原文作者:匿名博士

一命二运三风水,这辈子能够掌握多大的财富,其实先天就已经注定了。世界是个巨大的易经模拟器,东玄这套理论流传几千年进化至今仍然有不少高人在使用,定有其道理。华尔街花了一两百年总结了《股市晴雨表》,易经理论穿越近 3000 年历史已然成为经典,著成了人生的晴雨表。

如何将易经与web3做一个形象的嵌套类比?四柱八字类似项目基本面;人的面相、手相、气色类似二级 K 线形态;人所处的居住环境、祖宅风水、磁场等类似宏观环境。一个好的基本面,配合牛市形态,叠加好的宏观环境,就是最佳盈亏比。笔者认为,易经是一套既经典,又新颖的投资哲学与方法论。

本文仅从命理角度分析,不做其他角度解读。

1、财库的概念

先讲一下墓库的概念,财库财库,顾名思义就是有源源不断的财从库里流出来。想要白手起家到 A 8、A 9 甚至更高的财富层级,大部分都是八字自带库且为用神;财运能够让你有发财的机会,而财库是能够让你穿越周期。

币圈很多从业者,牛市账面浮盈非常多,但熊市完全丧失流动性,这就是没有库的结果。大级别的财富自由,命理学中的体现是需要不断的跨越周期、穿越周期、连续跃迁。能在一两轮牛熊活下来的从业者,只要库为用神,资本储备大概率都不会太差。

库在八字里为辰、戌、丑、未,四墓库,也是四个土。辰是水和木的墓库,戌是土、火、金的墓库,丑是水和金的墓库,未是木和火的墓库。

以水为财星且很旺,见辰、丑入库。

以土为财星且很旺,见戌、辰入库。

以火为财星且很旺,见戌、未入库。

以金为财星且很旺,见丑、戌入库。

以木为财星且很旺,见辰、未入库。

通常库的位置在日柱或者时柱为佳,如果无库,大运流年有库来帮身也可完成周期储备。

如何查自己的八字:https://pcbz.iwzwh.com/#/paipan/index

由于四柱八字的复杂性和非易用性,为了方便读者迅速理解自己的组合和墓库的概念,以上结论均为简化版,实际情况要比以上结论复杂的多。

2、从八字组合看财富等级

身旺身弱的概念主要看月令,月令是比劫、印枭,大概率身旺;也要看其他的类型组合,下图给了一个八字组合的旺衰分数图,根据实际情况打分区分身强身弱(特殊格局除外)。

身强身弱根据分数计算,天干地支有:比肩、劫财、正印、偏印。均可得分,得分大于等于 44 分为身强,否则为身弱。(藏干不做计算)

以上的表格仅供参考,实际情况也比上述结论复杂的多,A11 以上级别我们可以看 2 个Web3比较典型的名人案例:CZ、孙哥。

CZ:

庚金日元,身旺财弱八字无库,但为啥是大富大贵之相。四柱八字如果研究到后面,会发现官杀当财看,是更高级别的财富等级。金火两旺,格局清纯,是上上等之格局。天干地支都是三会、三合的局,能量上通常不容易内耗,更多的能量都去发展平台整合资源。

币安真正的崛起是在 2018 年之后, 2018 年刚好也是 CZ 换了一个甲辰大运,戊戌流年;辰戌冲开火库、金库,而 CZ 原局一片金火,比劫开库、官杀开库,取象为不仅事业盘子越做越大,且财全都能守住,这是一步非常上等的关键流年。由于土为印枭,所以开库的同时,CZ 的精神状态和压力都会伴随着 emo。

2021 年辛丑年,巳酉丑三合金局,比劫库再次被打开,比劫可以取象“兄弟姐妹”,对web3企业家而言则是“生态”,bnb 如日中天不就是在这一年。

2024 年甲辰年,辰辰自刑,枭印能量是以往的数十倍,这也许是近十年里最 emo 的一年,甲辰年岁运并临(伏吟),印旺而泄官杀,官杀为财、平台、事业。最近发生的事也印证了这一取象。CZ 只要能熬过去,跨越周期,后续的走势都不会太差。

孙哥:

丙火日元,身弱从儿(假从儿格),自带财库。2013 年走丙戌大运,大运让孙哥的格局走成了真从弱,从弱反为强,可当身强看。伤官伤尽的格局,也是非常 top 的食伤生财局。

与 cz 获取财富的姿势不一样,伤官伤尽的局通常通过“技能”、手腕、投机等获得巨额财富。伤官格很重的一个负面特征是“杠精”、“侵略性”,你说 A 他干 B,你干 B 他扯 C;食伤当财看也是大富大贵之相。

从格的一个特征是波动性极大,在好的大运流年,十倍的顺风顺水;在差的大运流年,逆境状态是普通人的十倍。孙哥和 CZ 的区别在于,假定从格的人按身弱看,眼高手低,每天追热点或者成为热点;CZ 八字身旺则专注于经营自己的一亩三分地。不同的八字格局,呈现出的处事方式截然相反,性格决定命运,八字决定性格。

2013 ~ 2022 丙戌大运,戌为土库,丑未戌三刑,开财库、食伤库;孙哥这十年几乎是开挂状态,从大学毕业、创业、进入币圈到巨资收购火币,这是普通人一辈子难以逾越的天花板。从格的特征是走到了好的大运等于加了百倍杠杆。

孙哥自带丑土财库,只要财星入库,呈现的状态会有一些“貔貅”的特征,能赚能守是很重要的投资技能。cz 满盘官杀劫财,属于又富又贵的局;孙哥食伤生财,通常只富不贵;不同局的八字做功,虽都为求财,但呈现出的特征都不一样。

2023 ~ 2032 丁亥大运,食伤库大运走完,水为孙哥的官杀,伤官见官透干通根,这步大运对孙哥来说可以称得上“熊市震荡”。孙哥能否守住 A 11 就看这步大运如何做防守,web3的逆风局并不是那么容易上手的。官杀对从儿格来说等于内耗,虽有财通根,但官杀也可取象为“负债”,事业盘子在扩大,但利润有可能在收缩。

2024 甲辰年,大运亥子丑三会水,流年申子辰三合水,注定是官杀和食伤的内耗战;火币近期发生的丢币事件,都是自 2023 年换运之后才发生的。也许近几年里,收购火币对孙哥来说是最高光的时刻。在逆风局中,如何守住和传承财富,是大佬的必修课。

孙哥晚年己丑运算是挺不错的一步大运,己丑对原局而言也是岁运并临,但对从格而言为喜用,则没有太大的负面影响,至少财富在这个周期是可以继续实现连续跃迁的。

3、什么样的八字适合做交易

神鱼有个广为流传的经典观点:“币圈是对性格,认知的补偿”;个人非常认同,八字决定性格,性格决定命运,什么样的八字适合在web3赚钱,下面会一一总结。

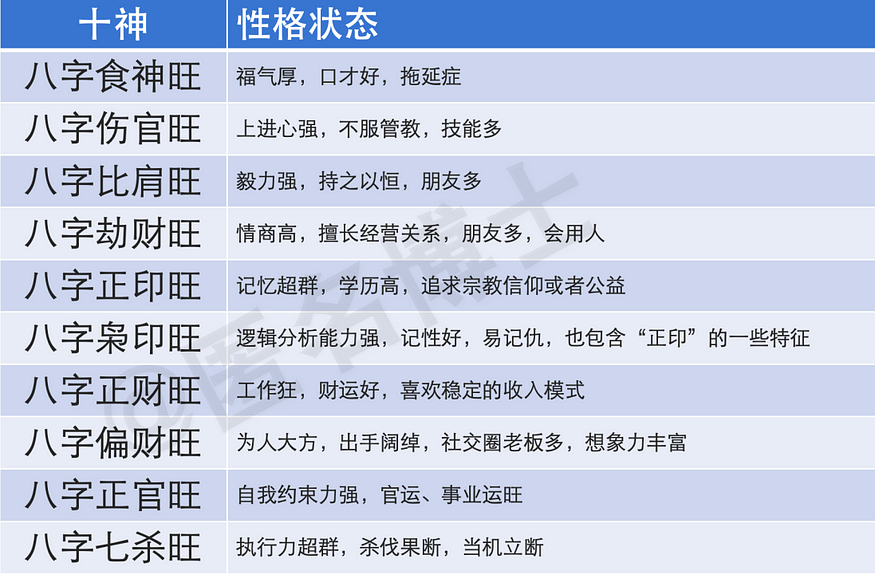

先来看看不同的八字十神所呈现出来的取象:

以上八字的十个十神,组成了自己的性格画像,可以根据自己的八字把性格公式嵌套进去。币圈放大了人性的善与恶,世界是易经的模拟器来形容一点也不为过。

我们再看看孙哥的八字,孙哥实际上是一个“天才”交易员,伤官代表技能,偏财代表财运想象力,正官代表自我约束力;好的交易员(投资家)是需要优秀的投资技能(食伤)+对行业的想象(偏财)+对赔率的思考与约束(正官),投资与交易能力也绝对是一流的,交易和投资没有太本质区别,都是对自己性格的代偿,剩下的靠运。

孙哥的组合为食伤生财,但不代表只有这种类型适合做交易。交易并不是web3的全部,但人的一生本质上都是在交易,我们在用有限的“生命”去交易“资源”,知己知彼,寻找属于自己的 alpha 才是正确的方式。

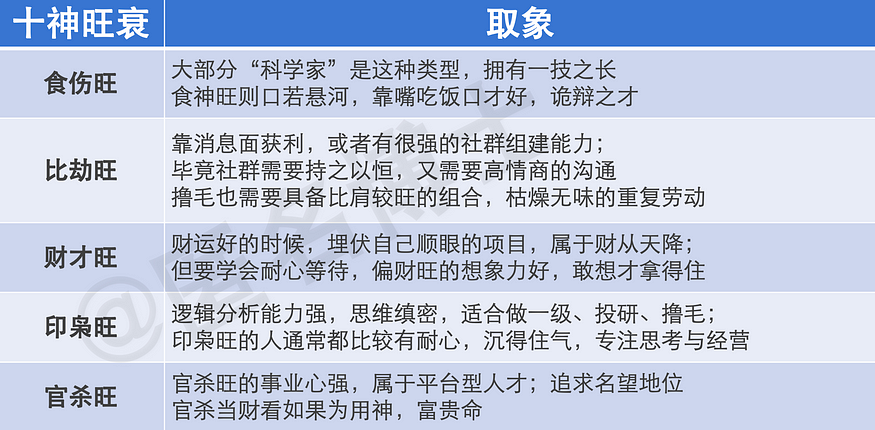

4、什么样的八字适合做撸毛、一级、投研、kol、科学家

以上总结,涵盖了大部分币圈的财富积累姿势,自己属于什么性格,擅长吃哪碗饭,知人之命知天。

5、什么样的八字组合与玄学有缘

通常八字土旺、印旺的格局会对玄学有比较深的缘分,很多web3类型的公链项目都是这种格局组合,比如以太坊、kas 等;土可生万物,土旺则能承载更多的生态、意识形态、以及一切可被“编程”的新世界。某种程度上来说,以太坊何尝不是一个“宗教组织”。

关于如何使用四柱八字去看web3项目的“技术形态”的案例,不在本篇文章做解读,日后有时间会专门出一篇文章深入浅出使用易经作为玄学技术指标去看web3项目的取象及走势。

6、结语

没有财库也不必担心,大运流年也可以来补;就算大运流年没有财库来补,风水上也是可以解决库和财的问题。关于如何在风水能量上构建属于自己的财库,也不在本文的探讨范围,日后有机会分享简单实用的补库技法。

没有完美的性格,也没有完美的八字,币圈是易经的模拟器加速版,找到适合自己的路,寻找属于自己的 alpha。大佬成功的故事可以听,但不可以学,他成功的道路上帝只为他设定,他自己也是摸着石头过河。时来运转,现在你也需要摸索出属于自己的 alpha。

文中提到的命理观点仅为本人简化版的解读,不代表最终严谨答案。