· At the beginning of 2026, the cryptocurrency market regained its upward momentum. Despite heightened geopolitical uncertainty, Bitcoin's price rose to $94,000, and the total market capitalization of cryptocurrencies approached $3.3 trillion.

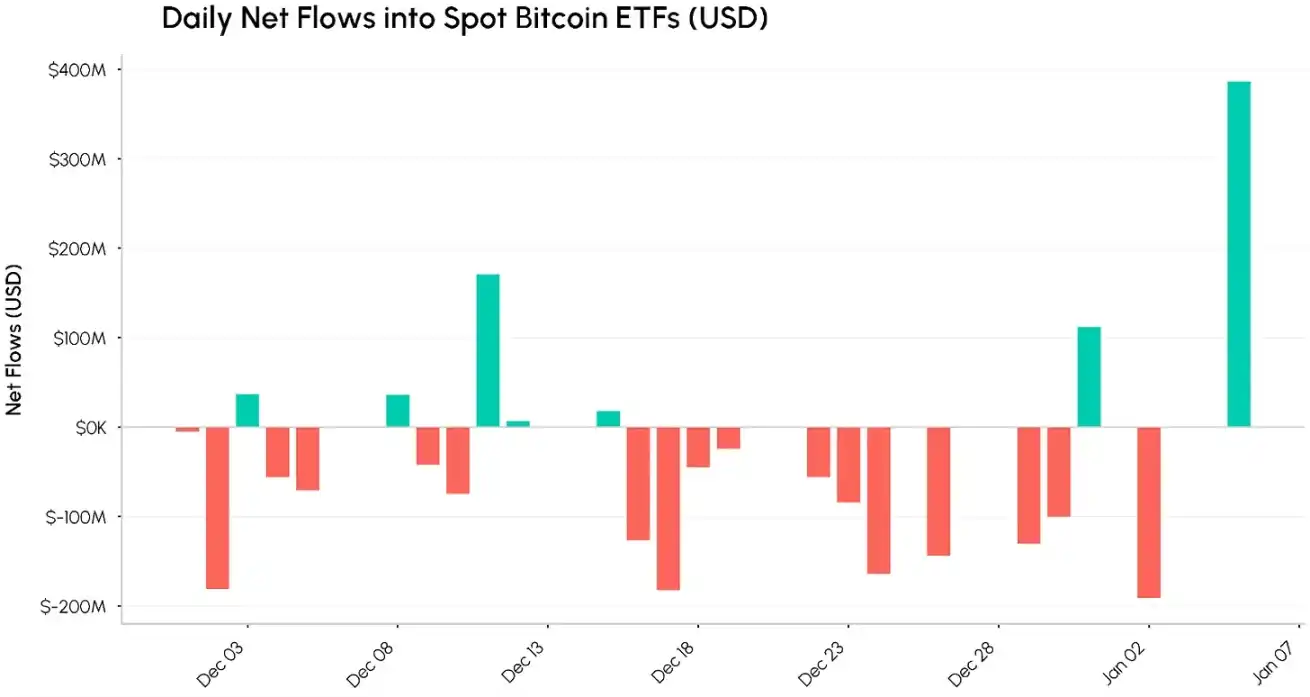

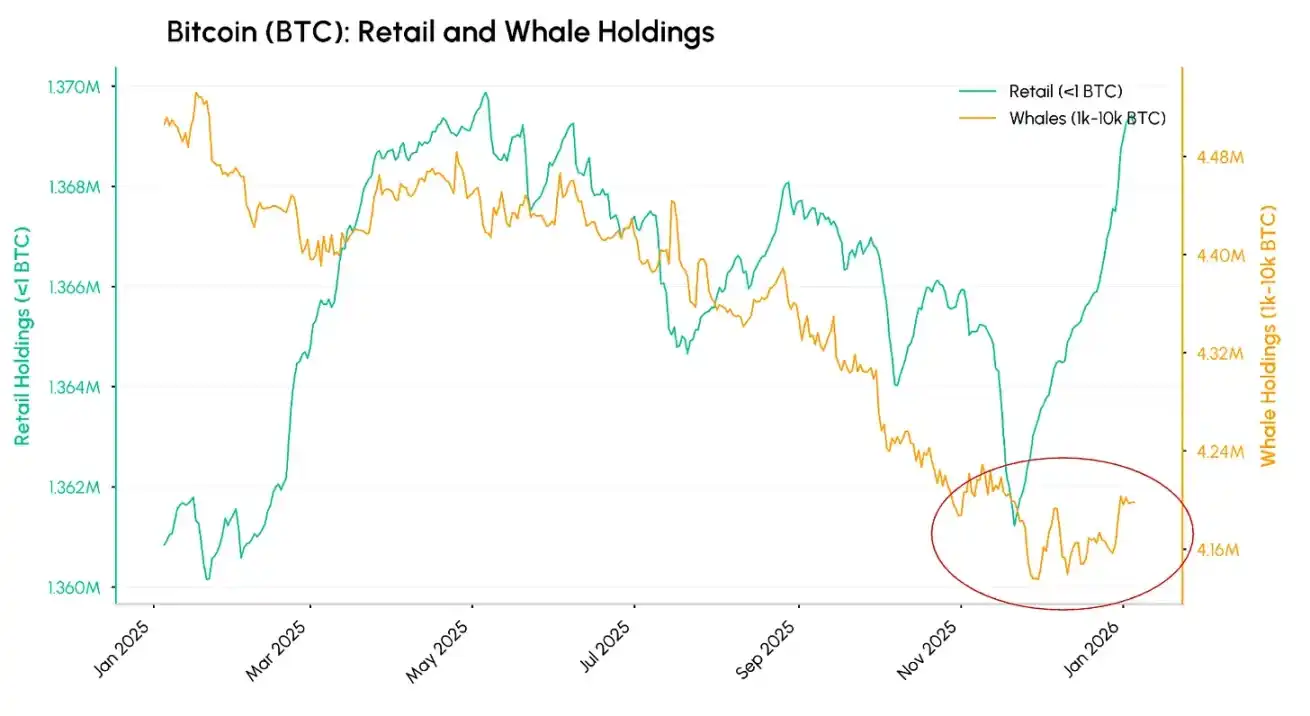

· Spot Bitcoin ETFs reversed the year-end outflow trend on January 5, with a net inflow of approximately $400 million; whale selling activity moderated, while retail investors actively accumulated positions.

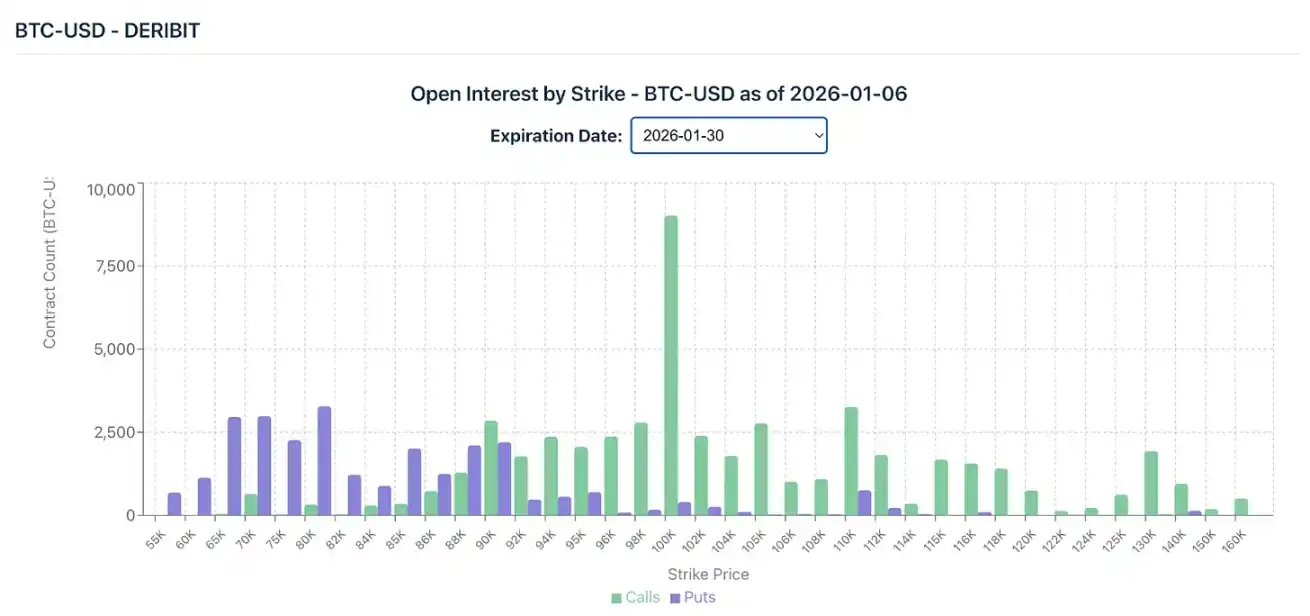

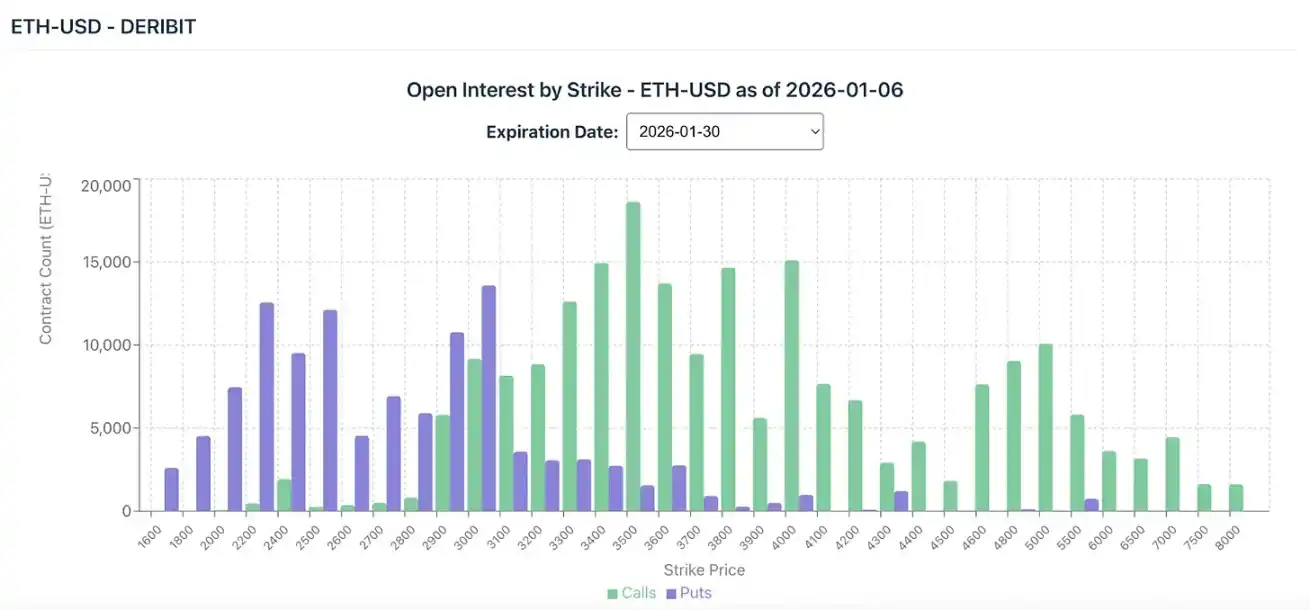

· Derivative market positions indicate a cautiously bullish stance. Among the options contracts expiring at the end of January, Bitcoin call open interest is concentrated at the $100,000 strike price, while Ethereum call open interest is concentrated at the $3,500 strike price.

A Green Start to 2026

After several weeks of range-bound trading during the holiday season, the cryptocurrency market started the new year on a strong note. Bitcoin's price surged to $94,000, and the total market capitalization of cryptocurrencies approached $3.3 trillion.

Despite the escalation of geopolitical tensions due to U.S. military action against Venezuela, the cryptocurrency market remained resilient. As year-end prices for precious metals like gold and silver soared, crypto assets gradually recouped their losses. Additionally, the strength of some altcoins signaled a rise in market risk appetite. However, influenced by the evolution of the geopolitical situation, global markets may still experience significant volatility in the short term.

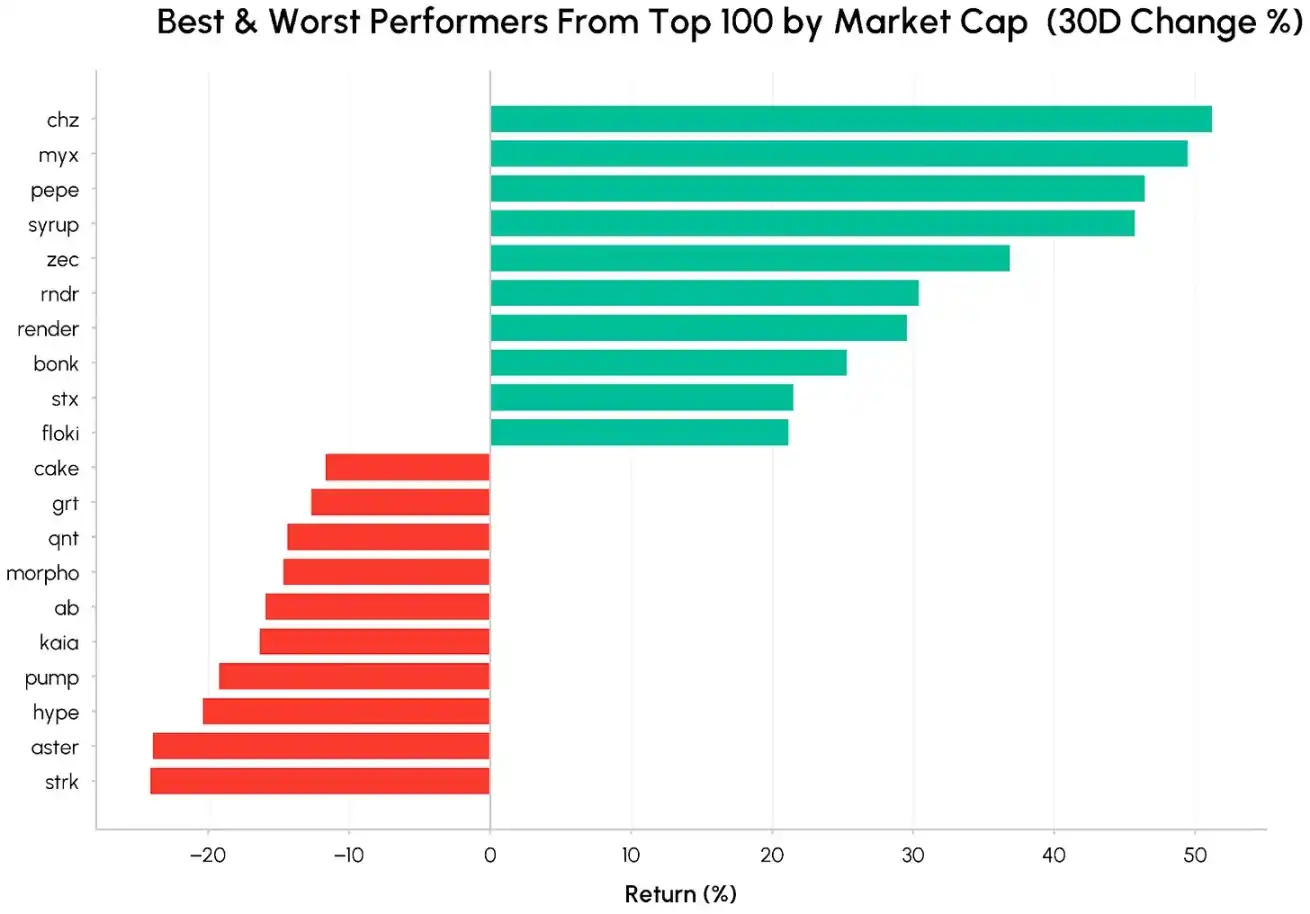

Over the past month, standout performers included Memecoins like PEPE and BONK, privacy-focused Zcash (ZEC), and the institutional credit platform Maple Finance (SYRUP). This trend indicates a resurgence of interest in Memecoins, privacy tokens, and DeFi tokens with clear profit-sharing mechanisms and visible cash flow growth.

In contrast, Hyperliquid (HYPE) and Aster (ASTER) underperformed. The reason lies in the diversion of market attention within the decentralized perpetual contract trading platform sector following the token airdrop by Lighter (LIT), a platform based on zero-knowledge Rollup technology. The decentralized lending protocol Aave (AAVE) also declined during this period due to intense community debate and multiple governance votes regarding token holder rights, profit distribution models, and the role of Aave Labs in the decentralized autonomous organization. This controversy reflects a broader trend across the DeFi industry: leading protocols like Uniswap and Aave are re-evaluating how value flows back to token holders.

Institutional Funds Return, Whale Selling Cools

Spot Bitcoin ETFs reversed the year-end outflow trend, with a single-day net inflow of over $350 million on January 5, marking the return of institutional funds to the crypto market. Around the New Year, spot Bitcoin ETFs had recorded net outflows exceeding $320 million. This reversal suggests a resurgence of institutional investor allocation interest as the first quarter of 2026 begins.

Institutional crypto asset reserves continue to expand: the U.S. Strategic Bitcoin Reserve added 1,287 Bitcoin, bringing its total holdings to 673,783; Bitmine increased its Ethereum reserves to 4.14 million, accounting for approximately 3.4% of Ethereum's total supply.

On-chain data shows that since the beginning of January, token selling by whale addresses holding 1,000-10,000 Bitcoin has significantly moderated, indicating reduced selling pressure from this group. Meanwhile, retail investors holding less than 1 Bitcoin have been accelerating their accumulation since mid-November last year. As cryptocurrency prices retreated from highs and consolidated, retail investors bought the dip. The combination of reduced whale selling and sustained retail buying creates a favorable market structure.

Derivatives Market Signals Cautious Optimism

Derivatives market positions indicate a cautiously optimistic view of the Q1 2026 trajectory. The two charts below show the open interest by strike price for Bitcoin and Ethereum options contracts expiring on January 30, 2026, on the Deribit platform, visually reflecting option traders' bets on short-term market direction.

Options market data shows that for contracts expiring on January 30, Bitcoin call open interest is heavily concentrated around the $100,000 strike price, while Ethereum call open interest is concentrated around the $3,500 strike price. This indicates traders are betting on short-term upside potential but are not exhibiting excessive euphoria. Downside protection is also in effect: Bitcoin put open interest is notable in the $70,000 to $90,000 range, though the overall open interest structure remains skewed towards the long side.

The futures market conveys a similar signal. Year-end, Bitcoin and Ethereum futures open interest saw a slight pullback but quickly rebounded in January, with the nominal open interest on major exchanges nearing the highs of last December. In late December, influenced by broad market deleveraging, the funding rates for Bitcoin and Ethereum perpetual contracts briefly turned negative. However, they have since recovered to positive territory, with Ethereum's funding rate significantly stronger than Bitcoin's. Overall, the market is in a cautiously bullish state, not yet showing signs of being overextended.

Stablecoin Flows and On-Chain Activity

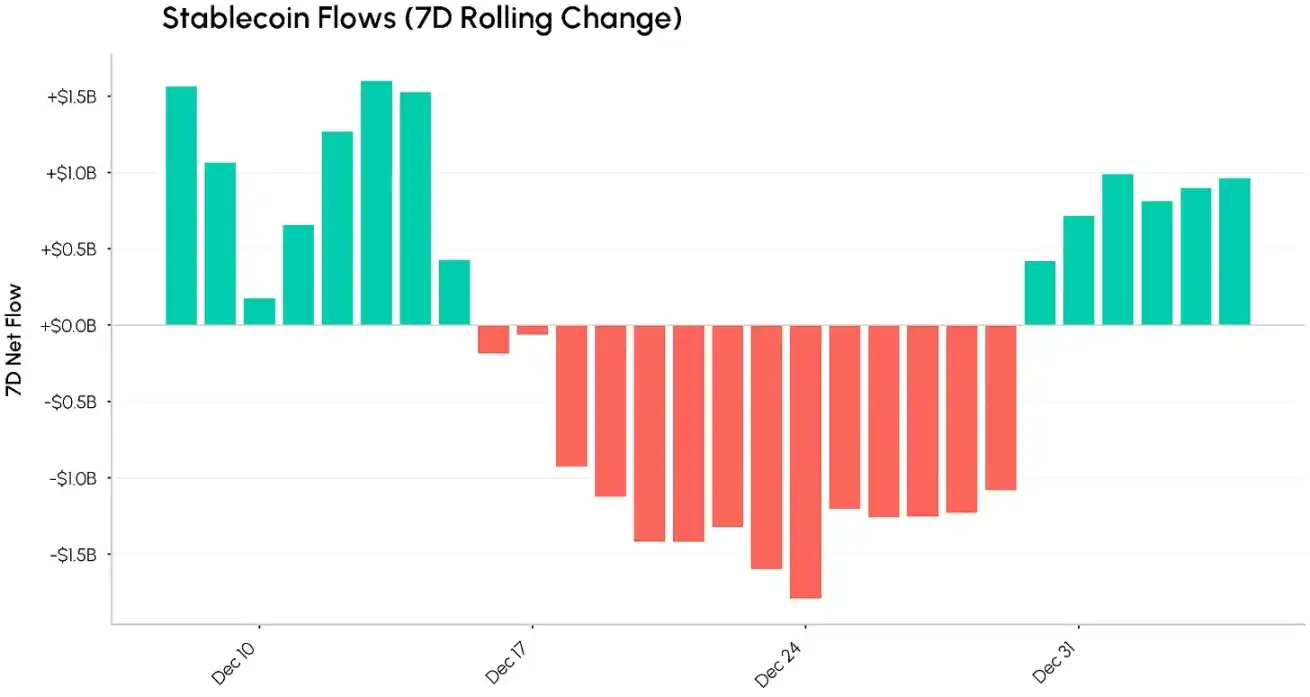

Stablecoin flow is a key indicator for observing capital movements into and out of the crypto market. In early December last year, the stablecoin market recorded sustained net inflows, but towards year-end, flows turned negative, with a single-week net outflow exceeding $1 billion. Entering January 2026, stablecoin flows stabilized and turned net positive again. If this trend continues, it will provide strong support for the sustained rise of the crypto market.

On-chain activity data further corroborates the positive market outlook. Following the implementation of the Ethereum Fusaka upgrade in December, Ethereum mainnet daily transaction volume hit a record high of 2.23 million, and the number of active addresses approached all-time peaks. Concurrently, stablecoin on-chain transfer volume also set a new record in December, indicating that capital flowing into the crypto market is not sitting idle but is actively circulating within the ecosystem.

Conclusion

Market data from the first week of 2026 paints a picture of cautious optimism, with the cryptocurrency market gradually finding its footing. The return of institutional funds, cooling whale selling, optimistic signals from the derivatives market, coupled with high on-chain activity and the return of net inflows into stablecoins, collectively support the market's upward movement. However, it is crucial to remain vigilant, as the geopolitical developments between the U.S. and Venezuela remain a potential risk factor that could trigger global market volatility in the short term.