上周美国非农和以制造业指数为代表的疲弱经济数据引发市场对经济放缓的担忧仍在蔓延,全球资产遭受“黑色星期一”带来的抛压。美元对日元汇率一度跌破 142 ,回吐过去一年来的几乎所有涨幅。日本,韩国,土耳其股指触发熔断机制。美股三大指数均收跌在 3% 左右,“七巨头”开盘便蒸发 1.3 万亿美元的市值,期货市场完全定价美联储 9 月将降息 50 个基点,两年期美债收益率于盘中一度结束与 10 年期的倒挂,现报 3.957% 。

Source: TradingView

市场的抛售情绪也由传统市场蔓延到了数字货币。作为与 SP 500 高度相关的风险资产,BTC 于昨日一度暴跌至五万美元下方,引发了市场的恐慌情绪,短期 IV 冲上三位数区间,流动性出现挤兑,Vol Skew 也随着价格一同下跌,Wing 上的需求暴增导致 Fly 的估值快速上扬。

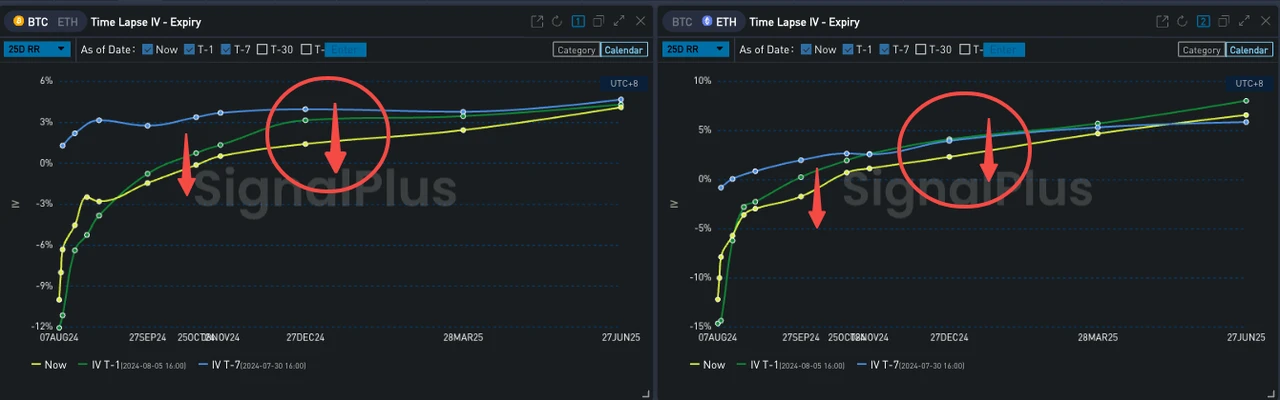

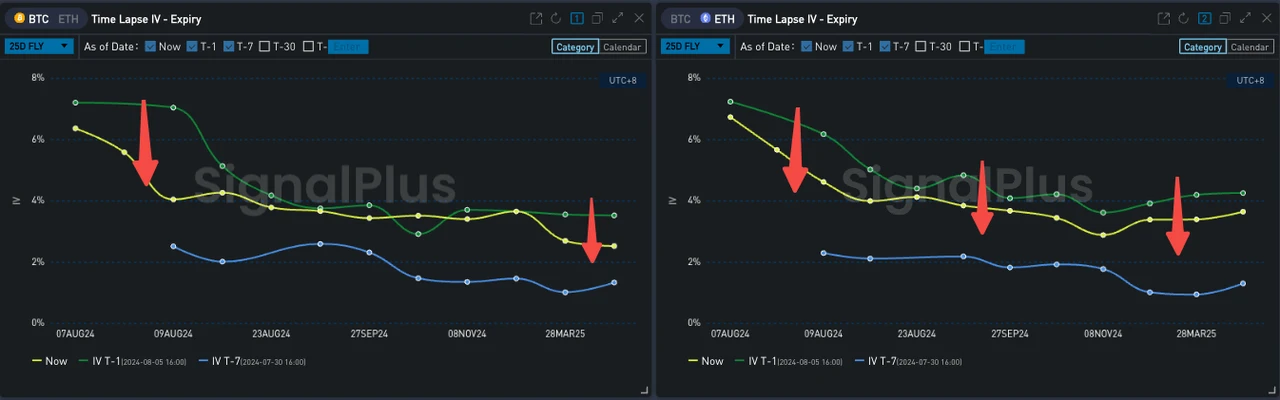

但随着价格逐步反弹回到 55000 美元,期权市场的流动性逐步回归,IV 下行逃离了局部高点,尾部高昂 Vol Premium 也被重新定价,Fly 整体走低。对 Vol Skew 来说,尽管前端的负斜率轻微反弹,但更需要关注的变化是远端 Vol Skew 的进一步大幅下跌,事实上,昨日价格暴跌的时候只有前端做出了反应,流动性较差的远端 Risky 直到今天才被重新矫正了定价。

Source: Deribit (截至 6 AUG 16: 00 UTC+ 8)

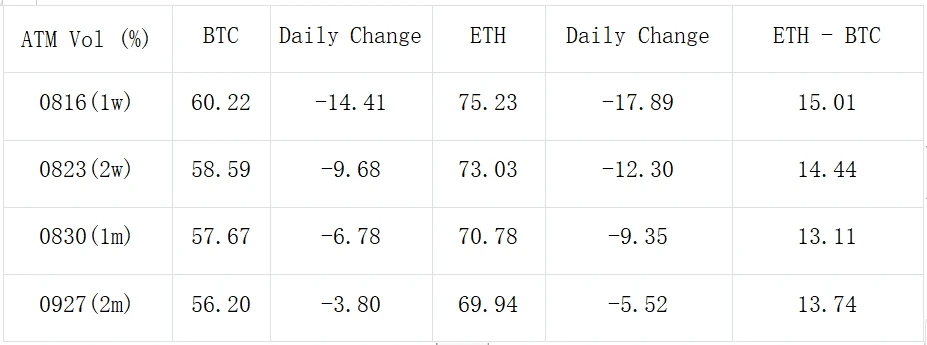

Source: SignalPlus,ATM Vol

Source: SignalPlus, 25 dRR,远端 Vol Skew 被重新定价

Source: SignalPlus, 25 dFly

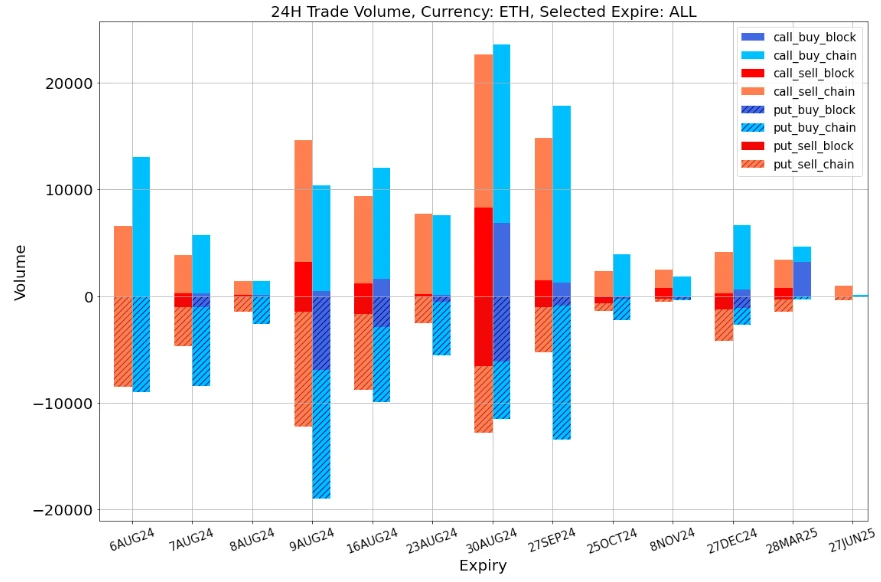

Data Source: Deribit, ETH 交易总体分布

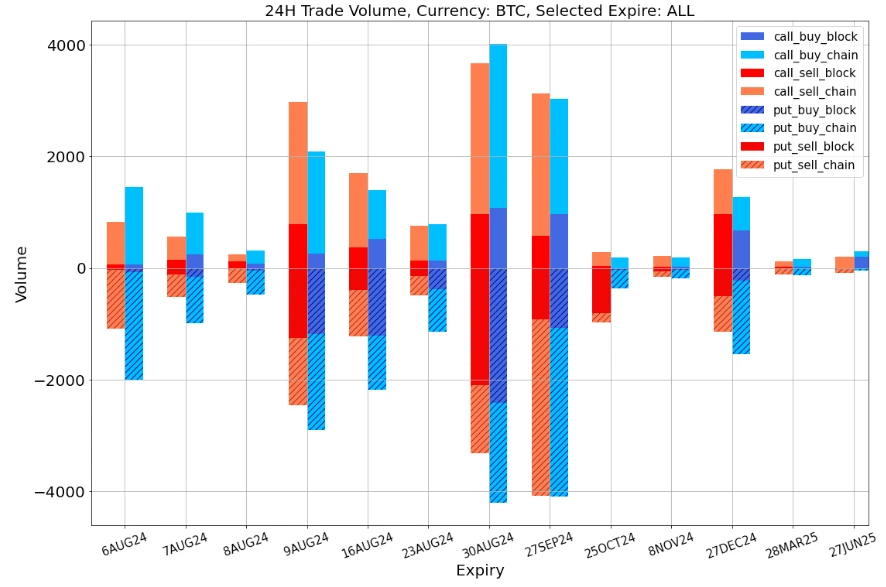

Data Source: Deribit,BTC 交易总体分布

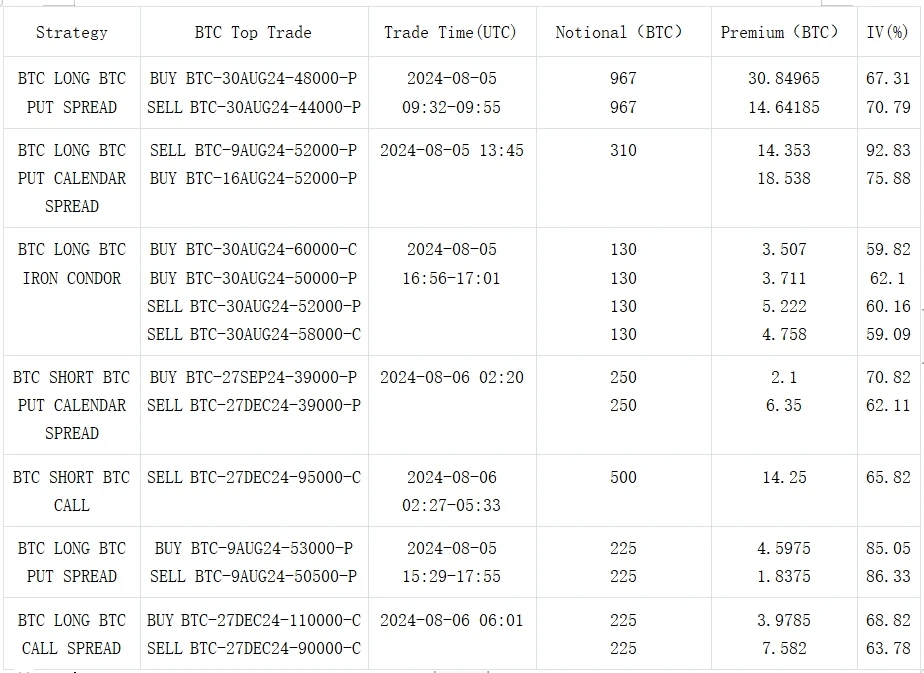

Source: Deribit Block Trade

Source: Deribit Block Trade

您可在 t.signalplus.com 使用 SignalPlus 交易风向标功能,获取更多实时加密资讯。如果想即时收到我们的更新,欢迎关注我们的推特账号@SignalPlusCN,或者加入我们的微信群(添加小助手微信:SignalPlus 123)、Telegram 群以及 Discord 社群,和更多朋友一起交流互动。SignalPlus Official Website:https://www.signalplus.com