原文作者:AlΞx Wacy

原文编译:深潮 TechFlow

将 1, 000 美元变成 100, 000 美元并不需要无休止的交易。

低市值山寨可能在未来几个月内成为市场巨大的机会,下面我分享了 8 个具有 100 倍潜力的山寨币。

每天都有潜在的未来巨头进入市场。其中一些会立即快速增长,而另一些则可能需要一些时间才能蓬勃发展。未来可能还会有更多类似的项目。

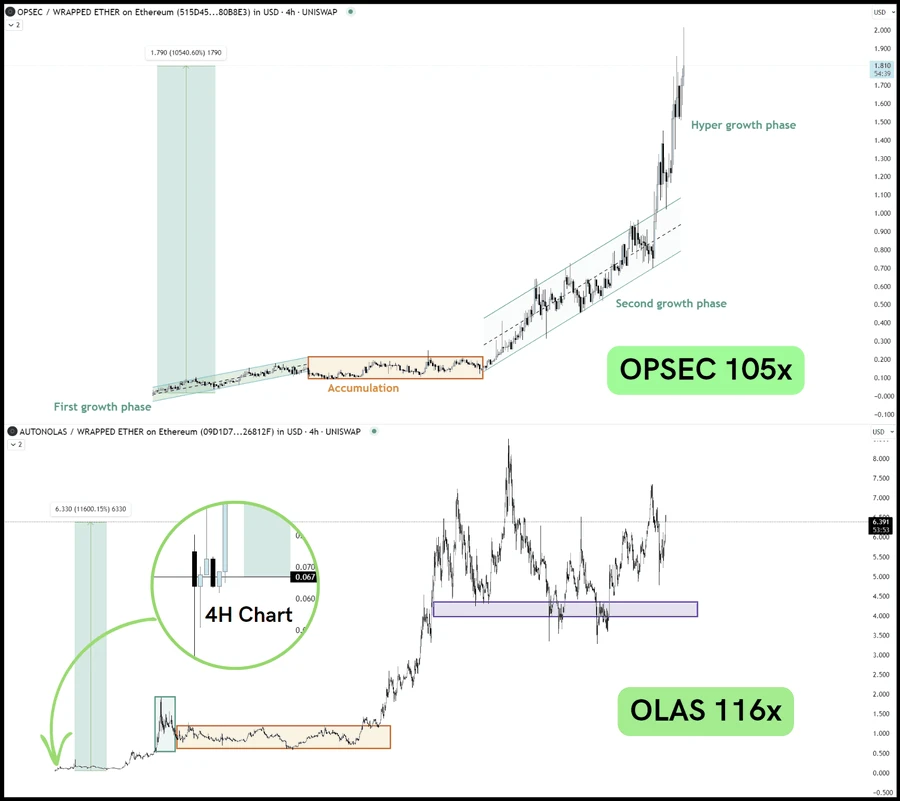

我经常强调:您不必成为第一个买家就能获得可观的利润。只需探索并相信该项目,在启动后进行投资,然后等待即可。

以 105 倍 的 $OPSEC 或 116 倍 的 $OLAS 作为此策略的主要示例。您甚至不需要使用机器人或其他工具来提前购买。这个案例清楚地表明,即使您买入得晚一些, 30-50 倍回报的潜力仍然很高。

让我们讨论一下最近推出的项目,这些项目有潜力在未来 2-6 个月内成为行业巨头。

在考虑此类投资时,进行深入的项目分析并保持耐心至关重要。否则,您最终可能会在代币短暂下跌时出售您的代币。

这些项目目前处于低调状态,市场对其缺乏足够的关注,这为我们提供了利用其预期增长的机会。

Shutter($Shu)

Shutter 是一个开源项目,其使命是通过基于阈值密码学的分布式密钥生成(DKG)协议来防止以太坊上的抢跑交易(Front Running)。

经过 3 年多的开发,开创了 Anti MEV 解决方案

由核心以太坊开发人员组成

与 EigenLayer 团队建立联系,与 $OLAS、 @Optimism、Gnosis Chain 和 Valory 合作 。

我对这个项目充满信心;它是未来的蓝筹股。我坚信,即使是 5 亿美元的市值也是不够的。

$SHU 目前价格 0.33 美元,市值 1500 万美元。

价格正在脱离积累区。考虑到其潜力,以 1000 万至 5000 万美元的价格购买性价比都很高。

更多代币将于 3 月 18 日解锁。如果再次下跌,我计划购买更多。

Uniswap 上可以购买。

Monai($MONAI)

Monai 正在开发一套未经审查的生成式 AI 工具,将与 @monad_xyz 无缝集成。

他们的旗舰产品是先进且不受限制的大型语言模型 (LLM)。

您可能知道, $MONAD 是一个备受期待的区块链项目。 Monai 是 Monad 的第一个人工智能项目,并且已经启动。

$Monai 目前价格 0.41 美元,市值 900 万美元。

虽然价格已经上涨,考虑到人们对 Monad 的浓厚兴趣,但未来它有可能与 $ENQAI 竞争。 这个想法有风险,但如果你愿意等待,它就会对你有用。不妨从现在开始看看团队的表现如何,少量定投可能是值得的。 Uniswap 上可以购买。

Balance AI ($BAI)

Balance AI 是一个全球协作工具包,旨在增强和利用人工智能程序。

对人工智能改进的贡献将得到认可和经济奖励。

Balance AI 作为去中心化机器学习网络的开源协议运行,在该网络中,模型协同工作,并通过权益证明区块链机制,根据其价值赚取 $BAI 代币。

我对这个项目抱有很高的期望,因为它有很多催化剂,是我强烈建议关注的。

我的目标是它在市场超级疯狂阶段达到 10 亿美元的市值。

$wBAI(DEX 交易的封装版本)目前价格 11.7 美元,市值 3500 万美元。

我计划在价格下跌期间买入更多 wBAI,因为我已经错过了最低点。

Uniswap 上可以购买。

EMC Protocol($EMC)

EMC 是 GPU 计算能力、AI 模型聚合和 AI 应用程序商店的突破性市场。

它在去中心化节点上运行 LLM、Stable Diffusion 和换脸功能,将 GPU 矿机转化为尖端的人工智能站。这种创新方法以经济高效的方式提供资源。

EMC 最初在 ICP 上推出,后来过渡到 ARB,在新加坡建立的强大法律框架下运营。

它诞生于万向区块链实验室和 HashKey Capital 共同创建的 Web3 孵化器 Future 3 Campus。

RWA、DePIN 和 AI——三个庞大的叙事汇聚在一个项目中。如果您认可这些叙事,那么它似乎是最佳选择。

$EMC 目前价格 1.5 美元,市值 2500 万美元。

目前价格已经放缓,定投这个项目的策略绝对不会是一个错误。

流通供应量: 2024 年底流通 8000 万枚, 2025 年底 1.9 亿枚。2 年后流通 20% 。

最大供应量: 1 亿枚, 50% 的币保留用于奖励 + 回购和销毁机制。

在 Arbitrum 上的 Uniswap 可以购买。

zKML($ZMKL)

ZKML 是一种注重隐私的第一层协议,融合了零知识证明、多方计算和同态加密 (FHE)。

其特点包括:

交易转换

用于安全通信的加密 ZKOS

高效的跨链交易

跨链隐私

使用 zKSearch 进行隐私浏览

资金被发送到一个秘密的区块链钱包,可以使用私钥确认和提取。这种集成确保了与更广泛的区块链网络的兼容性。

经验丰富的团队正在打造真正优质的产品。许多人甚至没有想到隐私有多重要,很快就会后悔。

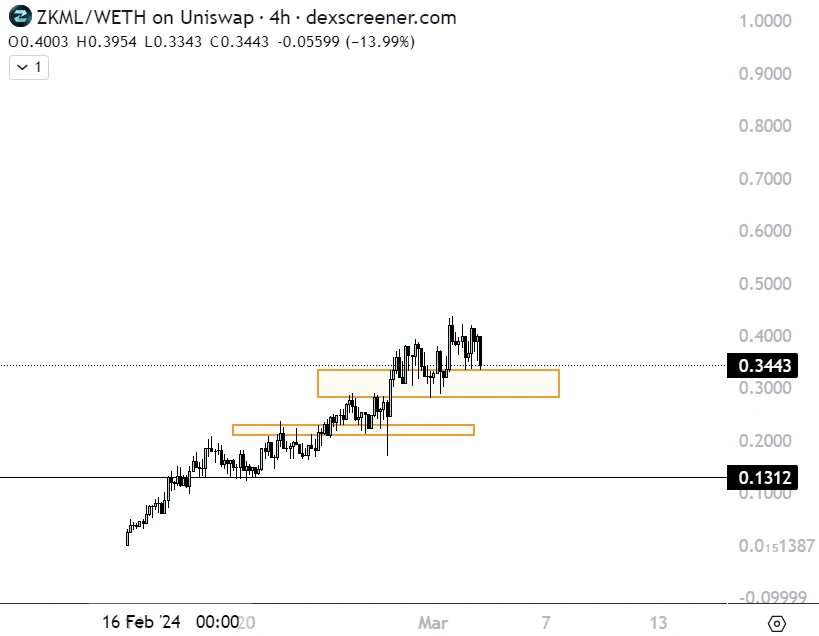

$EMC 目前价格 0.3 美元,市值 3400 万美元。

K 线图非常好看,各个级别的交易都很顺利,$OPSEC 有类似的图表,并且出现巨大的上涨。

Uniswap 上可以购买。

Tao Accounting System ($TAS)

TAS 协议是一个创新的去中心化人工智能项目,致力于在 Bittensor 网络中塑造可替代性的未来。

Tao 征求意见(TRC-20)将成为各种实验性代币标准的先驱。

通过利用 TAS 子网,用户将有能力在 TAO 区块链上生成 TRC-20 代币,为 TRC-20 交易、T-FI 和其他无数机会开辟新的可能性。

另一个冒险的看涨因素是,公共测试网子网将于 3 月 6 日上线。通过它的 dapp,用户将能够铸造和转移新的 TRC-20 。

$TAS 目前价格 0.9 美元,市值 900 万美元。

考虑到年轻的 $TAO 生态系统,我会考虑将此项目添加到我的自选中,它具有引起重大兴趣的潜力。

然而,值得注意的是,这个币的风险也很高,代币价值可能会降至零。应该投入你可以接受归零的资金。

下面的项目已经启动了一段时间,但其全部潜力仍未得到开发。看来它们在熊市期间被忽视了,价格而且尚未飙升。

Wicrypt($WNT)

Wicrypt 是一个去中心化网络,使用户能够共享移动互联网并从中获利。它作为虚拟互联网提供商运营,使用户能够控制自己的数据。

该协议可确保加密,根据数据使用量收费,并将相应费用记入主机。

Wicrypt 的价值仍然被严重低估。凭借 DePIN 领域的巨大潜力,我相信该项目必将取得巨大成功。

WNT 目前价格 0.38 美元,市值 1500 万美元。

从 K 线图看,似乎价格积累已经完成,正在为新的上升趋势做好准备。

在 QuickSwap 上可以购买。

MBD Financials($MBD)

MBD 旨在创建一个全面的生态系统,提供从投资机会到数字房地产、创业支持、教育、广告和健康产品等服务。

开发一个一体化的人工智能集成 RWA 电子商务平台,供企业创建数字产品展示等。

我之前曾提到过这个项目,这个想法仍然具有现实意义。这个项目有很大的潜力,所以我将其添加到我的自选中。

WNT 目前价格 0.00035 美元,市值 500 万美元。

在抹茶交易所和 PancakeSwap 上可以购买。

最后

在对待低市值山寨时,重要的是要注意它们的高波动性和增加的风险。

你不必投资于上面我提到的每个项目;进行彻底的研究,选择您最有信心的,然后考虑购买它。

我若投资于上面这些低市值的山寨,要么意味着我已经可以接受其归零的结局,要么意味着收益将会是 50-100 倍。

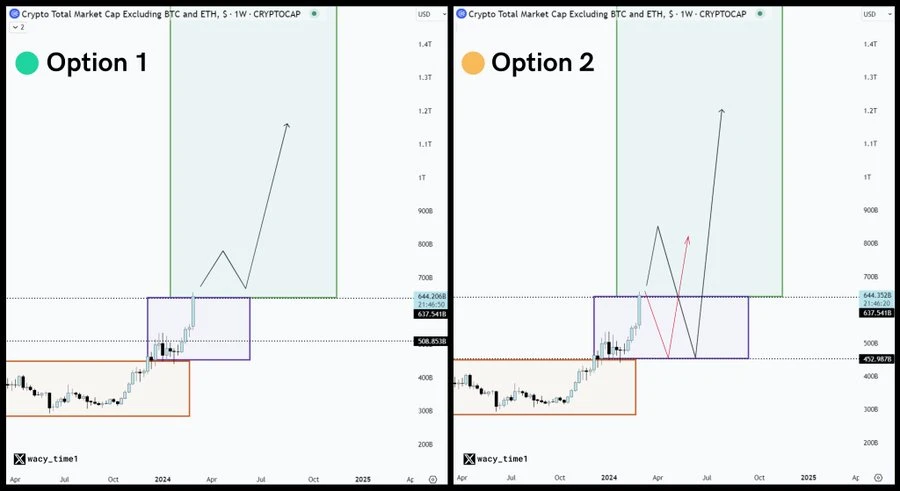

最后,回到山寨季的话题,我想提醒您注意现在潜在的情况。

鉴于市场明显过热和普遍的乐观情绪,我们可能会在大幅上涨之前经历一次震荡。

市场往往会吓到人们,并将他们赶下车,然后继续上涨。

您选择如何根据这些信息采取行动是您的决定,但我准备以较低的价格回购山寨币。

因此我建议在投资组合中持有一部分稳定币以应对此类情况。