Author: Claude, Shenchao TechFlow

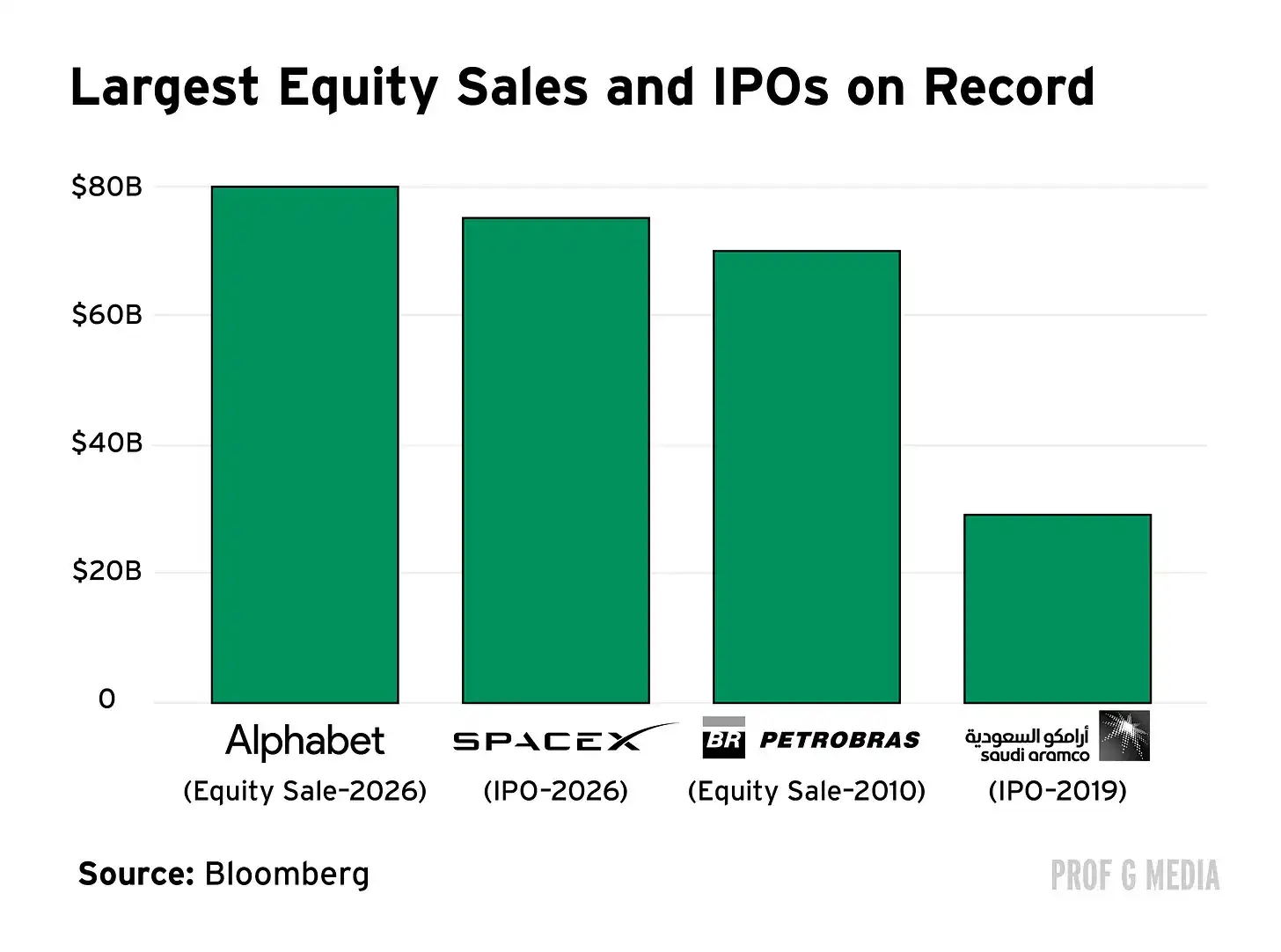

Shenchao TechFlow Insight: Alphabet priced $84.75 billion in equity financing on June 2nd, breaking Petrobras's 2010 record of $70 billion. The initial offering plan was $40 billion but expanded to $45 billion due to oversubscription; Berkshire Hathaway's $10 billion private placement anchored institutional confidence.

Meanwhile, SpaceX's $75 billion IPO is set to list on Nasdaq on June 12th, while Anthropic and OpenAI have both confidentially submitted S-1 filings. Total equity financing related to AI in 2026 could exceed $400 billion, nine times the size of last year's IPO market.

Alphabet has dropped a bombshell on the capital markets.

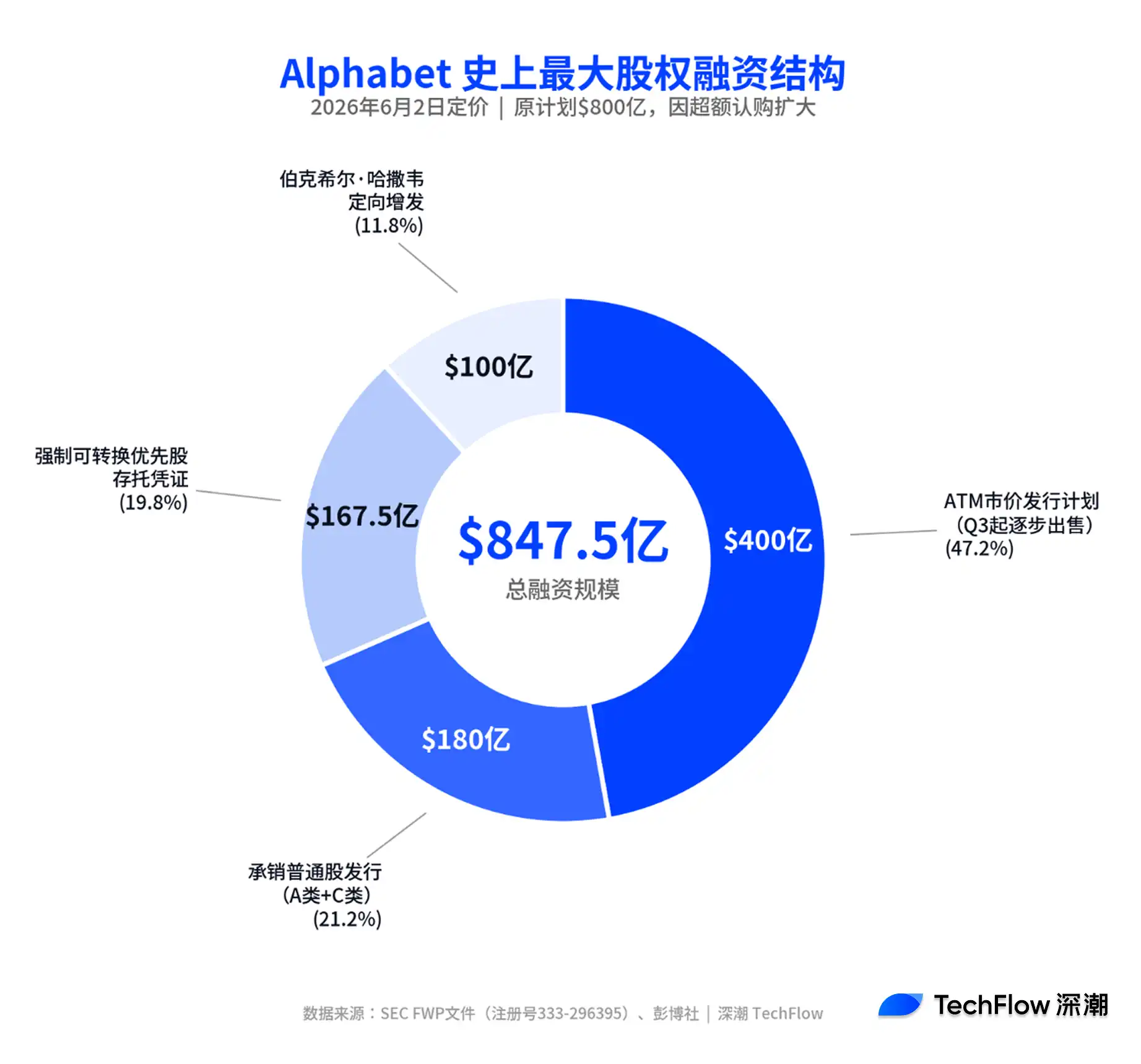

According to SEC filings and Bloomberg, Alphabet completed pricing for a total of $84.75 billion in equity financing on June 2nd, marking the largest single equity offering in history, surpassing the $70 billion record set by Petrobras in 2010 by over $14 billion. CEO Sundar Pichai posted on X platform that the initial offering was expanded from $40 billion to approximately $45 billion due to oversubscription. Following the announcement, Alphabet's stock price fell about 4%.

The destination of these funds is clear: AI infrastructure. Pichai defined it as "part of a multi-year investment strategy to seize the opportunities presented by AI." Alphabet's 2026 capital expenditure guidance has been raised to $180-$190 billion, nearly double the full-year 2025 figure of $91.4 billion.

How the $84.75 Billion Was Raised: A Four-Tier Structure Breakdown

This financing was not a simple secondary public offering but a composite structure pieced together from four components.

According to the FWP filing submitted to the SEC, the specific composition is: an underwritten offering of $18 billion in Class A common stock and Class C capital stock (expanded from the original plan of $15 billion); $16.75 billion in mandatory convertible preferred stock depositary receipts (expanded from the original plan of $15 billion), with a 6.25% fixed dividend rate; a $40 billion at-the-market offering program (ATM), which will gradually sell shares to the market starting in the third quarter; and a $10 billion private placement to Berkshire Hathaway.

The underwriting portion was priced at $355.20 per share for Class A shares and $351.80 per share for Class C shares. The common stock and depositary receipt offerings were settled on June 4th and June 5th, respectively.

Based on Alphabet's total market capitalization of approximately $4.2 trillion, this financing round represents less than 2% of its market value. According to Seeking Alpha analysis, considering the issuance structure and employee stock option tax obligations, the actual dilution effect may be lower than the nominal figure.

Buffett's $10 Billion Investment: Value Investors Cast a Vote of Confidence for AI Infrastructure

Berkshire Hathaway's $10 billion private placement was the most notable single transaction in this financing round.

According to SEC filings, Berkshire purchased equivalent amounts of Class A and Class C shares at approximately a 6.5% discount. This company, famous for value investing, has long been seen as conservative in the tech investment arena. But from heavily investing in Apple to now directly participating in AI infrastructure financing, Berkshire's move sends a signal: even the most cautious institutional capital now views AI infrastructure as an asset class worth betting on.

According to TechCrunch, Pichai specifically mentioned Berkshire's participation on X platform, emphasizing that its "long-term commitment to value investing" aligns with Alphabet's investment logic.

Google's Confidence: Q1 Revenue of $110 Billion, Cloud Backlog Exceeds $460 Billion

Alphabet's confidence in issuing an $85 billion financing check at this moment stems from solid data.

In the first quarter of 2026, Alphabet's total revenue reached $110 billion, a 22% year-over-year increase. Among this, Google Cloud revenue was $20 billion, a 63% increase, and contract backlog nearly doubled from the previous quarter to over $460 billion, with approximately 50% expected to be recognized as revenue within the next 24 months. Google Search and other business revenue grew 19% year-over-year to $60.4 billion, and Google paid subscription users reached 350 million. According to Prof G Media, Gemini's monthly active users are close to 900 million.

Pichai bluntly stated on the first-quarter earnings call: "We are constrained in the short term by compute supply." CFO Anat Ashkenazi added that capital expenditure in 2027 is expected to "increase significantly again." In other words, the $180-$190 billion annual capital expenditure is just the starting point.

Alphabet's President and Chief Investment Officer, Ruth Porat, played a key role in this financing round. Prof G Markets host Scott Galloway commented that Alphabet could have funded this investment entirely with cash from its own balance sheet, but Porat chose a smarter approach: financing with low-cost external capital while locking in investor allocations before Anthropic and OpenAI go public. "Every resource is finite, including investor appetite for AI infrastructure. Google just took $85 billion off the table," Galloway wrote.

The AI Financing Supercycle: SpaceX, Anthropic, OpenAI Queue Up for IPO

Alphabet's secondary offering is not an isolated event but the opening act of the 2026 AI capital markets supercycle.

SpaceX publicly filed its S-1 prospectus on May 20th, planning to issue 556.6 million shares at $135 per share, raising $75 billion, corresponding to a valuation of approximately $1.75 trillion. According to Bloomberg, the company is expected to price on June 11th and officially list on Nasdaq under the ticker "SPCX" on June 12th. The roadshow started on June 4th and has been oversubscribed. If completed, this will be the largest initial public offering in global IPO history.

Anthropic confidentially submitted a draft S-1 to the SEC on June 1st. Just prior, on May 28th, the company completed a $65 billion Series H funding round, with a post-money valuation of $965 billion, surpassing OpenAI's $852 billion to become the highest-valued AI company in Silicon Valley. According to multiple media reports, Anthropic's target IPO window is around October 2026, with exceeding a $1 trillion valuation on the first day seen as a baseline expectation.

OpenAI is also not far behind. According to CNBC's May 20th report, OpenAI is preparing to confidentially submit its IPO prospectus draft, with Goldman Sachs and Morgan Stanley acting as lead underwriters, targeting a valuation exceeding $1 trillion, with an IPO window between September and November 2026.

The Supply Shock of the $400 Billion Financing Wave: Can the Market Digest It?

Summing these numbers reveals a capital market financing scale in 2026 that is unprecedented.

According to Galloway's calculation, the largest year for IPO financing in history was 2021, with approximately $140 billion for the full year. The combined financing from just Google's secondary offering plus the IPOs of the three AI giants—SpaceX, Anthropic, and OpenAI—already far exceeds this record. If we add other AI-related listing projects like Cerebras and the entire 2026 financing pipeline, the total annual equity issuance could surpass $400 billion, approximately nine times the size of last year's IPO market.

Galloway presents a sobering historical statistic: the average maximum drawdown within one year of listing for the past 30 major IPOs was 55%. "The IPO moment is the peak of hype, the peak of demand. You are competing with every asset manager on the planet for the shares everyone wants," he wrote. "The smarter approach is often to wait for the hype to die down and find an entry point when fear is higher than greed."

For investors, Galloway offers a concise framework: Want AI exposure but unsure if Anthropic or OpenAI is worth their valuation? Buy Google. It's already one of the greatest businesses of all time, with a relatively reasonable valuation, offering upside with far less risk than pure-play AI companies. If AI ultimately disappoints, Alphabet won't disappear, but other companies might not be so lucky.