Криптовалютный рынок лихорадит на фоне ближневосточного кризиса. За первые сутки биткоин рухнул более чем на 5%, а общая капитализация криптовалют просела на 7,2% за два дня. Похоже, инвесторы решили, что сейчас самое время избавиться от рисковых активов.

Куда катится биткоин?

Трейдеры уже вовсю обсуждают, до каких глубин может докатиться «цифровое золото». Популярный аналитик Роман (Roman) считает, что мы еще увидим уровни $55 000–57 000:

«Рост объемов торгов при падении цены обычно указывает на сильный нисходящий тренд. Это подтверждает мою идею о том, что мы revisit область $55 000–57 000 перед возможным разворотом».

А вот трейдер Тони Гинеа (Toni Ghinea) и вовсе ожидает падения до $54 000. По его мнению, октябрь будет «медвежьим» месяцем для биткоина.

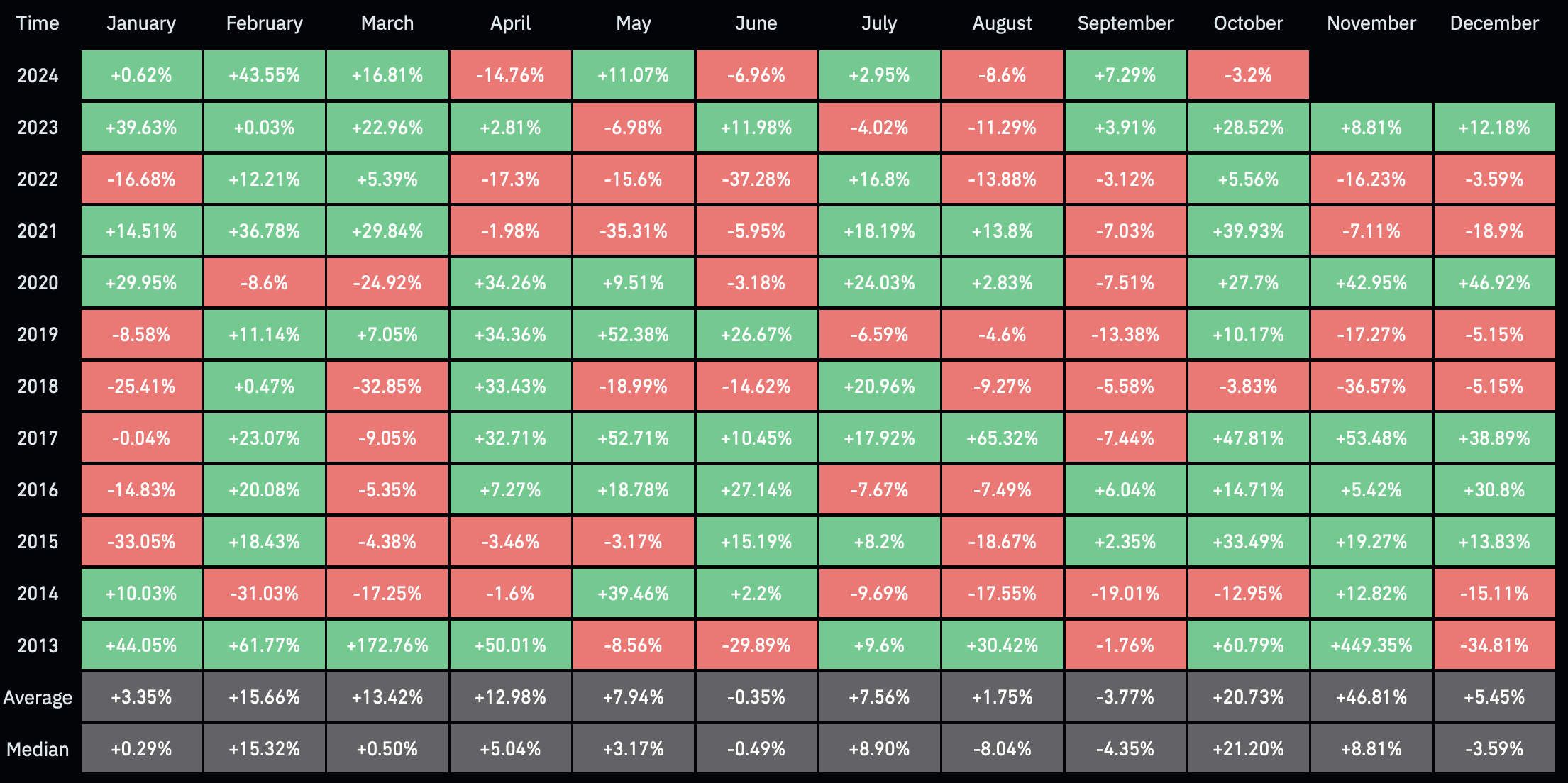

Интересно, что еще недавно аналитики наперебой предрекали биткоину рост на 23% в октябре. Видимо, не учли фактор геополитической нестабильности. Эх, знать бы, где упадешь — соломки бы подстелил!

Не все так плохо?

Впрочем, некоторые эксперты сохраняют оптимизм. Трейдинговая фирма QCP Capital отмечает:

«Похоже, мы нашли некоторую поддержку на уровне $60 000, но дальнейшая эскалация может опустить нас намного ниже, возможно, до уровня $55 000. Геополитика Ближнего Востока сейчас выходит на первый план, но неглубокая распродажа говорит о том, что рынок по-прежнему хорошо настроен на рисковые активы. Эта небольшая неудача не должна отвлекать от общей картины».

Криптотрейдер и аналитик Михаэль ван де Поппе (Michaël van de Poppe) также считает, что мы близки к локальному дну:

«Думаю, мы довольно близки к минимуму, возможно, будет еще одно падение до $60 000, и затем разворот. Рынки упалм немного глубже, чем я ожидал, но все еще следуют моему сценарию».

Что дальше?

Рынок криптовалют в очередной раз демонстрирует свою чувствительность к внешним факторам. Дальнейшее обострение ситуации на Ближнем Востоке может оказать дальнейшее давление на цифровые активы.

Однако не стоит забывать, что биткоин уже не раз доказывал свою устойчивость к потрясениям. Возможно, текущая коррекция — это лишь небольшая передышка перед новым ралли. В мире криптовалют предсказать что-либо наверняка — задача не из легких.