撰文:Glassnode

翻译:白话区块链

我们很高兴发布我们季度系列的第三版《加密市场指南》,这是与 Coinbase Institutional 合作制作的。这份报告对每个季度加密市场的关键发展进行了深入分析,包括价格表现、链上分析、行业事件和衍生品数据。

与之前的版本一样,我们的目标是通过基于链上数据的可操作洞察,为机构交易者和投资者提供对数字资产市场的更好理解。本版侧重于三个主要洞察:链上活动的迅速增加、ETF 的变革性影响以及对当前市场周期的分析。

关键亮点:

市场周期的评估:加密市场以其独特的涨跌周期著称。最新数据显示,尽管第二季度有所回落,我们可能处于自 2022 年底开始的当前牛市周期的中期。历史模式表明,这种调整是典型的,与以往的市场行为一致。

ETF 改变了格局:现货比特币 ETF 在六个月内积累了近 500 亿美元的资产管理规模(AUM),吸引了新投资者并加深了市场流动性。ETF 引入了一种受监管且熟悉的投资工具,补充了现有的选择,对整个加密生态系统产生了积极影响。

链上活动快速增加:在过去六个月中,各种指标如总锁仓价值(TVL)、活跃地址和用户基础规模显示出链上活动的显著增长。这种激增由各种用例推动,包括借代、质押和交易。随着现有用例的成熟和新创新的出现,预计链上采用将进一步增长。

1、第三季度的关键趋势

以下是过去一个季度中值得从投资者角度关注的一些趋势:

1)投资者盈利趋势与 MVRV

MVRV 动量是一个有助于分析师监测市场趋势的工具。它通过追踪投资者持有的未实现利润倍数(MVRV)相对于其 365 天移动平均线的变化来进行分析。

当 MVRV 交易高于其 365 天均值时,通常表明强劲的上升趋势和投资者盈利能力改善,往往导致在市场调整期间增加头寸。相反,当 MVRV 跌破 365 天均值时,往往预示着显著的未实现损失,增加了不确定性和避险决策。

在七月初,MVRV 比率在其 365 天移动平均线附近找到支撑,表明 2024 年的上升趋势仍然保持完整,并带来积极的投资者盈利能力。

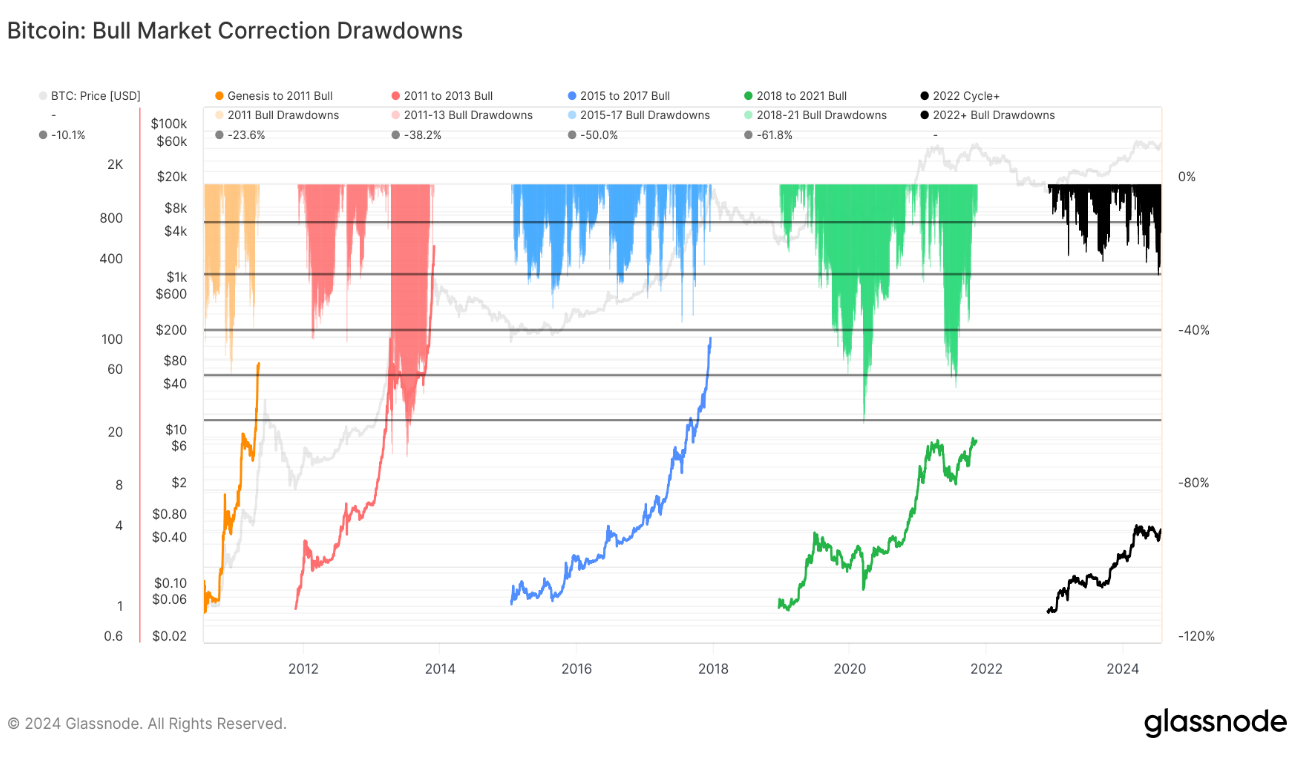

2、BTC 周期表现和回撤

自 2022 年末开始的当前牛市中,比特币价格上涨了 400%。在 FTX 崩盘之后,比特币经历了持续 18 个月的稳定价格上涨,达到了 73000 美元的历史最高价。随后,市场进入了一个持续三个月的区间震荡阶段,随后出现了 -26% 的回撤。

这次下跌趋势较之前的周期更为平缓,表明市场结构强劲,波动性降低。2023-24 周期与 2018-21 和 2015-17 周期相似,为周期结构和持续时间提供了宝贵的见解。

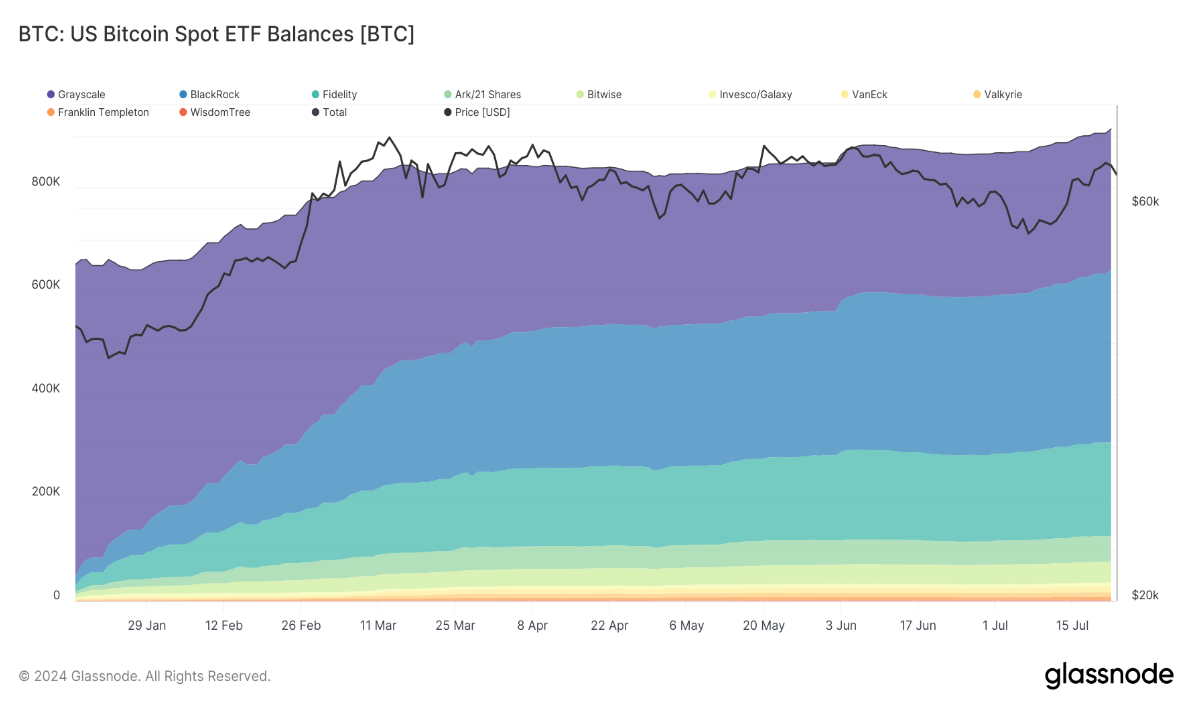

1)比特币现货 ETF 余额

跟踪美国前十大交易的比特币 ETF 的余额可以了解资金流入这些产品的情况。现货比特币 ETF 取得了空前的成功,资产管理规模超过 500 亿美元,使其成为历史上最成功的 ETF 发行。

自它们推出以来,ETF 的资金流入也显著超过了比特币的新发行量,创造了巨大的需求。这种增加的需求推动了现货和衍生品市场的交易量上升。

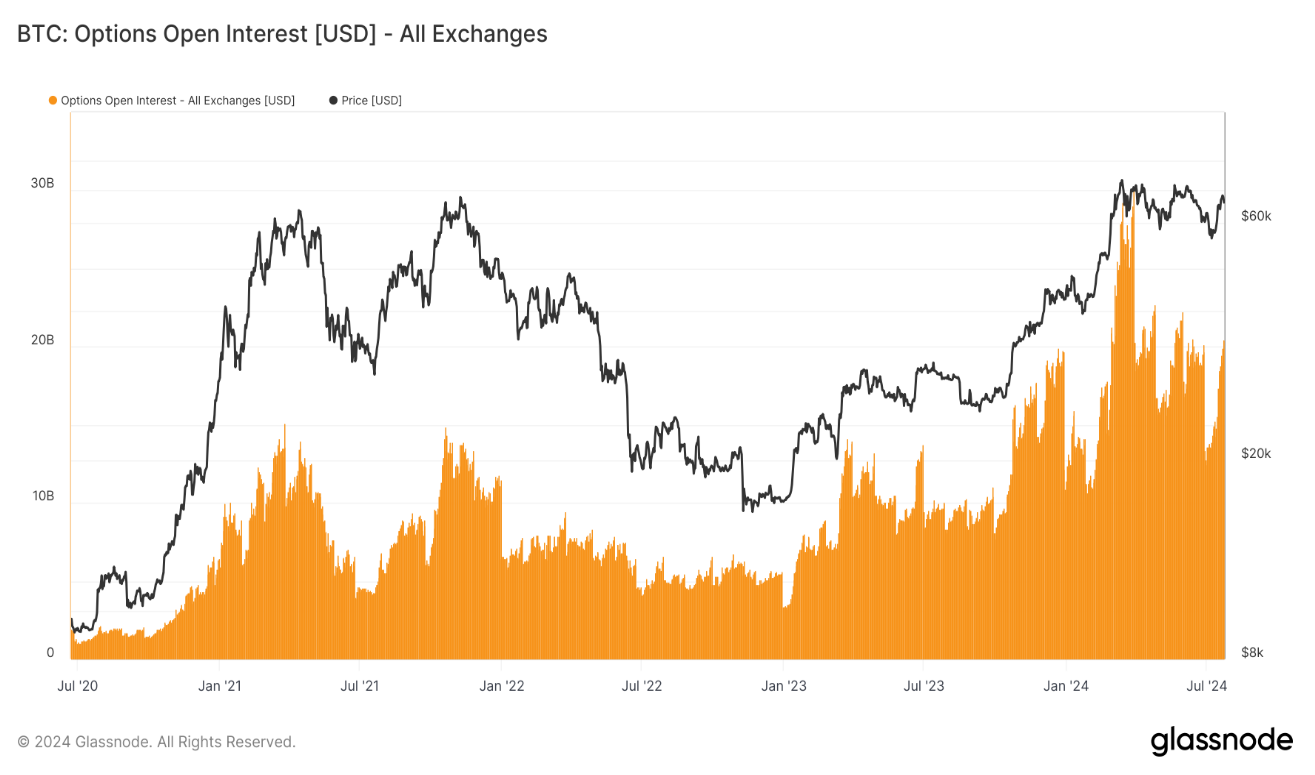

2)比特币期货交易量和持仓量

比特币期货的交易量和持仓量大幅上升。传统期货和永续期货都显示出参与度和流动性的增加,反映了对比特币衍生品日益增长的兴趣。

要深入探讨这些和其他主题,增强您的数字资产投资策略,请查看 2024 年第三季度《加密市场指南》的完整版本。

在此下载完整报告。