POKT 网络(又名 Pocket Network)已经通过分布在 22 个国家/地区的数千个节点为近 7000 亿个中继提供服务,目标是在下一轮创新周期中达到 1 万亿次 RPC 中继。

POKT Network (POKT) 于 2017 年开始构建其去中心化物理基础设施网络(DePIN)协议,并于 2020 年部署到主网,比 DePIN 一词的出现还要早两年。 POKT Network (POKT) 提供了一种激励和协作层,可以实现区块链数据在任何应用程序之间进行去中心化传输。

这种架构方式的优势是:

无可比拟的成本优势: POKT Network 的协议费用比中心化替代方案的 RPC 服务成本低 80% 以上;

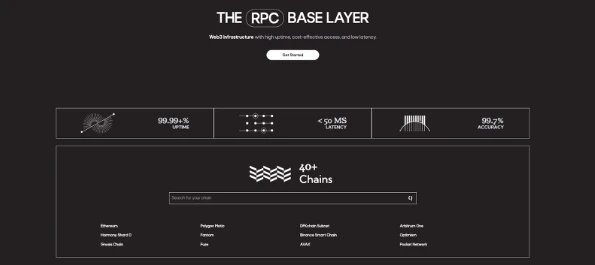

无与伦比的可扩展性: POKT Network 支持访问 50 多个链,而市场领导者 Alchemy 只支持 8 个链;

强大的基础设施: POKT Network 比中心化提供商更具韧性和稳健性。

经过 3 年主网运营积累的经验,实现了今天(POKT Network)所能提供的性能: 99.99% 的正常运行时间、 99.7% 的中继准确性和小于 50 毫秒的延迟。

所有这些都被纳入一个重大的协议升级中,即以信息论之父 Claude Shannon 的名字命名为「Shannon 升级」,目标是利用 Celestia 模块化区块链技术的最新发展,在 2024 年第二季度末进入主网。

这是建立在 2023 年实现的里程碑的基础上的,随着 POKT Network (POKT) 进入了一个新的成熟阶段,引入了协议收入,将通胀率控制在 5% 以下,关闭了不可持续的需求,并启动了为网络提供新接入点(“网关”)的战略。

这种“网关”策略将在 2024 年进行扩展,使更多的 RPC 业务能够在 POKT Network (POKT) 的 RPC 基础层之上构建,预计到 2024 年第二季度末将有多达 10 个业务接入。这些业务中的每一项都将推动对底层网络的需求,增加协议收入并缩短与 1 万亿次中继目标的距离。

“网关”还支持跨网络的创新。一个网关正在努力引入“webhooks”,这可能会使目前价值 10 亿美元的 RPC 机会增加约 10% ,并且已经在进行升级,使 POKT Network 能够为与任何开源 AI LLM(大型语言模型)交互的应用程序提供数据,这是一个价值 100 亿美元的市场。

“ POKT Network (POKT) 率先扩展了 DePIN 供应侧基础设施和治理的扩展,接下来我们将开启 DePIN 增长新策略。” POKT Network (POKT) 基金会董事 Dermot O’Riordan 表示。

关于 POKT Network (POKT)

POKT Network (POKT) (也称为 Pocket Network)是一家领先的 DePIN(去中心化物理基础设施网络),能够以最低的成本、最长的正常运行时间和高度的可扩展性为应用程序提供数据连接。 如今,这些数据连接涉及对分布式远程过程调用 (RPC) 基础设施的多链访问,但未来可能会扩展到服务其他类型的数据连接,包括支持主流社交媒体和开源 AI LLM(大型语言模型)的开源数据库。

POKT DAO 是一个价值驱动、协作、开源社区,负责构建和治理该项目。我们重要的数字基础设施是由用户构建和管理的。

POKT Network 基金会是 POKT DAO 授权的实体,负责执行 POKT Network 的战略愿景。

更多详情可以访问 https://www.pokt.network/ 官网查看。