作者:Rancune

编译:深潮 TechFlow

这可能是我迄今为止最重要的帖子之一。许多人可能会错过"牛市"。你会吗?这里的许多人都非常线性地思考,只考虑熊市或牛市 - 一维的;价格要么上涨要么下跌。长期以来,这种观点让我感到不安(请回顾第一条回复中的展示a)。今天,我提出了一个新的概念模型,我相信这个模型:

a)为周期提供了一个全新的视角,

b)帮助我们更好地理解当前的情况,

c)是可操作的。

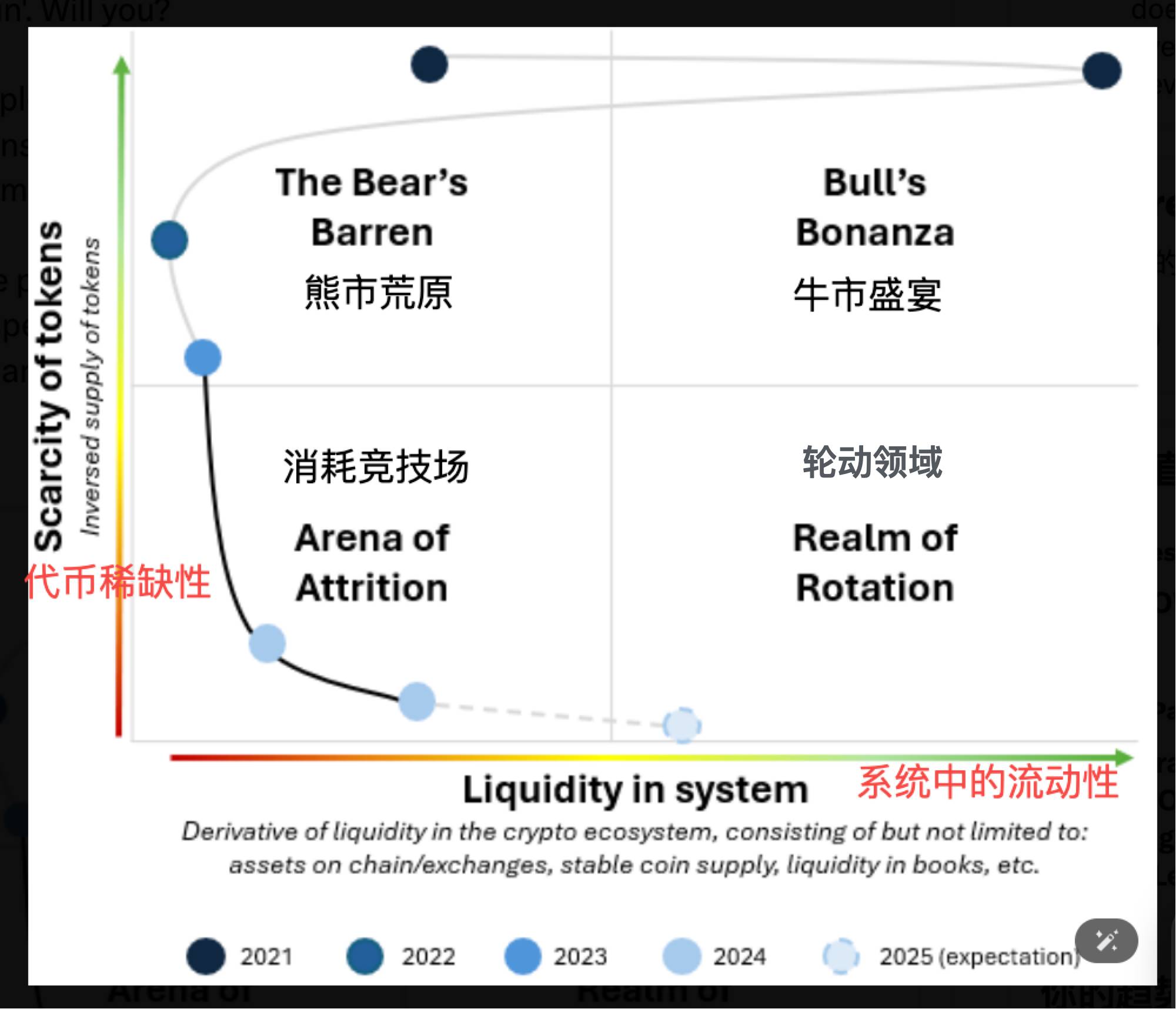

维度

系统中的流动性 | 加密货币比传统金融更难获取,在效率、入金、稳定币、中心化交易所可及性等方面都不够成熟。特别是现在,比特币和以太坊有传统金融的护栏,但这些护栏并没有向下传导,游戏规则已经改变。

代币的稀缺性 | 供应是加密货币的一个主要因素;它决定了可获得的流动性必须分散的分母。这与传统金融不同,在传统金融中,代币数量自然受限,通常需要IPO,而不是在Twitter Space上听到一个词就急于去Pumpfun。

根据我的理论,我们在2021年从低流动性和低供应飙升到高流动性和低供应("牛市盛宴")。之后,我们崩溃了,最终在2022年陷入"熊市荒原"。许多人称之为熊市,低供应和低流动性。熊市荒原和牛市盛宴的相似之处在于,由于供应量低,代币一致上涨(或下跌)。市场在移动,不一定是叙事在移动(尽管它们显然存在,但通常比我们当前的15分钟元叙事持续时间长得多)。

从FTX造成的损害和FTX的清算对生态系统的影响中缓慢恢复,流动性略微增加,但代币供应量增加更多。容易成为猎物的人退出了游戏,留下经验丰富(和恶意的)参与者,他们的提取基础设施已经建立并到位,可以提取更多。

从2023年开始,我们进入了"消耗竞技场",在这里我们无法从更高的流动性中受益,因为代币供应呈指数级增长。这真的是适者生存;最有技能的人(或与最好的人脉/最多内部信息的人)获胜。其他人则成为接盘侠。

我们经常将代币增长归因于Pumpfun和Solana垃圾币,这显然是真的,但不仅限于此。还包括无用的L1、L2、rollups、AI协议、桥等的数量之多。显然我们需要所有东西的分叉,我们绝对需要更多没有有机交易量、由风投资助的L2。这是我在展示b和c中写过的内容。

根据我的经验,每次我们在加密货币领域扩张时,接下来都会有一个收缩阶段。无论是在山寨币还是迷因币中,都会出现向优质资产的转移。

随着流动性的增加,我对未来6-18个月的预期是我们将进入轮动领域。我们将从增加的流动性中获得一些利益,但只限于特定的叙事和操作。大多数持有人将继续持有他们停滞不前或缓慢流血的代币,直到永远,在比特币往返6位数后回顾并思考:我是不是错过了?

我们不会再有2021年后每个人都联想到"牛市"的那种牛市盛宴了。这是不可能的,因为代币发行者的技能已经成熟(无论是你最喜欢的PF连环诈骗者还是试图从另一个元叙事中提取流动性的风投)。

但是,如何在轮动领域中操作呢?我将在下一篇文章中深入探讨这个问题。