原文作者:Aylo, 加密 KOL

原文编译:Felix, PANews

Avalanche 生态有很多可以尝试的应用程序和子网,而这些可能在 2024 年迅速发展。加密 KOL Aylo 盘点了 9 个可以在 Avalanche 生态上交互的未发币项目,并指出了可能获得空投的交互方式。

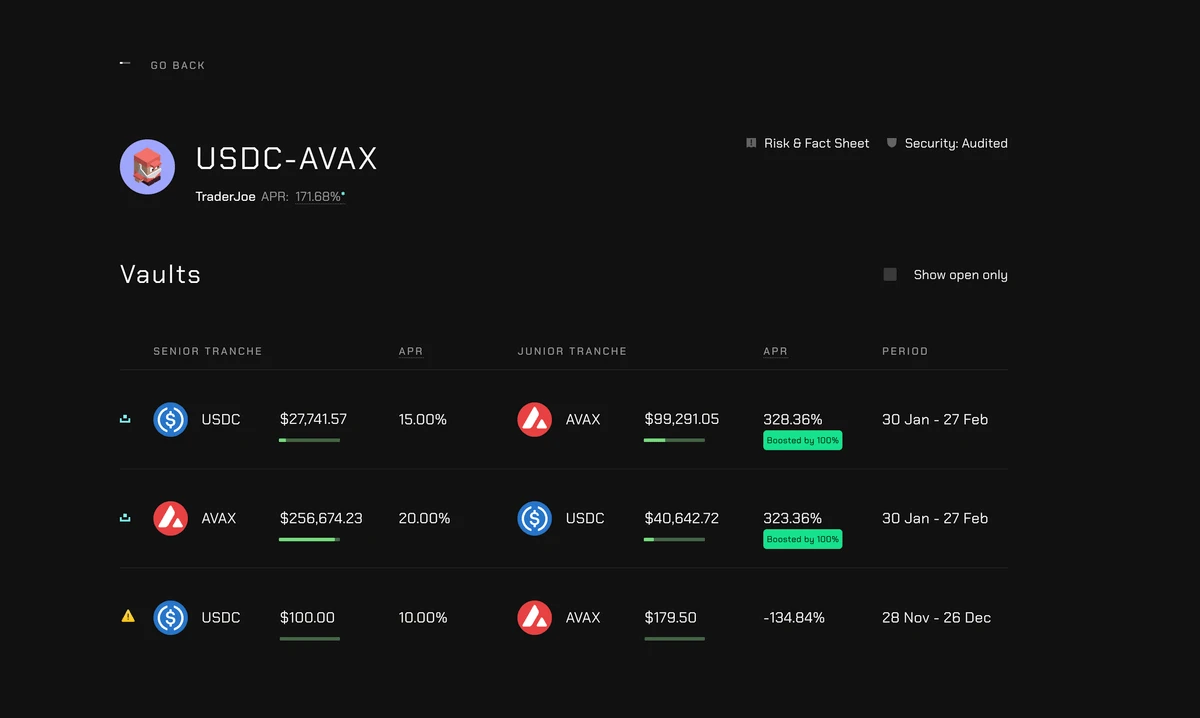

Struct Finance

Struct Finance 在 Avalanche C 链上推出,提供利息金库和“分档”机制,为 DeFi 用户提供固定/非固定收益产品。该机制将计息产品分为不同“档”,分别应用不同的策略。该协议刚刚获得了 100 万美元的 AVAX 激励。用户可以选择一个金库,获得固定或可变收益+积分(空投)。

相关阅读:Avalanche 第三季度报告:领域合作多面开花,生态系统充满活力

Hubble Exchange

Hubble Exchange 是一个使用 USDC 作为 Gas 代币的订单簿 DEX。用户使用 LayerZero 只需点击一次即可将资产从 EVM 直接存入 Hubble。

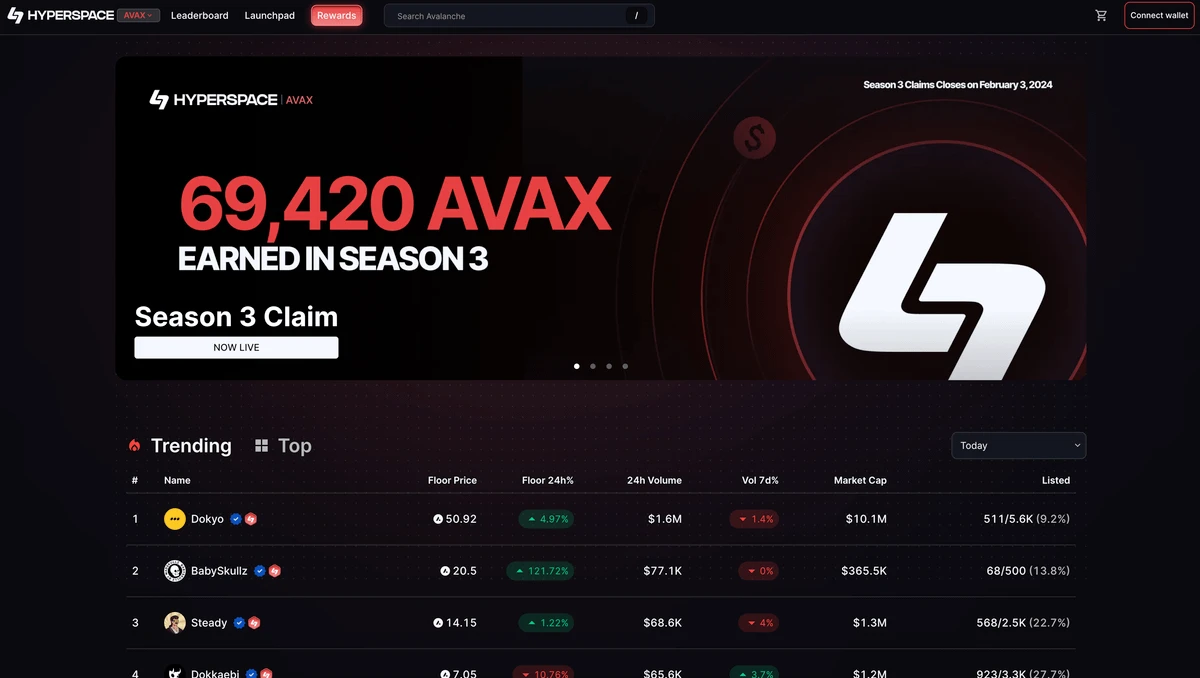

Hyperspace

Avalanche 链上的 NFT 表现得相当不错。用户在 NFT 平台 Hyperspace 上交易 NFT 可以赚取积分,目前正在举行 Season 3 活动,时间截至 2 月 3 日。积分将转化为 AVAX 奖励。

相关阅读:接力 Solana?盘点 Avalanche 生态最新进展

Gunzilla Games

Gunzilla Games 是建立在 Avalanche 子网上的 AAA 游戏工作室。目前正在开发一款赛博朋克大逃杀 2.0 游戏《Off The Grid》(OTG)。2022 年 6 月,Gunzilla Games 完成 4600 万美元融资,Republic Capital 领投、Griffin Gaming Partners、Animoca Brands、Jump Crypto 等参投。

用户可以下载 Technocore 应用程序(测试手机游戏,Season 2 已上线)和应用程序商店中的 GUNZ 平台。

相关阅读:揭秘最有钱的游戏风投基金 Griffin Gaming Partners 投资了哪些Web3项目?

BloodLoop

BloodLoop 一款利用 Avalanche 子网与区块链集成的 5 v 5 英雄射击游戏。

用户可以购买他们的 NFT 系列:https://avax.hyperspace.xyz/collection/avax/semcapsules

完成任务:https://sesamelabs.xyz/bloodloop/

Spellborne

Spellborne(前身为 Defimons)刚刚筹集了一轮资金,其中包括 Animoca 等投资人)。Spellborne 是一款基于 Avalanche 子网构建的复古风格捕捉怪物的 MMORPG 游戏(大型多人在线角色扮演游戏)。

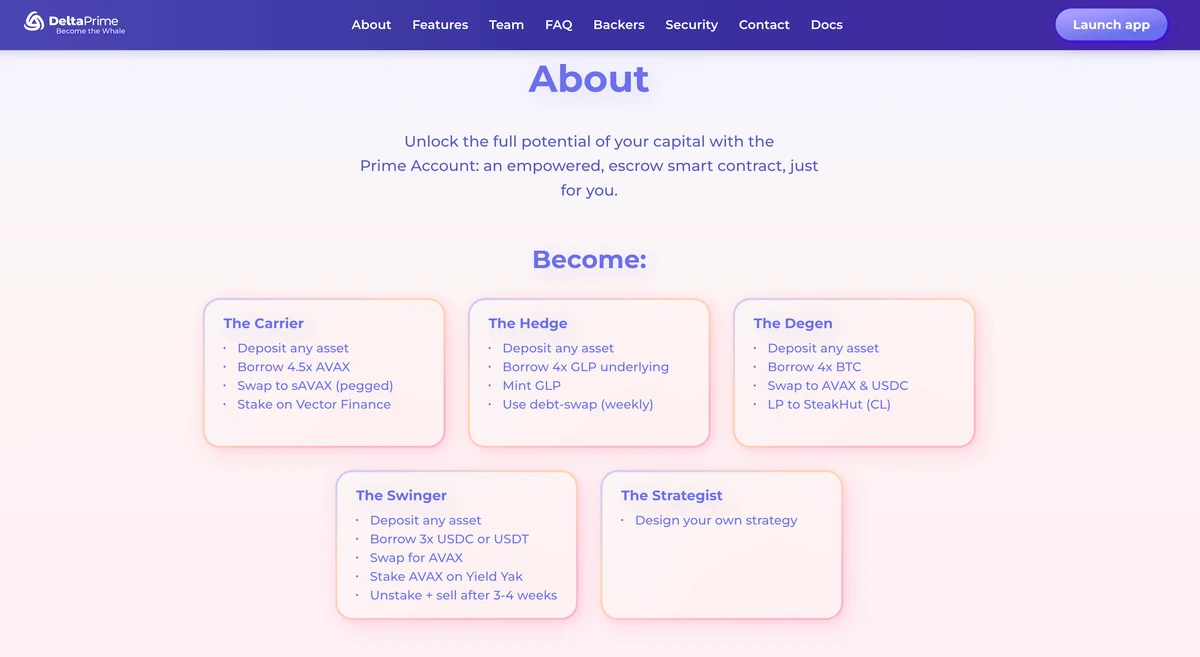

DeltaPrime

DeltaPrime 是一个部署在 Avalanche 上的借贷平台。用户可以存入和借出资金(贷款的最低抵押率为 20% )。借来的资金可用于投资集成协议。

The Arena

去中心化社交协议 The Arena(原名 Stars Arena)值得再次尝试,该协议有了新的领导层,新任首席执行官为 Jason Desimone。该协议的 TVL 在上周翻了一番。用户可以通过参与该平台赚取积分。社交网络或将迎来第二波浪潮。

LEVR.bet

LEVR.bet 是 Avalanche 链上的杠杆体育博彩平台。用户在其网站上注册测试版即可参与并赚取空投。