继 Maestro、Unibot、Banana Gun 之后,Telegram Bot 又新增一员大将 Alfred,成为这两日的小热点。

据官方文档显示,Alfred 的创始人是 Flashbots 联创 Stephane Gosselin。Stephane Gosselin 和 Phil Daian 于 2020 年创立了 Flashbots。最近几天许多社区和 KOL 在传播 Alfred 时,称 Stephane Gosselin 为「MEV」之父,BlockBeats 发现这种说法有些「吹捧」。

矿工可提取价值(MEV)这一概念由 Phil Daian 在名为《Flash Boys 2.0 》的论文中首先提出,虽然「MEV」之父有点「过」了,但 Flashbots 联创 Stephane Gosselin 也确实在 MEV 届做出了贡献,可以说得上是 MEV 老 OG。

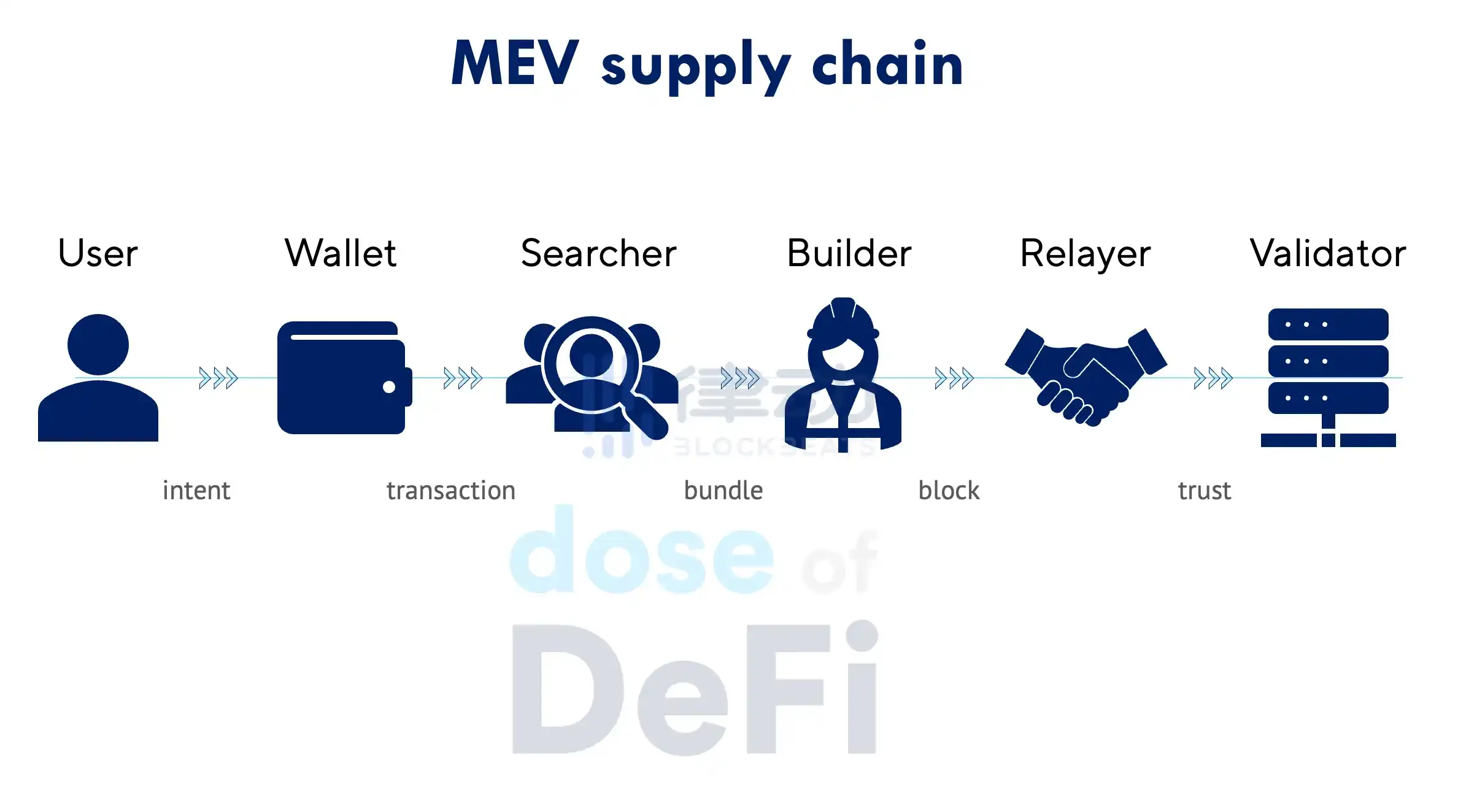

目前,以太坊通过 MEV-Boost 实现 PBS,这是由验证者运行的 Flashbots 提供的软件,它允许随机选择的区块提议者将创建最赚钱的区块的权利拍卖给出价最高的竞标者。迄今为止,PBS 已经通过仅让质押者参与,而不需要使用复杂的 MEV 策略,实现了 MEV 奖励的普及。然而,MEV 供应链的其他部分仍然存在集中化和审查的风险。

这个图表展示了 MEV 供应链的主要组成部分,据 DeFi 研究员 Chris Powers 在《MEV resolution: Are we there yet?》文中写道,说该术语最早正是由 Stephane Gosselin 首次提出。

但在 2022 年底,据 BlockBeats 消息报道,Stephane Gosselin 因希望验证者支持未经审查的中继,而与团队发生分歧,并辞职。当时 Gosselin 在一份声明中表示,对于一个多样化和有竞争力的 MEV 生态系统,保持审查阻力至关重要。「在短期内,我希望验证者能够避免连接到执行审查的中继。区块空间供应商对审查施加经济压力将有助于避免审查过度。」

Alfred :解决三明治攻击的狙击新币交易 Bot

上一个狙击开盘 Sniper 的交易 Bot Banana Gun,在上线初期,日活用户数量很快就超过了 Unibot,甚至直逼 Maestro。已经证明了狙击开盘是用户们的真实需求。

相关阅读:《赶超 Unibot,即将发售的黑马 Banana Gun 有多大潜力?》

不过 Alfred 显然更了解 MEV 方面的研究,在 Alfred 看来,用户在通过传统方法访问 Crypto 和 DeFi 时会遇到很大的摩擦:

首先,使用钱包时通常会遇到下载粗略的钱包应用程序或令人困惑的浏览器扩展程序;其次,建立交易是一种复杂而压倒性的体验,要选择要使用的 DEX 或前端,然后了解如何设置滑点、基本费用和优先级费用等内容;同时,对于普通用户,除了「我想将令牌 A 换成令牌 B」之外功能较少,狙击新代币发布等功能仅是为高度复杂的参与者保留的。

最重要的是,加密内存池是一片黑暗的森林,普通用户每次都会通过抢先运行、夹在中间或只是在他们的订单上得到糟糕的执行而获得 rekt。

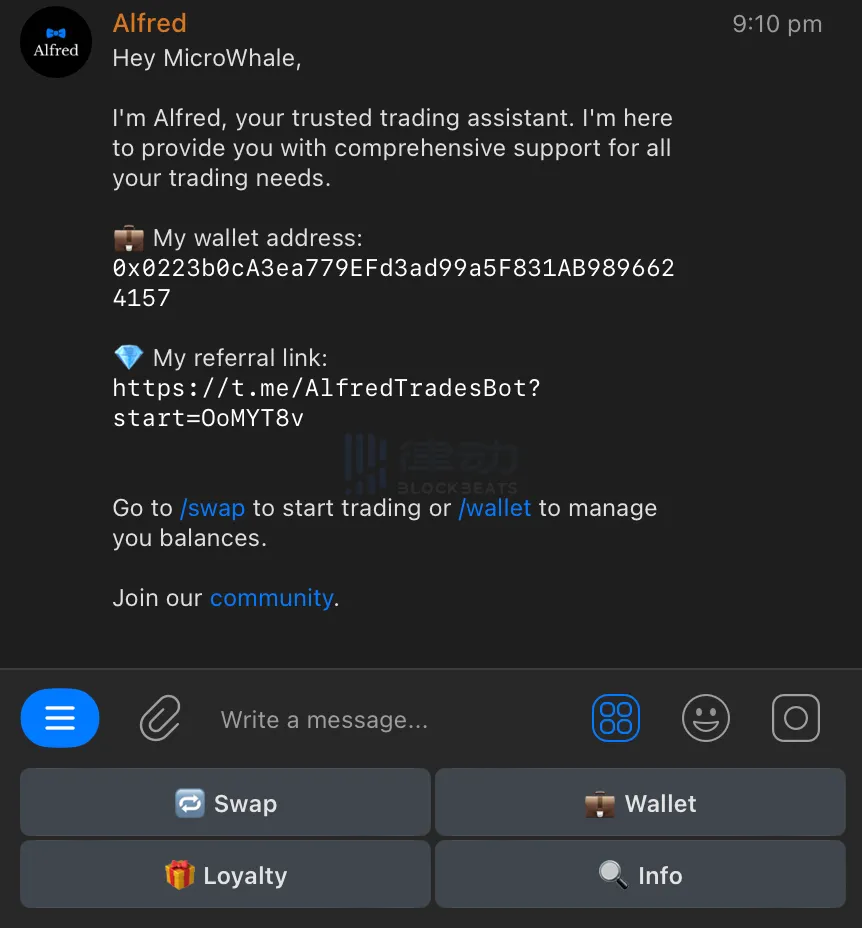

据官方文档显示,Alfred 是一个快速安全的交易机器人,直接内置于 Telegram 中。只需单击几下即可将机器人添加到 Telegram 后,用户将直接在 Telegram 应用程序界面中获得一个易于使用的加密钱包和一整套高级交易工具。Aldfred 将成为用户的交易管家,只需点击几下即可帮助持有、购买、出售和狙击代币。用户的所有交易都将是完全私密的,并受到保护,免受三明治机器人和领跑者等对抗性行为者的侵害,确保用户在交易中获得最佳执行。

目前 Alfred(AlfredTradesBot)仅作为一个 Telegram 机器人机器人的形式出现,允许用户直接从 Telegram 帐户在以太坊上购买、出售和狙击代币。但在未来,Alfred 将作为所有 DeFi 和加密活动的入口和平台。

Alfred 相关 MeMe 图

Alfred 狙击的工作原理

当您想狙击即将到来的代币发布时,可以在 Alfred 机器人中设置狙击。您只能为交易尚未激活的代币/池设置狙击。如果您想购买现有代币,只需点击 Buy 功能而不是狙击。

然后,Alfred 监控区块链内存池中是否有待处理的目标交易。有效的目标交易是指如果在目标交易之后直接执行的买入交易将有效(不会恢复)。常见的目标交易包括:Pool_creation/liquidity_add(创建池子、增加流动性)和 Trading is un-paused(交易未暂停)。

当 Alfred 在内存池中看到有效的目标交易时,它将在目标交易之后直接创建一个包含您的狙击交易的捆绑包,并尝试将该捆绑包登陆链上。如果多个 Alfred 用户试图狙击同一个令牌,它会将所有狙击捆绑在一起,按贿赂金额排序。也就是说,那些愿意贿赂更多的人会先购买。

怎么使用 Alfred

1. 创建钱包

和其他 Telegram Bot 类似,使用链接进入将 Alfred 添加到 Telegram,然后单击 Start,设置钱包和交易账户。

将 Alfred bot 添加到您的 Telegram 帐户后,您将立即生成您的钱包。下一步是存入一些以太坊来为您的钱包提供资金。

由于以太坊区块链的机制,您的钱包中需要一些以太坊(ETH)来支付交易时的汽油费。通过将一些以太坊发送到您生成的钱包地址,将一些以太坊存入您的钱包。如果您想出售或交易其他 ERC 20 代币,您也应该将它们发送到此地址。

2. 发送 ETH 和代币

要从您的 Alfred 钱包发送 ETH 或代币,请单击 Wallet > Send ;指定货币(代币或 ETH)和您希望发送的金额,输入目标钱包地址,然后单击 Press to continue

3. 设置狙击 Sniping

单击「Swap,接着点 Sniper 和 Create a new snipe 后,输入您要狙击的代币的合约地址。接下来,您需要配置您的 Snipe。

输入您要用于购买的 ETH 数量,输入贿赂(贿赂越高,您最先落地的可能性就越大),选择降落在 Block 0 还是降落在下一个区块购买 Block + 2 。

接着单击创建 Press to create a new snipe 完成创建。一旦确定了有效的目标交易,狙击将尝试执行,您将直接在 Telegram 中收到成功或失败的通知。您可以通过单击「Swap > 来编辑金额或取消狙击。

Alfred 的忠诚度积分

Alfred 的忠诚度积分是通过与 Alfred Bot 的各种互动获得的。您产生的积分越多,您节省的交易费用就越多。未来将通过忠诚度积分计划提供额外的福利和奖励。所有用户都从 Chef 级别开始,随着他们获得更多积分而增加到更高的级别。

获得忠诚度积分的几种方式:

1. 首次使用的用户将获得「入职奖励」:首次存款: 500 积分;首次交易: 750 积分;首次交易狙击: 1, 500 点。完成所有首次奖励将保证以 2, 750 分的总积分晋升到管家级别。

2. 与交易金额挂钩:$ 1 = 1 Point ;$ 50 trade = 5 points, $ 1000 trade = 100 points。

3. 连续使用倍数:连续几天使用 Alfred 即可获得积分乘数;连续使用 Alfred 的每一天,积分都会增加 0.05 倍, 10 天后最多增加 1.5 倍;如果错过了一天,将恢复到前一天的乘数。

4. 推荐奖励:对于推荐的每个用户,用户将获得用户赚取的积分的 25% ,通过推荐系统可以获得的积分没有上限。