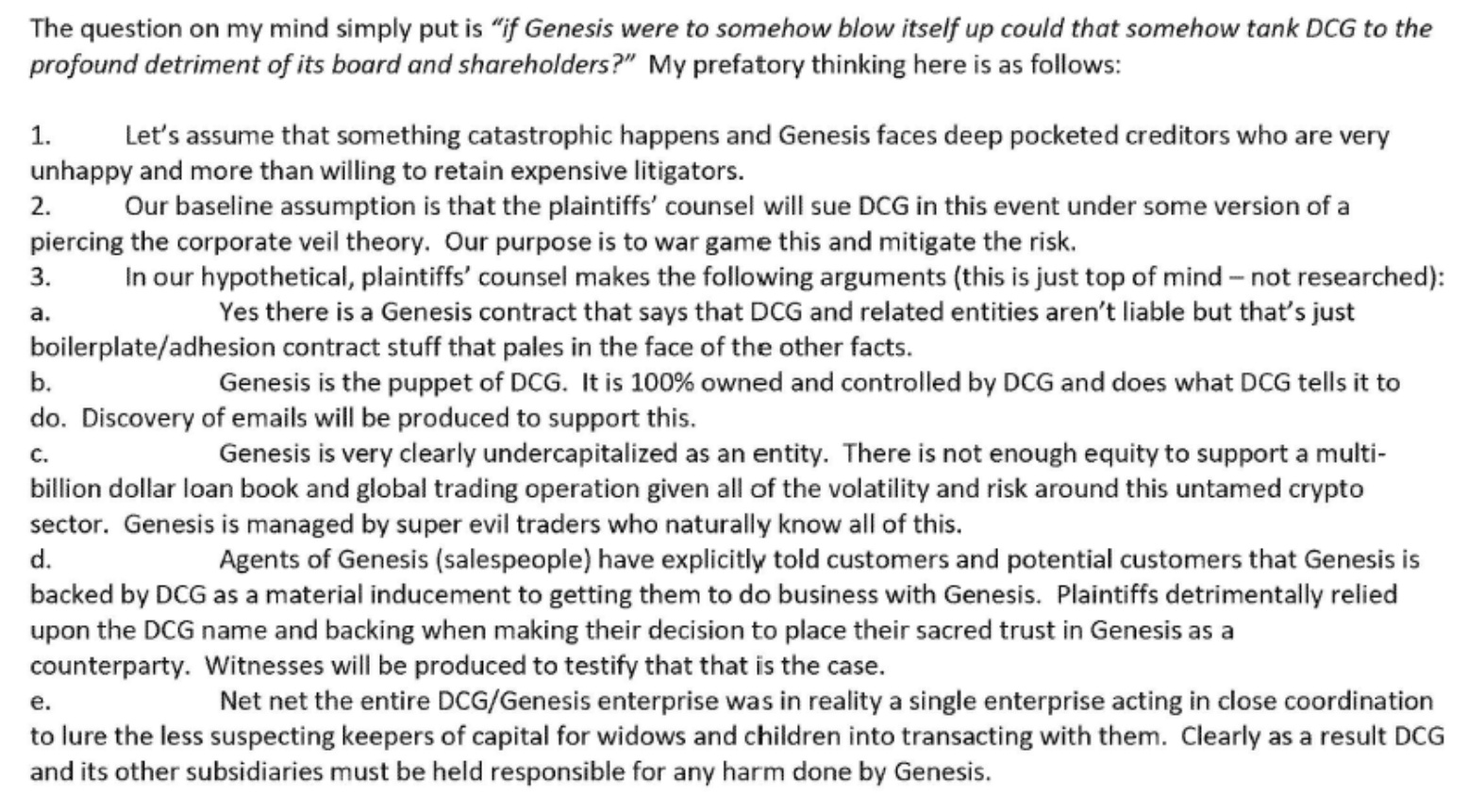

В конфиденциальной записке, представленной бывшему генеральному директору Genesis Майклу Моро и другими руководителям, Крэйнс изложил соображения по подготовке к юридическим аргументам, которые может выдвинуть будущий истец, если Genesis рухнет. Записка, приложенная к жалобе, отражает претензии, которые сейчас являются центральными в иске.

«Вопрос, который у меня на уме, звучит так: «Если Genesis каким-то образом взорвет себя, может ли это каким-то образом погубить DCG, нанеся огромный ущерб ее совету директоров и акционерам?» Мои предварительные соображения здесь таковы», — написал Крэйнс Моро, дав понять, что они готовятся к неминуемому судебному разбирательству.

Записка, которую Крэйнс написал Моро. Источник: Genesis.

Записка, которую Крэйнс написал Моро. Источник: Genesis.

DCG проигнорировал предупреждения о рисках

В заявлении также раскрывается, что DCG наняла сторонних консультантов по рискам, которые выдавали предупреждения, которые либо игнорировались, либо учитывались слишком поздно. Внутренние документы показывают, что DCG признала, что Genesis «летела вслепую», когда ее кредитный портфель раздулся с 4 миллиардов долларов до 12 миллиардов долларов.

Внешние аудиторы еще в 2020 году выявили «существенные недостатки и слабости» в системе финансового контроля Genesis.

Сторонние консультанты по рискам выносят DCG серьезные предупреждения. Источник: Genesis.

В Genesis был сформирован так называемый комитет по риску «заражения», чтобы смягчить воздействие. Однако его первое заседание состоялось лишь через девять месяцев после одобрения советом DCG. Сообщается, что Крейнс пошутил, что задержка «просто немного облегчила мне будущую дачу показаний».

В жалобе также описывается токсичная корпоративная культура, в которой от сотрудников Genesis ожидалось, что они будут служить интересам DCG в ущерб надлежащему управлению.

Один из инсайдеров написал, что DCG поддерживала Genesis в живых, «чтобы она могла разграбить баланс… поддержать Genesis, создать вид стабильности, а затем занять, пока они могли бы, чтобы получить из нее наличные». Сотрудники Genesis внутри компании называли обстановку в фирме «культурой подчинения».

«Это не просто технические споры по поводу внутрифирменного учета, — заявил Комитет по надзору за судебными разбирательствами Genesis. — Жалоба Делавэра раскрывает преднамеренную схему DCG и Барри Силберта по разграблению Genesis в момент ее краха».

Публичный обман и спорные транзакции

В иске также утверждается, что имел место публичный обман. Персоналу Genesis было приказано читать заготовленные сообщения после краха Three Arrows Capital (3AC), в то время как руководители DCG, включая Барри Силберта, ретвитнули посты, в которых преуменьшался кризис.

Кроме того, жалоба проливает свет на две спорные сделки. Они включают в себя вексель от 30 июня 2022 года и сделку «туда и обратно» от сентября 2022 года, обе из которых были оформлены как попытки скрыть неплатежеспособность и ввести в заблуждение кредиторов.

Genesis пытается взыскать более 3,3 млрд долларов с DCG, Силберта и других инсайдеров.