1. Market trend: the main currency is stable, and BTC is temporarily supported,

The latest number of BTC addresses shows that the number of addresses with more than 1000 BTCs is still stable. The value on April 13 remained at 2248, indicating that the main force of a large number of currency holders is still stable, indicating that the short-term correction of BTC price may be oversold. After the sharp increase in the number of giant whale addresses on February 28, there is little room for callback, which means that the selling volume of main investors is within a limited range, and low suction opportunities can be paid attention to in the short term.

In terms of price, BTC hit the off track of brin line after continuous withdrawal, and the technical rebound has lasted for three trading days. From the closing price point of view, the current short-term low rebounded continuously after January 22. The bottom of BTC has increased to US $39530 on April 11, maintaining a further upward trend.

At present, the disadvantage to the market is that the number of active addresses and trading volume of BTC are flat, and the strong price signal has not been further verified. Therefore, it is still necessary to maintain a medium and low level in the number of coins.

2. Interpretation of investor sentiment:

The panic index of BTC trading was sluggish, reaching 25 and 28 on April 13 and April 14. The panic was more serious.

At present, while the trading volume of BTC is running at a low level, the volatility also decreases during the price retreat. In terms of market conditions, BTC trading performance has been at a low level since 2022, and there are few opportunities for upward strong changes.

3. Dragon and tiger list:

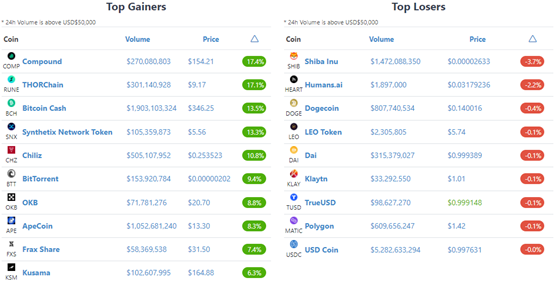

During the short-term rebound of mainstream currencies led by BTC, most sectors showed upward performance. Among the increase list, the top one is the defi concept comp, with a 24-hour increase of 17.4%. For similar currencies, Rune rose 17.1% in 24 hours and SNx rose 13.3% in the short term, also ranking top in the ranking. Other currencies with higher growth were distributed in different sectors, with BCH, CHZ and BTT rising higher.

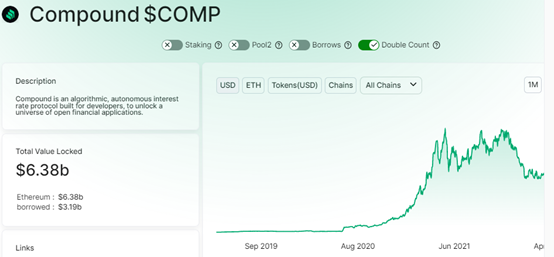

COMP

Recently, what has a great impact on comp price is the transformation of its economic model.

In 2020, compound innovatively launched the liquidity mining plan. But now, in order to solve the problem that liquidity incentives attract "speculative" liquidity, comp's incentives are expected to continue to change.

For example, comp will completely reduce the incentive to zero on April 15; Further improve the interest rate model in order to balance the interests of both borrowers and lenders. Finally, an alternative incentive plan will be introduced.

From the change of the number of locked positions of comp, the number of locked positions on April 14 was US $6.38 billion, and the quantitative performance is still relatively low. Therefore, the short-term price rise is driven by sentiment, and trading investors can pay attention to the progress of project incentives.

Rune

Rune price rebounded in the short term. Due to the amplification of the trading volume in the early stage by more than three times, the short-term price activity remained high. Rune has two ecological concepts of atom and Luna, and the price performance can continue to be concerned in the short term.

One development that inspires the rune community is the integration of Terra (LUNA) into the thorchain protocol. This integration also enables the platform to support all cosmos based projects. Terra integration brings Luna tokens and terrausd (UST) stable coins into the thorchain ecosystem and provides users with more trading and pledge options.

Affected by this, we can continue to pay attention to the ecological development of Rune and its driving effect on prices.

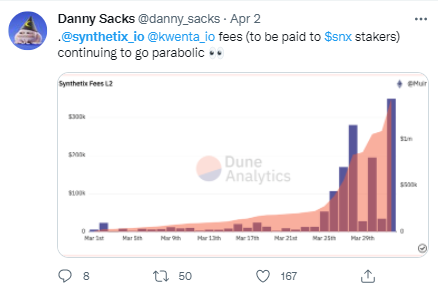

SNX

Synthetix aims to build decentralized and untrusted networks. The synthetix network token (SNx) token supports a variety of comprehensive assets, including legal tender linked to the US dollar, precious metals, indexes and even other cryptocurrencies.

In terms of data, the fees paid by SNx to pledgers continue to rise, which may be a strong evidence to promote the rise of SNx prices.

At the same time, we should also pay attention to the negative side of the news, which can not be ignored.

Grayscale removed synthetix (SNx) and sushiswap (sushi) tokens from its defi fund as part of the rebalancing in the first quarter of this year. SNx and sushi failed to meet the required minimum market value. No other cryptocurrencies were eliminated throughout the rebalancing process.

Decline list

Most of the currencies with the highest decline are concept currencies, with Shib and Doge ranking first and third in decline. In the short term, we need to pay attention to the adjustment expectations of these currencies.