背景

过去一年,仅以太坊链上数据统计NFT市值峰值为319亿美元,总成交额为575亿美元。2021年,传统艺术品拍卖成交额为657亿美元(仅拍卖统计),而未统计的链下艺术品成交额则在几千亿美元规模。未来,小到几十元的不知名艺术家的画作,大到国宝级收藏,可能都会有一个链上映射的NFT。

过去一年,大量知名影视明星和体育明星踏入NFT领域,比如bayc持有者库里、Justinbieber、麦当娜、小威廉姆斯、Parishilton、SnoopDogg等等;传统艺术家和文化公司也在陆续发布NFT,比如DC、阿迪达斯、哔哩哔哩、百事、余文乐、蔡国强、方立均、村上隆、周杰伦等。现目前NFT主要是FPF及数字艺术品为主的交易,但未来万物上链,万物均可NFT。

NFT高歌猛进的一年,NFT市场同时也存在许多问题:比如流动性差、波动率大、市场混乱、NFT热潮是否可持续?传统艺术品上链,元宇宙,数字艺术品的容量和前景有多大,这值得我们深度思考和探索。

NFT现状

金融市场有晴有阴,而NFT作为投资品也难独善其身。近期比特币和以太坊回调,NFT投资者投资情绪也在下降。

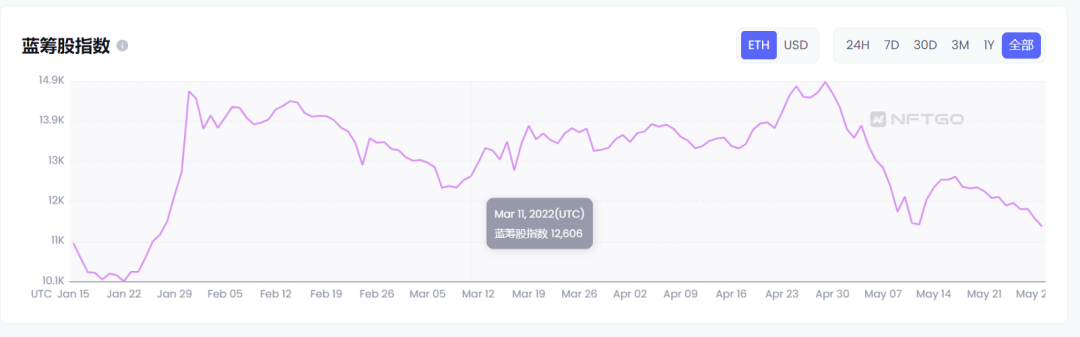

-NFT蓝筹更新换代快,总有新物追旧物。可能上半年是蓝筹,下半年就无人问津,逐渐失去流动性。

-NFT版块市值受大盘影响相对较弱,回撤幅度小于BTC(BTC价格:1/5-29/5,$39000-29000,回调39%;NFT总市值:1/5-29/5,355亿-257亿,回调28%)。

-另一个下跌原因与ETH计价有很大的关系,ETH跌,NFT价格也跌,在熊市中形成双跌。

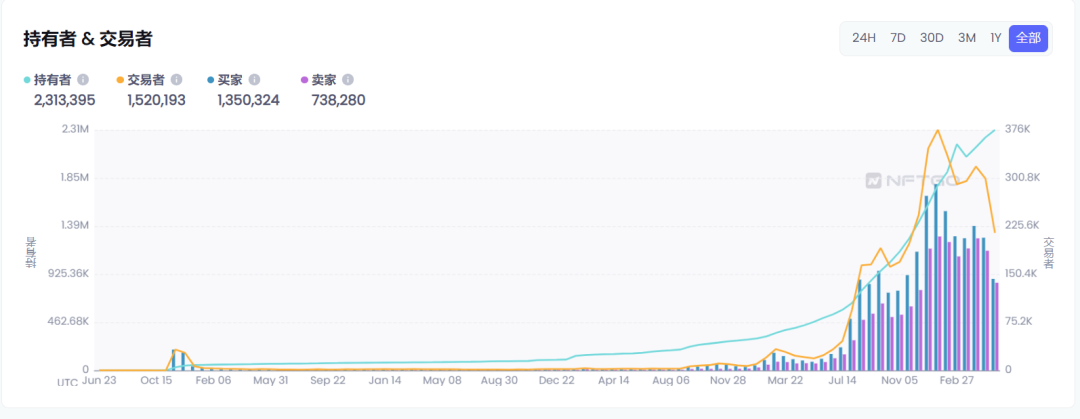

-近期NFT持有者在稳定上升,主要原因是最近2个月freemint开始流行。

-但交易者人数5月份随大盘也在同步下降。

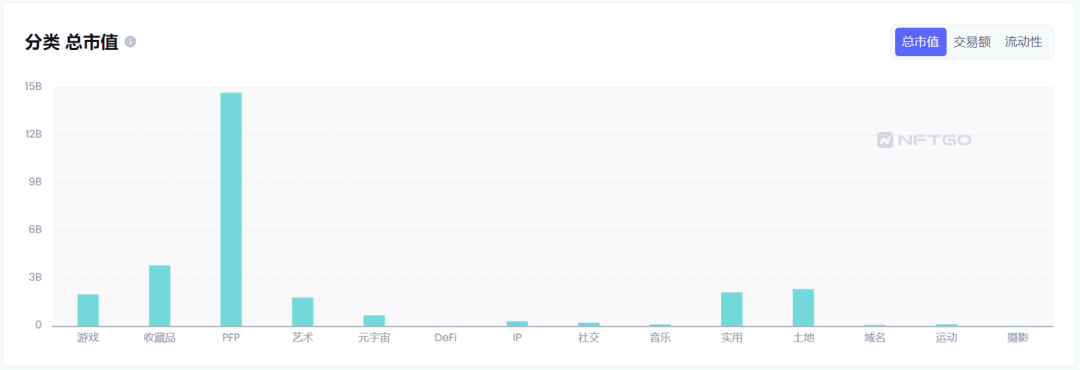

-目前的NFT市场品类主要是PFP、艺术品、PASS卡和虚拟土地为主。

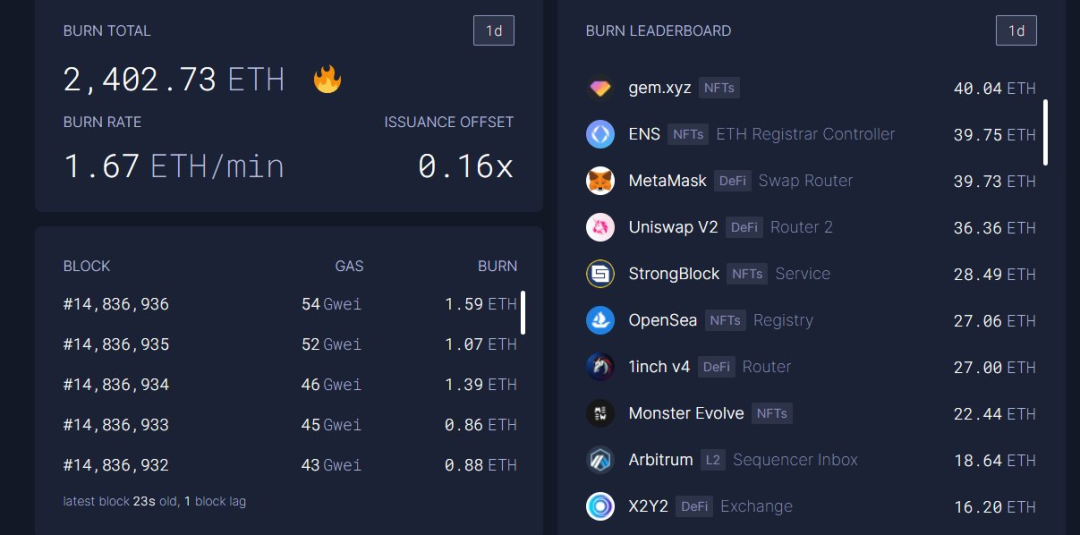

-从链上数据看,目前链上或者web3里最火热的场景就是NFT铸造和交易,opensea几乎成为了每日以太坊链上gas消耗最高的平台。

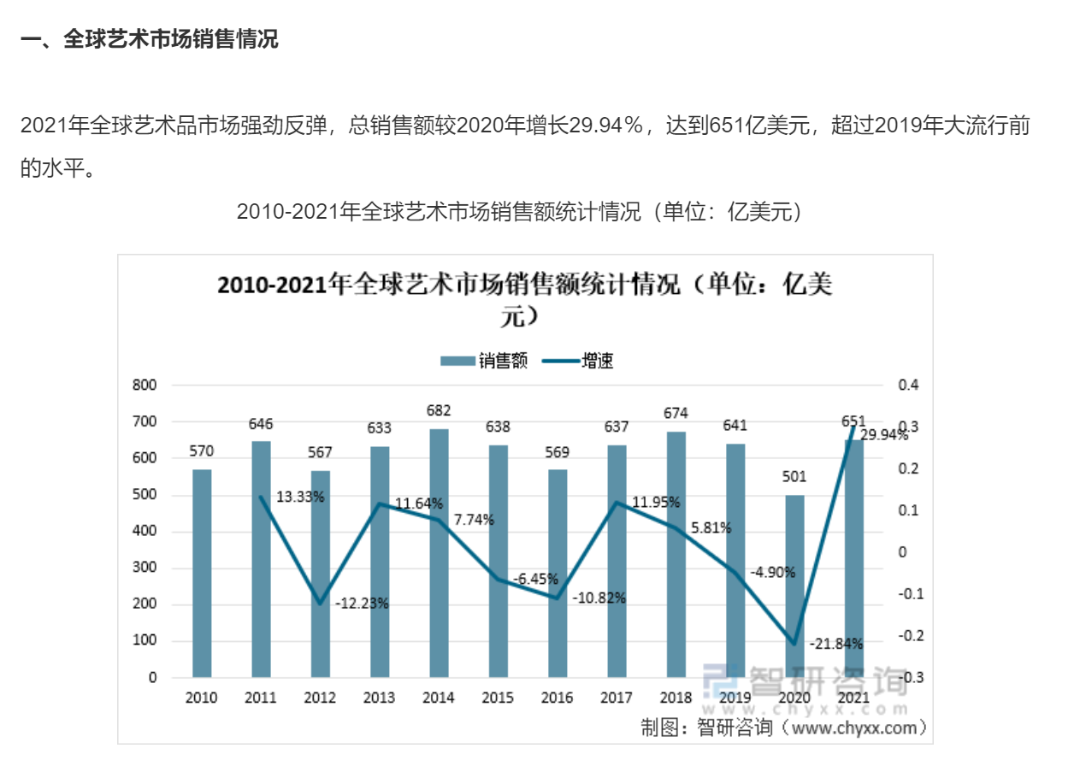

-据智研咨询发布的《2022-2028年中国艺术品拍卖服务行业发展现状调查及市场分析预测报告》显示,2021年全球艺术品市场强劲反弹,总销售额较2020年增长29.94%,达到651亿美元,超过2019年大流行前的水平。而这仅为拍卖口径统计,实际上全球未统计的艺术品、收藏品成交额可能在上千亿美元。NFT市场与之相比,仿佛一切才刚刚开始。

NFT平台现状

收费模式(平台):

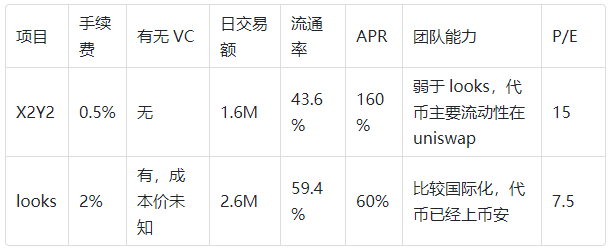

-opensea向卖家收取2.5%销售税,looksrare收取2%,X2Y2目前为0.5%;Foundation向发行方第一次收取15%,二次交易向用户收取5%。

收费模式(艺术家):

-主要是mint收费(或者可以freemint),在二级市场中每笔交易时收取版税(0-10%)。

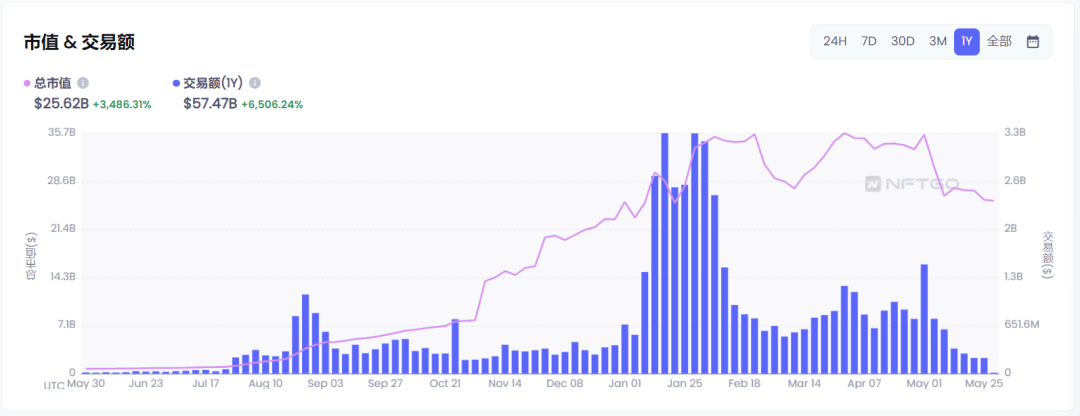

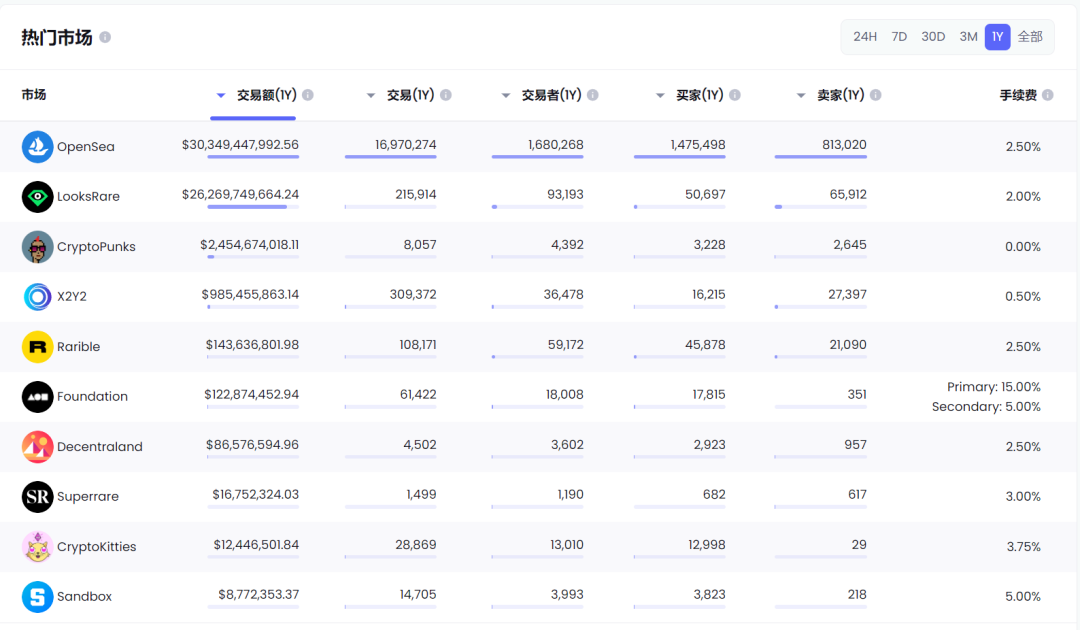

过去一年,opensea的总交易额为$30,349,447,992,按每笔2.5%的手续费,opensea的收入为7.75亿美元。由于opensea的中心化平台垄断,还是以web2的平台经济主导的收益分配模式,团队独享了赛道收益,平台用户得不到任何收益,这引来了很多WEB3用户的不满。因此,在过去的一段时间,出现了一些WEB3的NFT交易平台,他们正在以100%收入分配给社区的形式挑战opensea的行业垄断地位。

新晋NFT平台对比:LooksrareVSX2Y2

注:2022年1月,OpenSea宣布完成3亿美元的C轮融资,公司估值飙升到133亿美元,无论是Looksrare或者X2Y2,目前来看都是NFT赛道的低市值优质标的,下面我们将逐一分析他们的不同。

K线分析

X2Y2和Looks价格距离上市时均已经跌去超过90%,X2Y2相对于Looks横盘时间更久,底部支撑更加牢固。

团队:

Looksrare:据传闻是BSC链某头部DEX团队。

X2Y2:据传闻是国内某头部媒体团队。

团队在此不做评价,仁者见仁,智者见智。

代币经济模型:

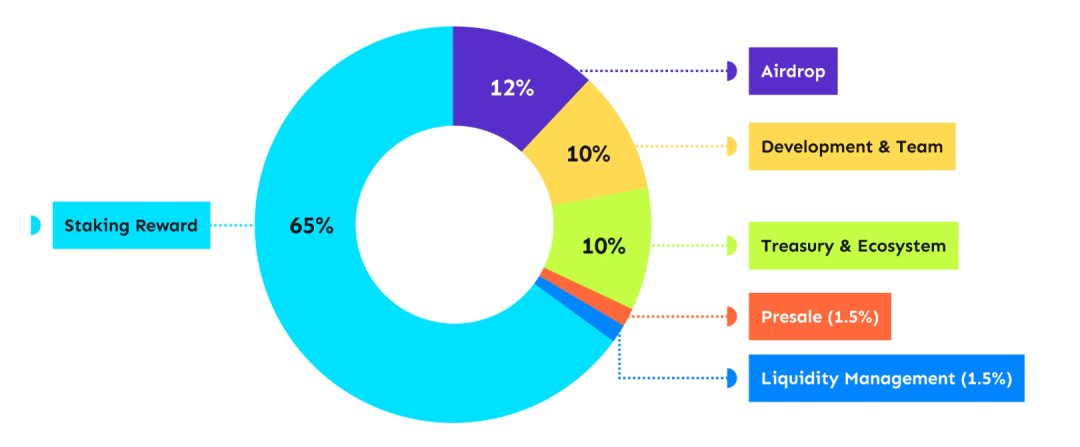

x2y2

总发行量10亿X2Y2,已经销毁9200万(空投未领取部分),现实际总量为9.08亿左右。

1、ILO公募出售15,000,000(1.5%)X2Y2代币,分1000份,每份1.5ETH,共募集1500ETH。(按彼时以太坊价格计算,公募成本约为$0.3,现已破发多日)

2、募集结束后,1500ETH+1%总量的X2Y2被添加进uniswapLP池并且被永久锁定。

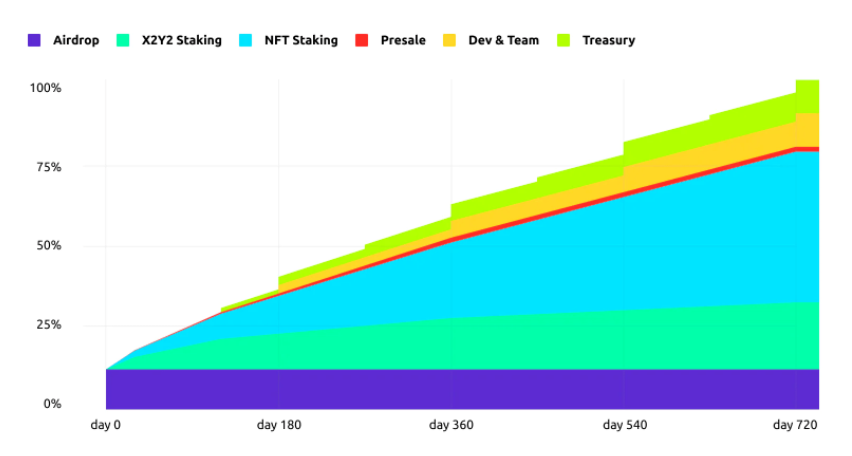

3、参加公募的X2Y2代币自2月14日起在360天内线性解锁。

4、团队代币锁定6个月后分12期释放,将在8月份释放第一期。团队在项目运行的半年无法通过出售代币获得任何收入,这点值得精神与勇气肯定。

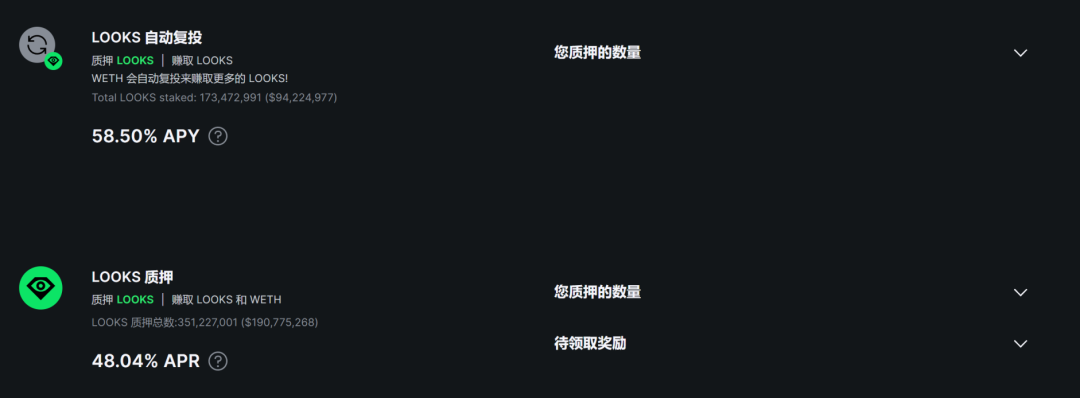

5、X2Y2质押奖励和交易奖励所产生的每日抛压约为120万个,按0.2现价预计每日抛压为24万美元。需要关注的是,其质押奖励将在6月18日从现在的每日60万个减少至97000个。

6、代币用途:质押X2Y2可分享100%平台手续费收入。

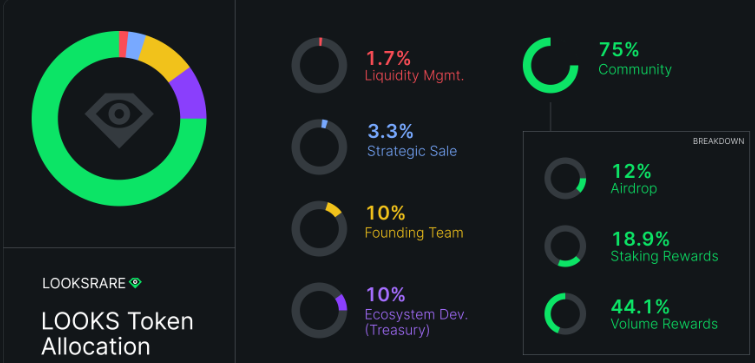

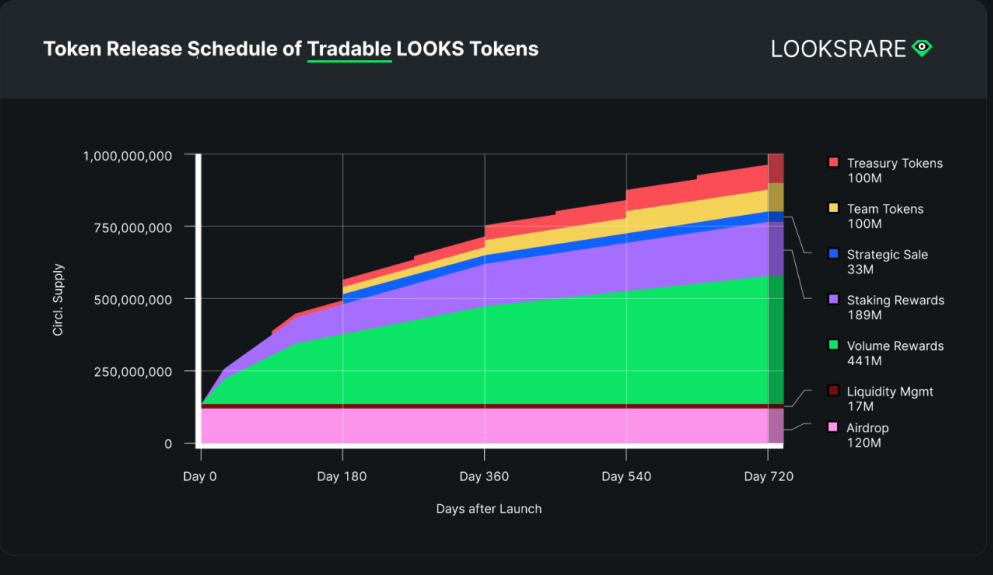

Looksrare

现目前,Looks每天的质押奖励为23万个,交易挖矿奖励为53万个,即每日抛压为76万个,按目前0.5的价格,每日抛压为38万美元。

代币用途:质押Looks可分享100%平台手续费收入。

交易额对比

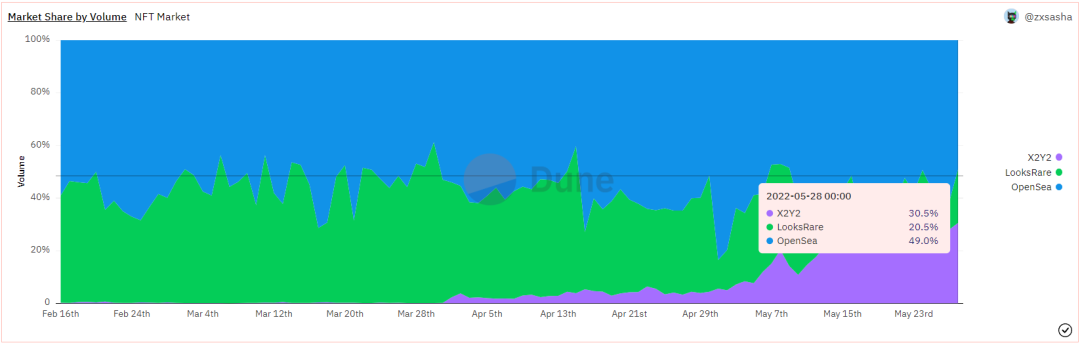

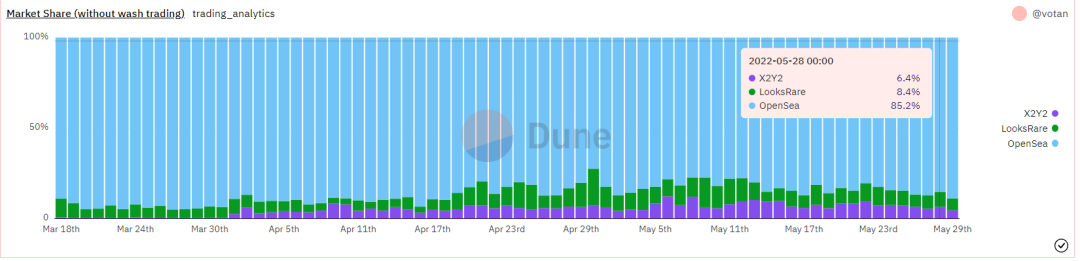

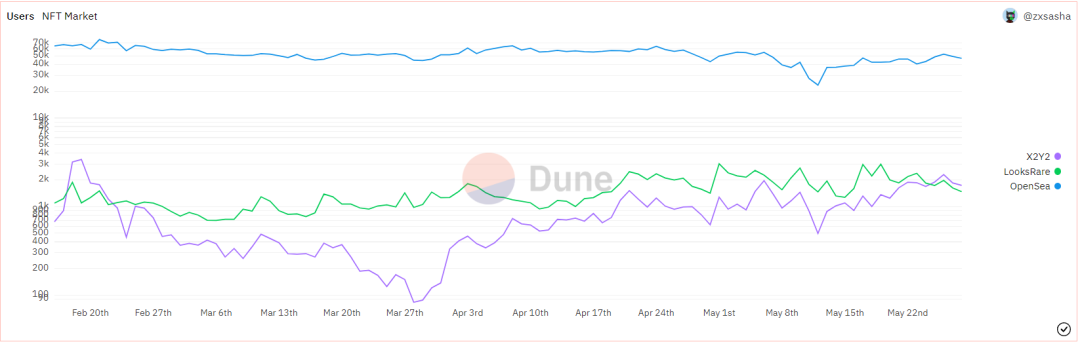

5月29日数据显示:opensea,Looksrare,X2Y2的NFT市场占有率(去除刷量)分别为85.2%、8.4%、6.4%;交易额为$32M,2.6M,1.6M。

用户数对比

受X2Y2的0.5%交易手续费吸引,近期在用户数量上,X2Y2开始超过Looksrare,并有望长期保持。

P/E市盈率对比(按无刷量估算)

(市盈率=每股价格(P)/每股收益(E)=公司市值/净利润)

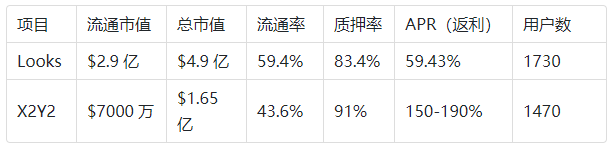

X2Y2:按平均每日交易额为3百万美元计算,交易手续费为1%,则每日手续费收入3万美元,年利润为1100万美元。X2Y2目前市值为1.65亿美元,则预计P/E=1.65亿/1100万=15

Looksrare:按平均每日交易额为450万美元计算,交易手续费为2%,则每日手续费收入18万美元,年利润为6570万美元。LOOKS目前市值为4.93亿美元,则预计P/E=4.93亿/6570万=7.5

质押分红APR对比

两者质押奖励都是阶梯性减产,由于X2Y2入市较晚,挖矿奖励启动较晚,现在交易挖矿奖励和质押奖励均高于Looksrare。X2Y2的质押奖励将在6月18日,日产出将从现在的每日60万个减少至97000个。

总结

1、X2Y2正在迎头赶上looksrare。用户数量上已经正式超越looksrare,真实交易量也和looksrare互不相让,但后期交易手续费提升且618质押奖励大幅减产后是否还能留住用户,稳得住市值,这是最大的问题。建议持续关注X2Y2真实交易量的可持续性,以及平台收入超过looksrare的转折点。如X2Y2的平台收入超过Looksrare,且市值依旧低于Looksrare,则适合买入X2Y2。

2、从目前来看,Looksrare没有和X2Y2打手续费价格战是很明智的决策,在坚持2%手续费的情况下,收入仍是X2Y2的几倍,市盈率相对X2Y2较低,且在很多头部交易所可以买到,交易流动性更好,相对更为稳健。

3、如果说Looksrare是NFT平台的蓝筹,那么X2Y2则是NFT平台中的潜力股,现在总市值仅为前者的1/3,后期更具爆发力。

图片

写在最后

1、为什么要写X2Y2和LOOKS:我们应该关注长期赛道,关注优质生息资产,关注最适合web3用户的利益分配方式。

2、如果你认可NFT赛道和未来的发展潜力,那么持有一些NFT平台代币是一个不错的选择,或许他们其中一个就是NFT版块的币安。

3、什么是优秀的代币经济模型?

-公平分发,没有私募轮,大家成本一样。

-团队份额占比少,且有长期锁仓,陪项目成长。

-代币有实际用途:持币者有锁仓动机,有项目收入用例(分红、回购、销毁、赋能代币),不通涨、有通缩等等,而不是单纯的治理代币,或者国库富得油流,代币常年不涨。