原创|Odaily星球日报

作者|jk

美国当地时间 1 月 31 日周三,已破产的加密货币交易所 FTX 向法庭表示预计能够全额偿还其客户。这一声明是通过法庭听证会公布的,美国破产法官 John Dorsey 已初步批准了这个日期,尽管有相当一部分债权人人对此表示不认同。

根据法庭程序,FTX 放弃了重新启动其平台的计划,转而专注于全额偿还其前客户。根据法庭程序,FTX 由于缺乏买家而放弃了重新启动其平台的计划。顾问们在市场上进行了很彻底的搜寻,以找到愿意重启 FTX 的投资者,但没有人愿意提供重启交易所所需的现金。

FTX 律师 Andrew Dietderich 表示,偿还过程将要求索赔人提交证明,以验证他们确实持有并在 FTX 上损失了资产。这一过程将由重组顾问审查。

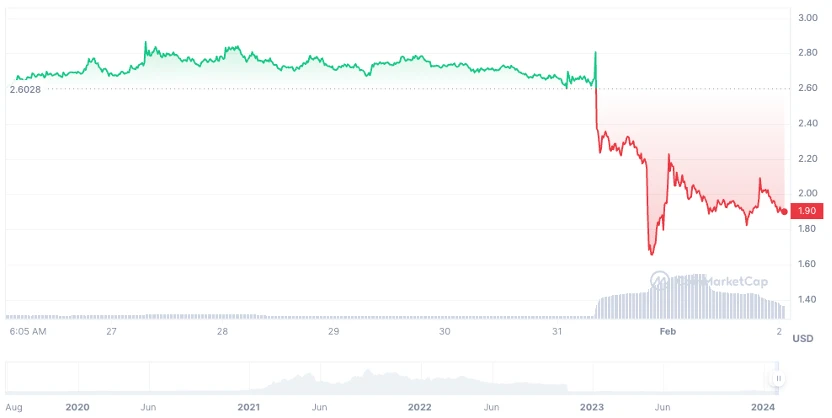

平台币 FTT 还有用吗?

FTX 的原生代币 FTT 在公司的这一计划公布后短暂上涨,但随后急剧下跌。几日前,FTT 的价格一直在 2.65 美元左右短暂波动,然而如今已经来到了 1.91 美元左右,最低点来到了 1.65 美元, 7 日跌幅达到了 27.04% 。

FTT 走势,来源:Coinmarketcap

这一市场反应实际上是可以期待的。按照此前期待重启的剧本而言,FTT 的升值是基于 FTX 重启之后仍然有可能重新启用 FTT 作为原生代币,或者是按照一部分比例去兑换 FTT 用来发布新的原生代币。然而,这一预期随着 FTX 宣布不会重启而破灭;在放弃重启以后,FTT 事实上已经找不到新的用途,且随着 FTX 不断清算资产用以赔付客户,FTT 的价值必然随着抛售进一步下跌。

按照最坏的预期来看,FTT 可能终究会成为如同 Terra 崩溃后的 Luna Classic 一样,成为事实上的 memecoin,跟随每次相关新闻的出现而波动,但已经极大概率无法回到当年的高点了。

全额赔付:是个好消息,但是是以什么时间点的资产价格赔付?

FTX 之前报告称,有超过 36, 000 项索赔,总额约为 160 亿美元。去年,它表示只能赔偿大约 90% 的客户。而现在,打算全额赔付客户自然是一个更好的消息,不过也有一个随之而来的问题;FTX 很可能不能按照原有的代币种类赔付给客户,那么如果按照美元价值赔付的话,依据的是什么时间点的美元价值?

若是在 FTX 崩溃前,比特币的价值是 2 万美元左右。若是按照 FTX 宣布破产的时间,比特币的价值则来到了 16000 美元左右,而如今则是 43000 美元左右,差值巨大。“其中许多索赔是基于那个动荡时期货币价值大幅下降的情况提出的,”FTX 债权人委员会律师 Kris Hansen 在周三的听证会上说。

而根据彭博社报道,美国破产法官 John Dorsey 裁定,每项索赔的规模将基于 FTX 申请破产当日所欠客户或债权人的金额。Dorsey 还批准了估算每个债权人和客户所欠金额的规则。一些客户抱怨,将他们的索赔固定在 2022 年底的价格上,会导致他们错过数字资产价格上涨的机会。Dorsey 裁定,破产规则要求公司的债务必须与其申请法院保护的日期挂钩。所以,这一点与之前 Odaily 报道的 FTX 曾提议过的索赔价值相似,按照的是比特币在 16000 美元左右的价格进行赔付,而这无疑将会对债权人带来很大的损失。

而从好的方面想,如果不是从 2023 年开始的这一轮小牛市,FTX 破产后剩余的加密货币资产未必足够它偿还所有的投资者。也就是说,按照近日的价格来偿还已经是几乎不可能的事情,但是这一轮升值才让 FTX 按照 2022 年 11 月的价格赔付变得可能。

“我希望法庭和利益相关者理解这不是一个保证,而是一个目标,”Dietderich 说。“在我们和这个结果之间还有大量的工作和风险。但我们相信这个目标是可达到的,并且我们有实现它的策略。”