据 Dune 数据,以太坊信标链质押总量已超 2942 万枚 ETH,占 ETH 总供应量的 24.53% 。自以太坊上海升级后质押净流入达 955.13 万枚 ETH,可见以太坊原生质押正如火如荼地进行中。

而市场似乎已不满足于一级市场的无风险质押收益,再质押协议如雨后春笋般涌出,各大质押平台纷纷带资下场,推出属于自己的再质押协议。

都对老百姓口袋里的以太坊「虎视眈眈」?粗略统计,头部再质押协议已催生出近 20 种以太坊衍生品(XXXETH/ETHXXX)。本文梳理了 6 个主流再质押协议及其金库,在不去重的情况下,至少有价值 35.26 亿美元以太坊衍生品资产在不断生息,约占信标链质押总量的 5.2% ,「套娃」正在进行中。

EigenLayer

EigenLayer 是一个基于以太坊的再质押(Re-staking)协议,为未来整个以太坊的加密经济体系提供以太坊级别的安全性。它允许用户通过 EigenLayer 智能合约将原生 ETH、LSDETH 及 LP Token 进行再质押并得到验证奖励,让第三方项目在可享受 ETH 主网安全性的同时还能获得更多奖励收益,从而实现共赢。

2022 年 8 月 1 日,EigenLayer 开发商 EigenLabs 完成 1450 万美元种子轮融资,Polychain Capital 与 Ethereal Ventures 联合领投。

2023 年 3 月 29 日,EigenLayer 开发商 EigenLabs 完成 5000 万美元 A 轮融资,Blockchain Capital 领投,Electric Capital、Polychain Capital、Hack VC、Finality Capital Partner、Coinbase Ventures 和 IOSG Venture 等参投。

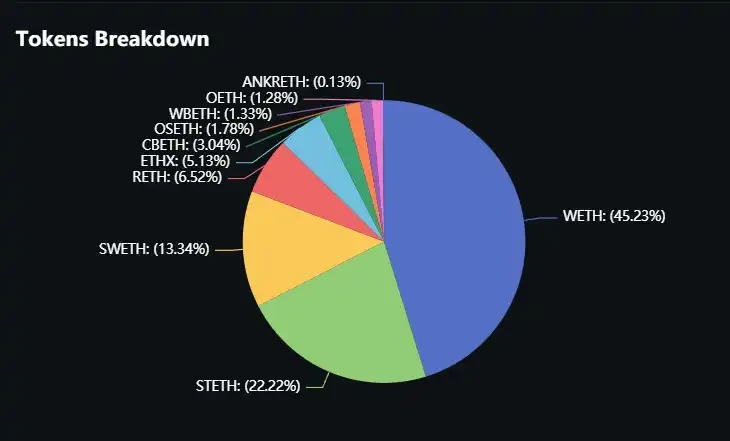

TVL: 20.45 亿美元

据 Defillama 数据,当前 EigenLayer 总 TVL 为 20.45 亿美元,金库中占比前三的 ETH 及其衍生品分别为:WETH(45.23% )、STETH(22.22% )、SWETH(13.34% )。

ether.fi

ether.fi 是一个非托管流动性质押平台,于 2023 年 11 月 12 日在主网上线了流动性质押代币 eETH,用户在 ether.fi 上质押 ETH 将收到协议 LST (eETH),可用于在整个 DeFi 生态系统中产生更多收益,包括再质押到 EigenLayer 上。在整个过程中,用户将保留对其私钥的控制权,同时将以太坊验证器操作委托给节点运营商。通过其协议生成的每个验证器都将表示为 NFT。存入至少 32 ETH 的以太坊质押者将持有 NFT,代表了验证者的经济利益。

ether.fi 公布了 2024 年上半年的路线图。团队将 TGE 定在 4 月份,其他关键日期包括二月发布 DAO 框架、三月发布代币经济学文档。此外,主网 v3 计划于第二季度初发布。

2023 年 2 月 28 日,ether.fi 完成 530 万美元融资,North Island Ventures、Chapter One 和 Node Capital 共同领投,BitMex 创始人 Arthur Hayes 等参投。

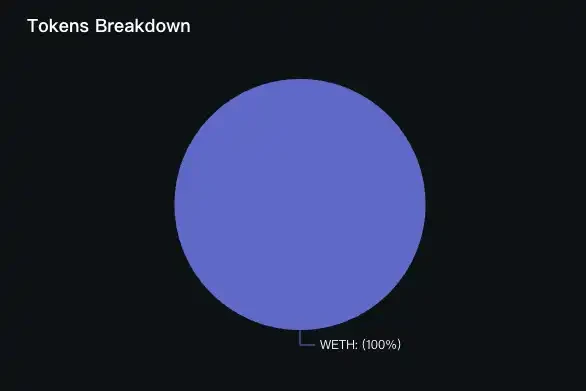

TVL: 5.09 亿美元

据 Defillama 数据,当前 ether.fi TVL 达 5.09 亿美元,月涨幅达 367% ,目前金库中有 22 万枚 WETH。

Swell Network

Swell Network 是以太坊流动性再质押协议,用户可通过抵押 swETH 和提供流动性来收集 Pearls,然后在今年晚些时候的 Token 生成活动上兑换成 SWELL,将分配 5000 万枚 SWELL(5% )。Swell Network 于 1 月 30 日推出再质押代币 rswETH(Restaked Swell Ether),用户可赚取 Pearls、 EigenLayer 积分和未来再质押奖励,为用户提供对 EigenLayer Restaking 的无限制访问,可在 DeFi 中使用,同时继续累积 Restaking 奖励。

2022 年 3 月 14 日,Swell Network 完成 375 万美元种子轮融资,由 Framework Ventures 领投,IOSG Ventures、Apollo Capital、Maven 11 以及天使投资人 Mark Cuban、Synthetix 联合创始人 Kain Warwick 以及 Jordan Momtazi、Balancer 创始人 Fernando Martinelli、Ryan Sean Adams、Bankless 联合创始人 David Hoffman、Ren Protocol 联合创始人 Loong Wang 和 Mask Network 的创始人 Suji Yan 等参投。

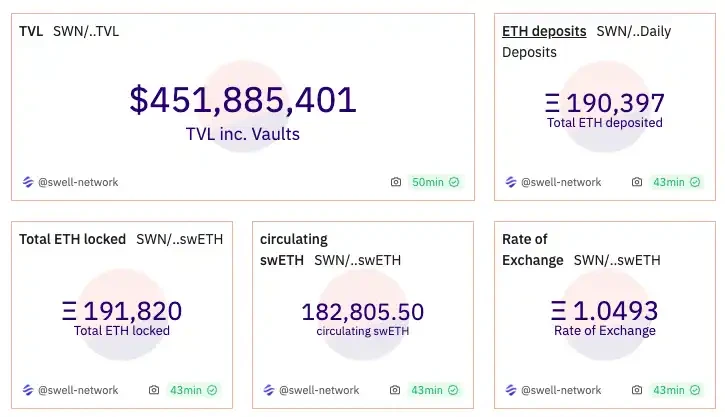

TVL: 4.51 亿美元

据 Defillama 数据,当前 Swell Network TVL 达 4.51 亿美元,其中金库中储存的 swETH 达 191, 070 枚,rswETH 为 1, 475 枚。

Kelp DAO

Kelp DAO 是多链 LSD 平台 Stader Lab 旗下的 Restaking 项目,基于 EigenLayer 以 rsETH 构建了的 LRT(Liquid Restaked Token)解决方案。

Kelp Dao 质押用户可赚取 Kelp 积分,项目金库中的以太坊也质押于 EigenLayer,并同时为社区用户共享积分。2023 年 12 月 19 日,Kelp DAO 仅上线 6 日已吸引约 38, 000 枚 ETH 存款。

2021 年 10 月 7 日,Stader Labs 宣布完成 400 万美元种子轮融资,Pantera Capital 领投,Coinbase Ventures、True Ventures、Jump Capital、Proof Group、Hypersphere 等参投。

2022 年 1 月 20 日,Stader Labs 宣布以 4.5 亿估值完成 1250 万美元私募融资。本轮融资由三箭资本领投,Blockchain com、Accomplice、DACM、GoldenTree Asset Management、Accel、Amber、 4 RC、Figment 及多位天使投资人跟投。

TVL: 2.55 亿美元

据 Defillama 数据,当前 Kelp DAO 总 TVL 为 2.55 亿美元,金库中共有三种以太坊衍生品,分别为: 6.836 万枚 ETHX(63.02% )、 3.523 万枚 STETH(31.78% )、 0.538 SFRXETH(5.2% )

Renzo

Renzo 是一个流动性再质押协议,目前已在 EigenLayer 的主网上运行,Renzo 的核心是 ezETH,这是一种流动性再质押代币(Liquid Restaking Token, LRT),用户可以通过将以太坊或 LST 存入 Renzo 来铸造这种代币。ezETH 可以进一步用于其他 DeFi 协议,从而获得复利回报。Renzo 抽象了终端用户的所有复杂性,使他们能够低门槛地参与 Eigenlayer 生态的再质押。作为原生态的再质押产品,优势在于可充分质押,即不受到 EigenLayer LST 存款限额的约束。

1 月 15 日,Eigenlayer 生态的流动性再质押协议 Renzo 宣布完成 300 万美元种子轮融资,本轮融资由 Maven 11 领投,SevenX Ventures、Figment Capital 和 IOSG 等参投。

TVL: 1.55 亿美元

据 Defillama 数据,当前 Renzo TVL 达 1.55 亿美元,月涨幅达 1368% ,金库中储存的 ezETH 达 67109 枚。

Eigenpie

EigenLayer 是一个基于以太坊的再质押(Re-staking)协议,允许用户通过 EigenLayer 智能合约将原生 ETH、LSDETH 及 LP Token 进行再质押并得到验证奖励。由去中心化流动性聚合协议 Magpie 与 EigenLayer 联合推出。Eigenpie 是基于 EigenLayer 智能合约技术从而为用户提供 LRT 服务,用户可以同时从以太坊质押和 EigenLayer 中获得被动收入,而无需锁定期。

隔离再质押(Isolated Liquid Restaking)代币是由 Eigenpie 生成的再质押凭证,只能通过存入特定的 LST 来铸造,而不能通过存放一篮子不同的 LST 来铸造。用户可以将其 LST 存入 Eigenpie,以获得其特定资产的 LRT 版本。用户将 LST 存入 Eigenpie 时收到的 ILR 代币将保留其原始名称,并添加前缀「m」。

Eigenpie 原生代币为 EGP,总供应量为 1000 万,分配包括 IDO(40% )、社区激励(35% )、Magpie Treasury(15% )和早期支持者空投(10% )。将通过公平启动引入 EGP 代币,无 VC 或预售活动的参与。团队正式放弃代币分配,将 15% 的 EGP 代币分配给 Magpie Treasury。

2022 年 9 月 8 日,Magpie Protocol 宣布完成 300 万美元种子轮融资,此轮融资由 Jump Crypto、ArkStream Capital、Sandeep Nailwal、GSR Markets、Parafi Capital、Republic Capital、Big Brain Holdings、Serafund、Faculty Group、MH Ventures、D 1 Ventures、Apollo Capital 等参投。

TVL: 1.11 亿美元

据 Defillama 数据,当前 Eigenpie 总 TVL 达 1.11 亿美元,金库中占比前三的以太坊衍生品分别为:STETH( 50.73% )、WBETH( 14.75% )、METH(14.62% )。