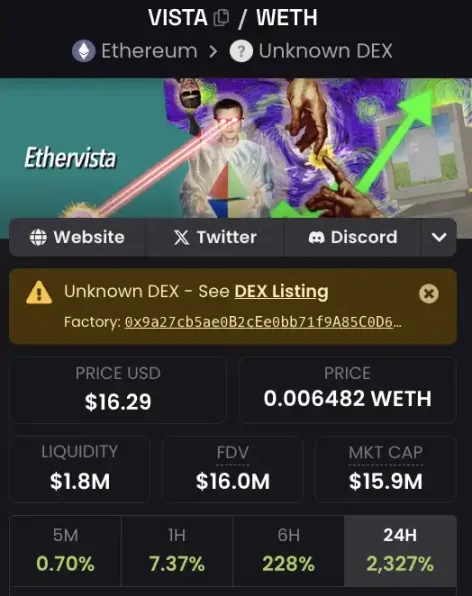

今日,一个诞生 1 日、名为「VISTA」的新代币用一个下午的时间涨幅超 10 倍,而在 Dexscreener 上,VISTA 的详情信息还提示为「未知 DEX」。VISTA 来自一个刚开始运行 1 日的 DEX EtherVista,其自称为「挑战 Uniswap 的 DEX」,被一些代币持有者称为「以太坊上的 Pump.fun」,目前已有数个代币在 EtherVista 部署发行。

EtherVista 是什么?

EthervVsta 称,其机制特色在于挑战了 Uniswap 的 AMM 模式。

根据 EtherVista 的六页白皮书表述,EtherVista 标准引入了一种新的模式,费用只以 ETH 支付,并分配给所有参与这个池子的流动性提供者和代币创建者,每次交易都通过一种新机制来分发奖励,同时保持较低的 Gas 费。与 Uniswap 不同的是,EtherVista 模式的核心特性是做市商和创建者从交易量中获益,而不是单纯依赖代币价格,这样就鼓励了长期投资,而不是短期的价格炒作。投资者也可以通过一种延迟的流动性撤回机制来获益,这样的机制可以防止快速套现跑路的情况。

简单来说就是,一般基于 Uniswap AMM 机制创建代币的开发者可以设置买入卖出费用,比如每次交易代币的 5%,并以此获益。当代币价格上涨之后,开发者的收益也会随之增加,就可能会在获得足够收益后卖出代币「跑路」。但在 EtherVista 中,开发者只能根据 EtherVista 设定的智能合约收取交易费用,并以 ETH 作为结算。比如智能合约设定买入平台代币 VISTA 时手续费为 10U,卖出时为 15U,不管 VISTA 的价格如何,在手续费这个渠道上,开发者都只能通过交易次数获益,降低了「赚够跑路」的风险。

EtherVista 智能合约会维护一个数字序列,称为「欧拉数列(Euler)」,这些数字会在每次 ETH 转移到合约时更新。每个欧拉数是根据前一个欧拉数加上交易费用和流动性提供者代币总供应量的比率计算出来的,通过这个机制,可以确保每个流动性提供者在每笔交易中都能准确获取应得的收益。

每次交易,EtherVista 都会收取 ETH 费用,这个费用会在流动性提供者和协议之间进行分配。每个池子里会有四个设置费用的变量,这些变量会根据链上的交易情况来动态计算。比如,一个池子可以设置买入费用为 10 美元,卖出费用为 15 美元。如果用户卖出代币,他需要支付 15 美元的 ETH 给流动性提供者和协议。协议的智能合约会用这部分费用建立一个稳定的价格底线,并为项目创造者提供可持续的收入。每个流动性提供者都可以随时领取自己应得的奖励。

提供流动性的用户被称为「创建者」,他们有权限设置池子的各种参数,比如费用、协议地址和元数据。这个新模式把重点从短期获利和价格波动转移到更长期的活动和项目实用性上。创建者还可以定义他们代币的链上元数据,比如网站链接、项目描述、社交媒体账号等。这些信息会在 EtherVista 平台上显示,确保用户访问的是可靠的项目信息。平台还集成了全球实时聊天功能(SuperChat),帮助用户更快地交换信息。

Ethervista 还在白皮书中表示将计划扩展到更大的市场,比如建立 ETH-BTC-USDC 的流动性池,并提供借贷、期货和免手续费的闪电贷功能,目的是成为一个多功能的一站式去中心化应用(DApp)。

协议机制

7 月 11 日,EtherVista 了第一条推特。8 月 19 日,EtherVista 表示正在「空投白皮书」,只要转发推文,官推将会以 DM 的形式发送项目白皮书。

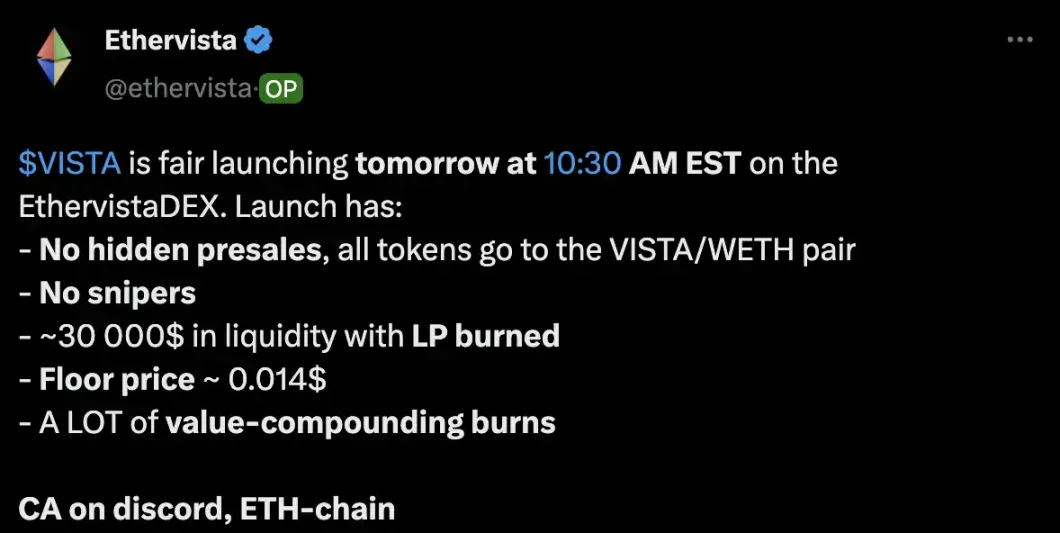

8 月 31 日,EtherVista 在官推宣布将在 9 月 1 日上午开启 VISTA 的 Fair Launch,初始流动性约为 3 万美元,并且 LP 代币将被销毁。代币的发行价大约是 0.014 美元,按照现价 18 美元计算,涨幅为 12857 倍。上线之前,EtherVista 官推声明没有预售和团队预分配,会在上线时使用团队资金以公平的方式与其他用户同时购买自己的代币。

EtherVista 的平台代币为 $VISTA,供应量固定为 100 万枚。它是一种「价值复合型的通缩代币」,也就是说,每次交易都会燃烧一部分代币,在这样的基础上,VISTA 的价值会随着交易而增长,EtherVista 以此来让 VISTA 具有对抗通胀的能力,促进代币价格的持续增长。

EtherVista 白皮书提出了一种新型的去中心化交易所模式,旨在通过引入更合理的费用分配和代币机制来解决现有问题。相比传统 AMM 模型,EtherVista 通过采用只收 ETH 的费用机制和创新的收益分配方式(比如欧拉数列),激励参与者进行长期投入而不是短期投机。平台还提供了一些独特的功能,比如 SuperChat 聊天和定制化的代币元数据展示,旨在打造一个更透明、信息更丰富的去中心化金融平台。总体来看,EtherVista 的设计有助于区块链生态系统的持续增长和稳定发展。

为了确保 $VISTA 及其他 EtherVista 项目的长期成功,平台实施了 5 天的锁仓期。这个锁仓期的设计是为了防止开发者和流动性提供者过早地撤回流动性,从而导致项目「跑路」。锁仓期的 5 天计时从代币创建者首次添加流动性时开始,确保在此期间内,代币创建者不能比其他流动性提供者更早地撤回流动性。

即使在前 5 天内流动性不能撤出,但流动性提供者可以随时领取他们的奖励。EtherVista 标识仅在 $VISTA 代币的 LP 奖励再 5 小时里已经超过 25,000 美元,且这些费用是以 ETH 支付的,这意味着费用的收集不会给 $VISTA 或 EtherVista 平台上推出的其他代币带来额外的抛售压力,降低了对项目的潜在风险。

体验教程

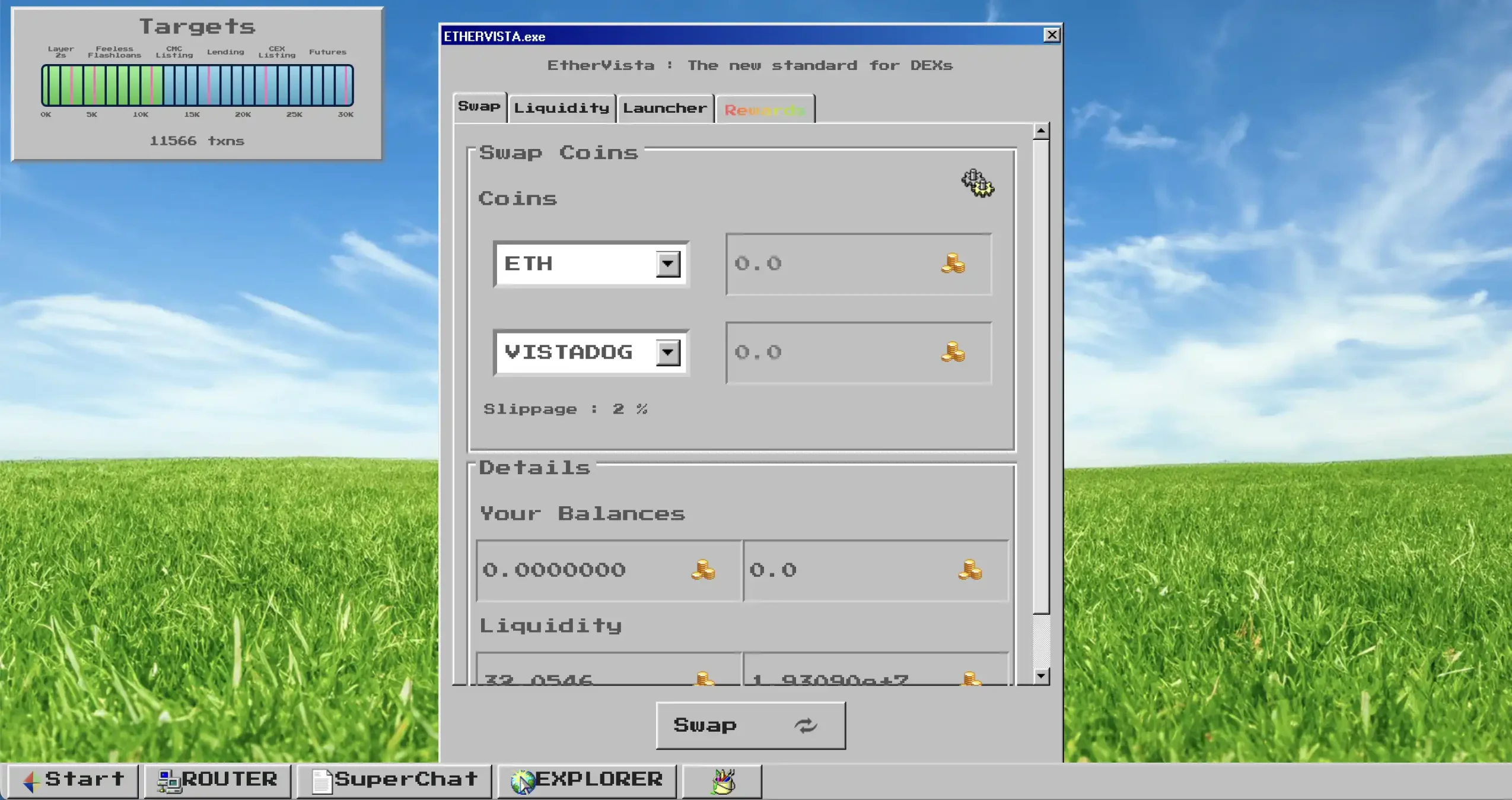

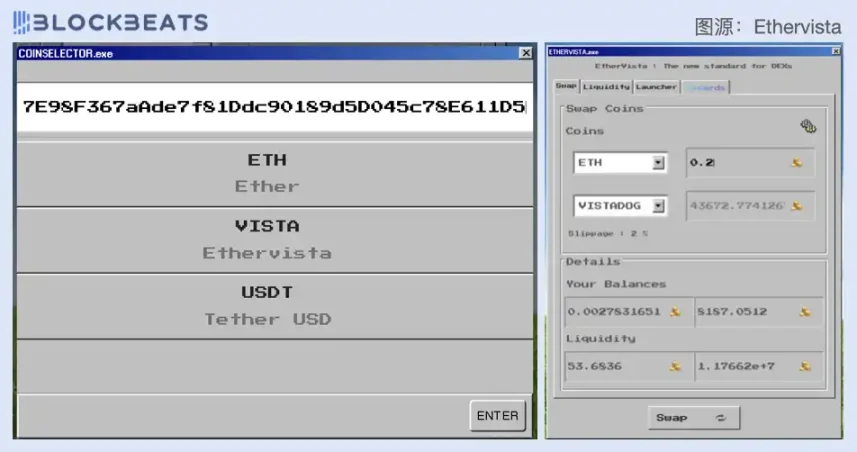

交易

EtherVista 只直接显示了 ETH、USDT 和 VISIA 的代币名称,要购买其他代币,需要在输入框中粘贴代币合约地址,点击 ENTER。然后输入购买的数额,界面会显示能够交易的代币数量和代币当前的流动性池信息。

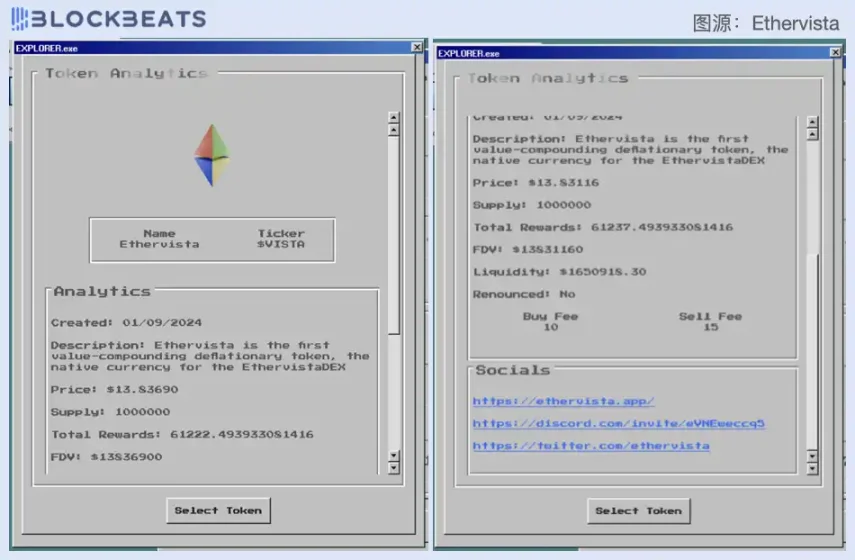

代币查询和聊天

EXPLORER 窗口可以查看平台上创建的代币信息详情,这些信息由代币创建者定义,涵盖网站链接、项目描述、社交媒体账号等。与其他一般代币信息展示格式不同的是,在 EtherVista 上可以查看代币所产生的奖励,这些奖励将会分给 LP。

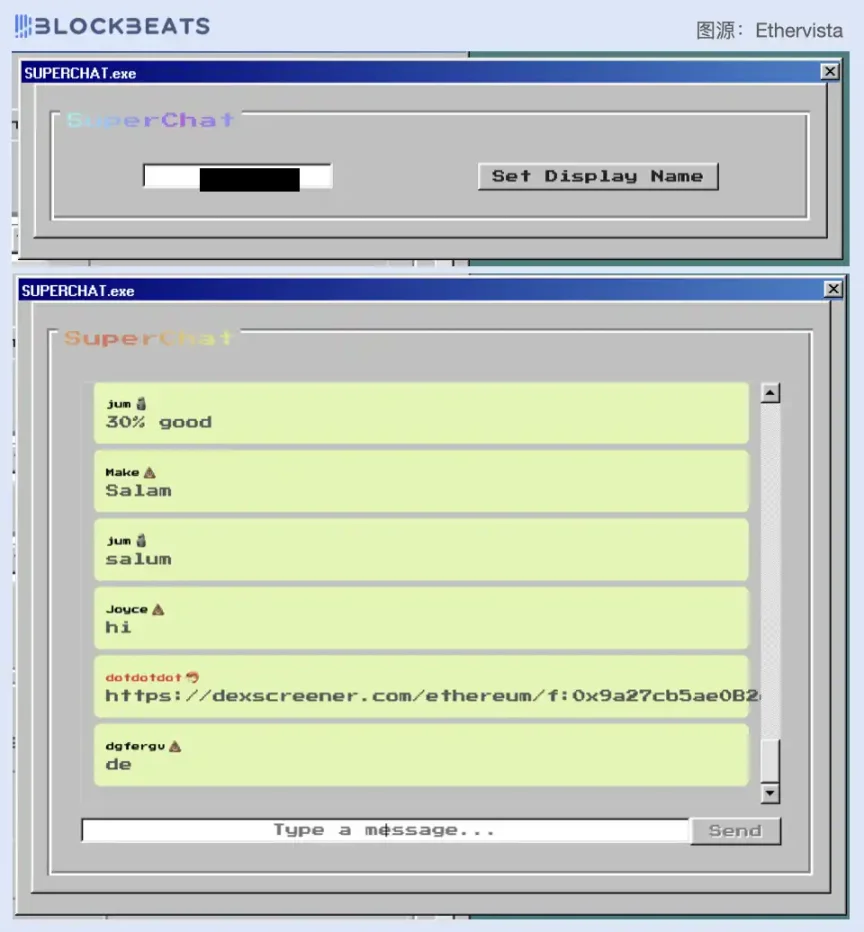

另外,Ethervista 平台集成了实时聊天功能,进入 SuperChat 窗口,设置一个用户名后就可以在界面中聊天。这个功能类似于 Pum.fun 的代币评论区,但更为简易粗糙。

热门标的&持仓情况

VISTA

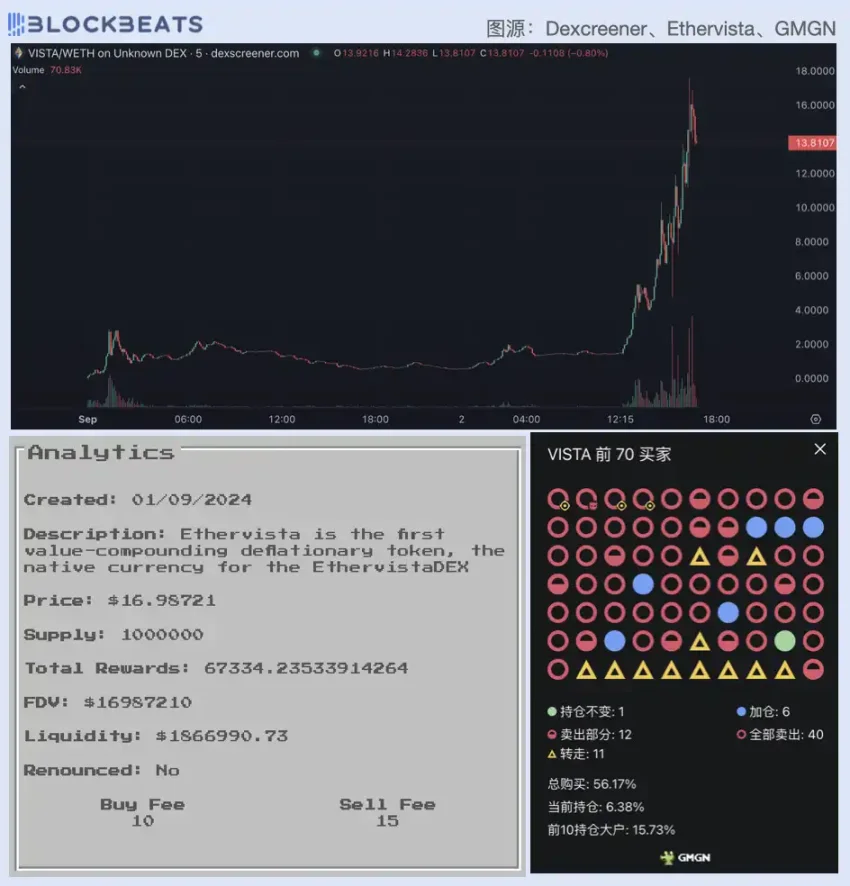

EtherVista 的平台代币为 $VISTA 上线于 9 月 1 日凌晨 0 时,今日中午,VISTA 突然开始飙升,5 小时涨幅 10 倍,交易量超 850 万美元,目前市值为 1300 万美元。EtherVista 上显示,VISTA 共为其 LP 产生了 67,334 美元的奖励。GMGN 数据显示,VISTA 前 70 名买家共购买了 56% 的代币,目前持仓份额为 6.38%。

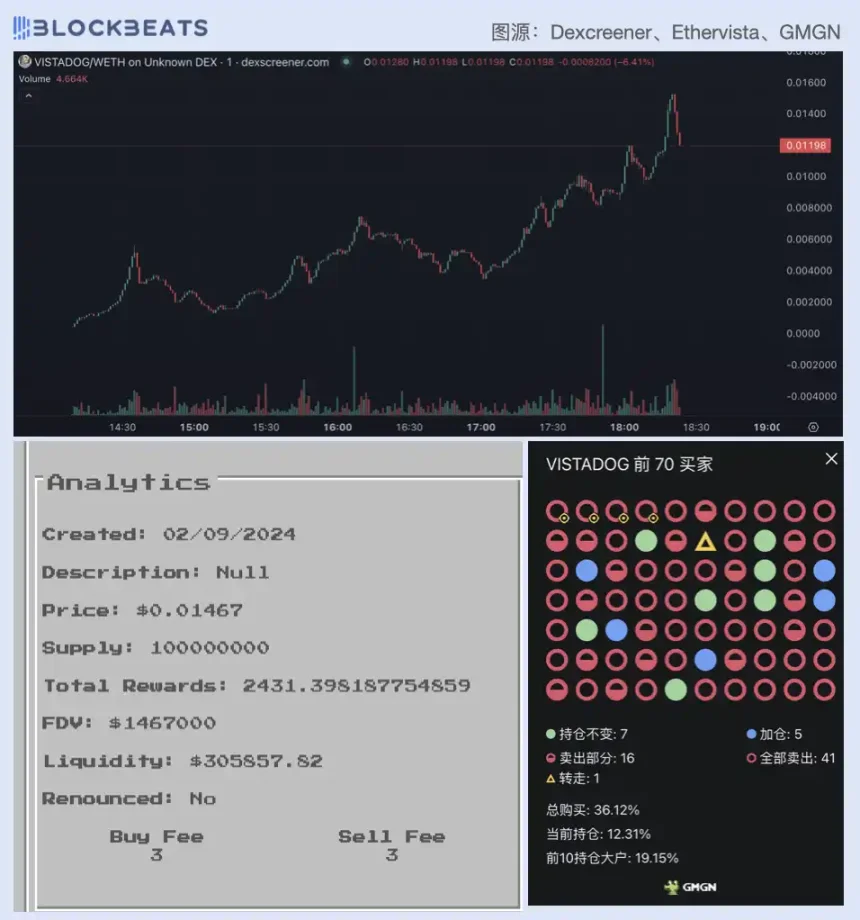

VISTADOG

VISTADOG 创建于 9 月 2 日下午 2 时左右,上线后 4 小时涨幅超 40 倍,交易量 150 万美元。截止撰稿时市值为 120 万美元。EtherVista 上显示,VISTADOG 目前共为其 LP 产生了 2,431 美元的奖励。GMGN 数据显示,VISTADOG 前 70 名买家共购买了 36% 的代币,目前持仓份额为 12%。

开发者日赚 3 万美元?

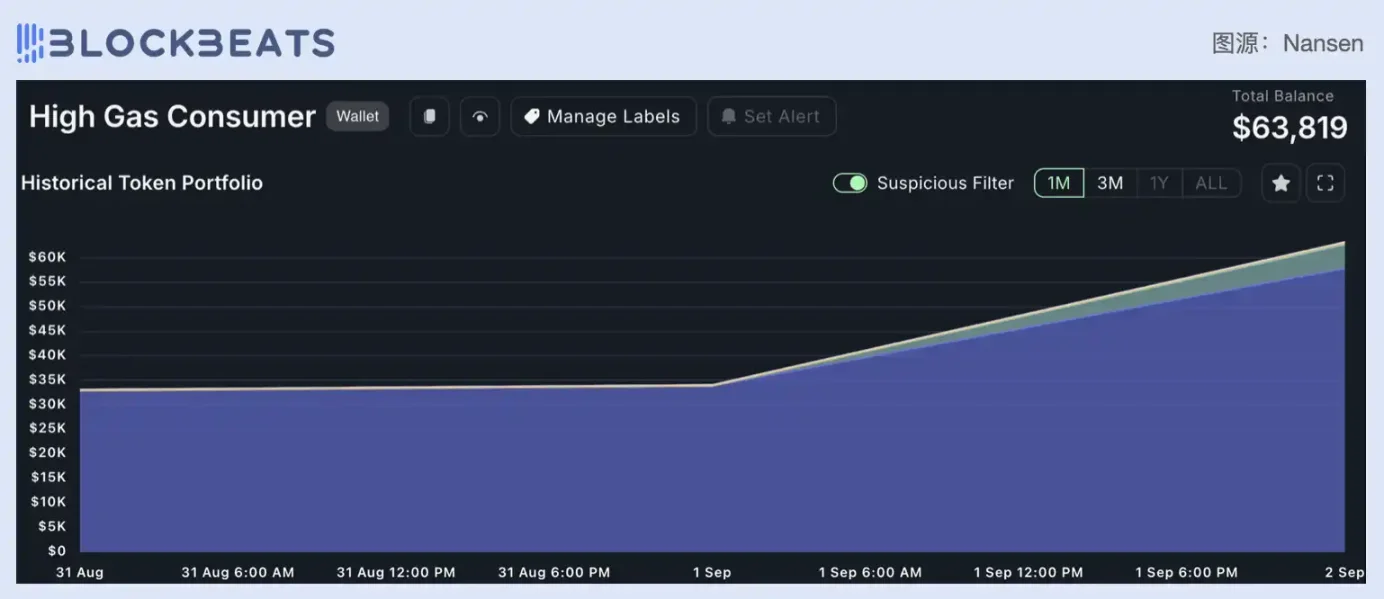

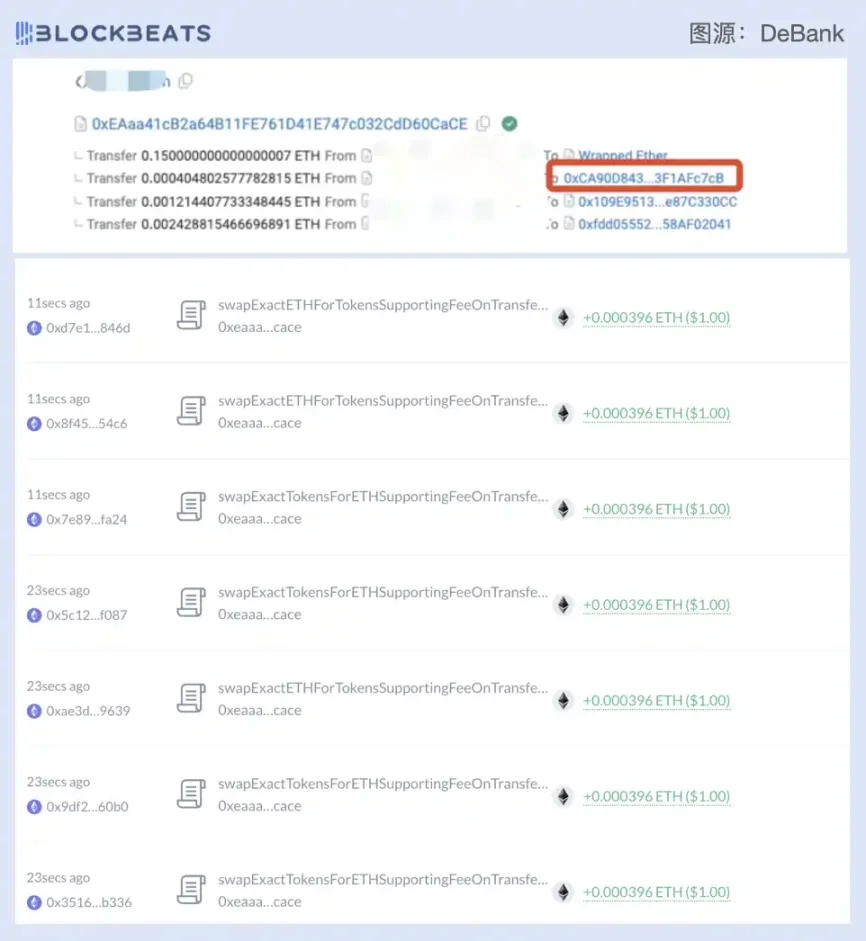

BlockBeats 在 EtherVista 上进行了一笔交易后,发现有一笔约 1 美元的 ETH 打入了 0xCA9 开头的地址,DeBank 数据显示,截至撰稿时,这个地址每秒都有数笔价值为 1 美元的 ETH 入账,疑似为 VISTA 开发者的地址。

在 Nansen 上,这个钱包地址被标记为「High Gas Consumer」,目前共有 63,819 美元,分别为价值 57,856 美元的 ETH、4,875 美元的 CLIPPY 和 281 美元的 VISTA。而其在昨日拥有 33,833 美元的 ETH,也就是说,EtherVista 开发者通过 VISTA 收获了的 24,023 美元的 ETH。